Follow Us on Google Discover

Follow Us on Google Discover

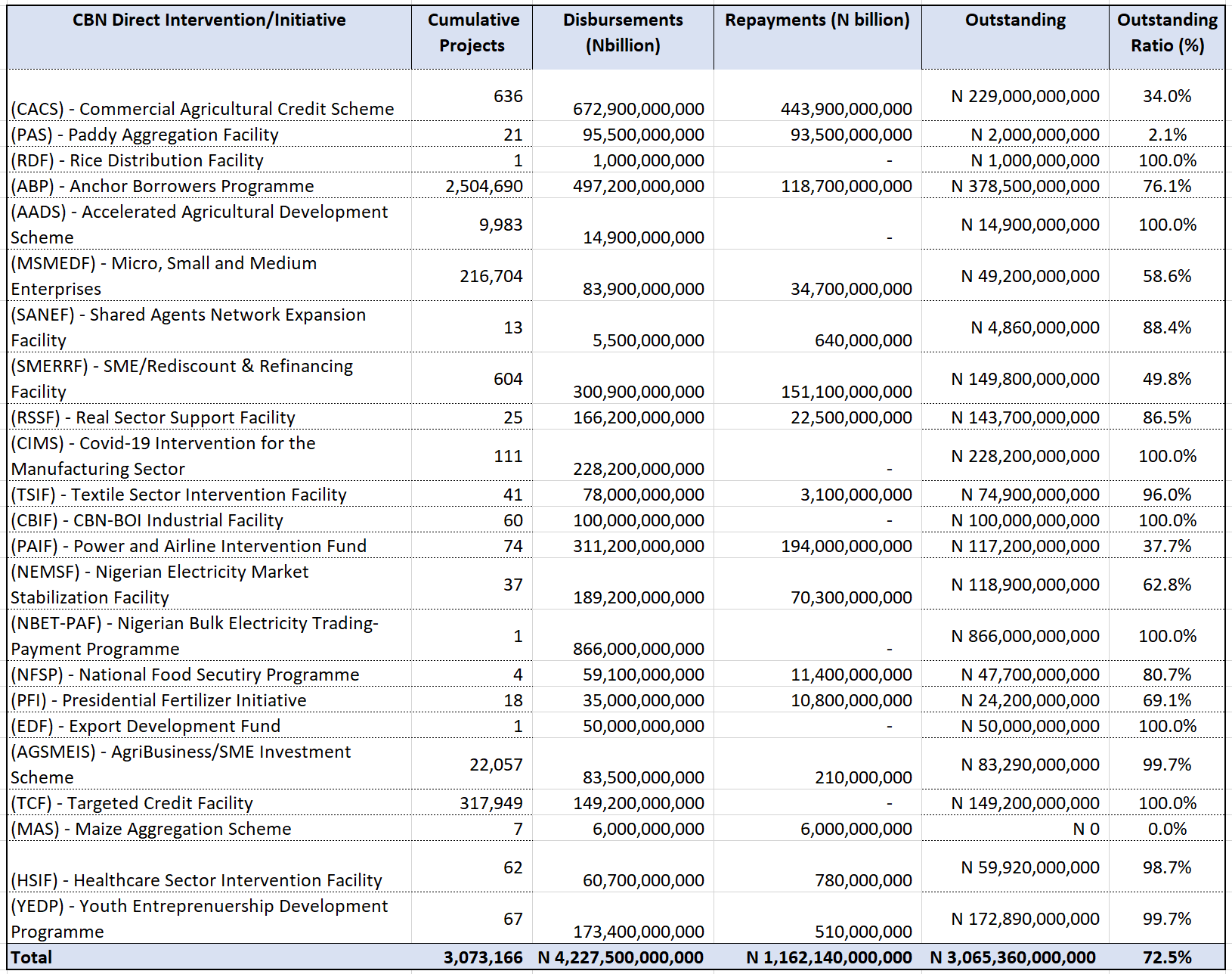

Over N3 trillion out of the N4.2 trillion intervention funds disbursed by the Central Bank of Nigeria (CBN) are outstanding as of December 31st, 2020.

This is according to data from the recently released fourth-quarter economic report (4Q’2020) of Nigeria’s Apex bank.

Given the recent dire results for Nigeria’s unemployment, inflation rate, and GDP growth rates, we were curious to assess the Central Bank of Nigeria’s (CBN) inventory of direct intervention programs which were supposedly created to address Nigeria’s economic challenges.

READ: NESG’s allegations, malicious attempt to tarnish the economic recovery program- CBN

Also Read

CBN Intervention Funds

According to the CBN, “Intervention schemes by the Bank continued to focus on enhanced credit delivery to critical sectors, in a bid to enhance productivity and stimulate the real sector of the economy.”

The Central Bank of Nigeria in its fourth-quarter economic report (4Q’2020) outlined the various activities and accomplishments by the Apex bank.

READ: How N343.95 million got missing in Water Ministry

Included in this 2020 economic report is a summary of the Central bank’s inventory of intervention programs with a breakdown of

- Number of intervention programs inflight,

- The total number of projects approved within each initiative.

- Funds disbursed by the Central bank for each initiative.

- Total repayments received as of November 2020.

Whilst the Central Bank must be praised for continuous transparency, the results of the program are worrisome.

READ: SERAP sues Buhari over FG’s plan to borrow N895bn from dormant accounts, unclaimed dividends

A) Where is all the money going?

Specifically, there are 23 major intervention programs in-flight for which N4.23 trillion Naira has been disbursed by the CBN across 3 million projects.

Remarkably, the CBN has an intervention fund for almost every single economic sector.

- a) Agriculture sector received. N1.47 trillion

- b) Power sector received N1.06 trillion.

- c) SMEs (across Manufacturing, Trade, Transportation) received N1.15 trillion.

Alarmingly of the N4.23 trillion disbursed, only N1.16 trillion (or 27.5%) has been repaid. Thus N3.07 trillion (or 72.5% remains outstanding).

READ: CBN introduces new charges for USSD services with effect from March 16

READ: CBN blames petroleum import for Nigeria’s $5.2 billion current account deficit

B) So where is the Impact of all the interventions?

One immediate question which comes to mind, if N4.2 trillion has been disbursed in intervention funds, and across multiple sectors, then how come the country has been experiencing anemic growth, with mind-boggling unemployment/under-employment statistics of over 50%?

One key observation is that the CBN interventions are concentrated on a tiny population of projects.

Specifically, of the N4.2 trillion in CBN interventions which the bank reports to benefit over 3 million projects.

- N3.1 trillion (73% of the total funds) were disbursed to only 1,116 projects (0.04% of projects).

- N1.1trillion (27% of the funds) were disbursed to 3million projects (99.96% of projects).

READ: CBN, Bankers committee back N3.5 trillion stimulus package for Nigeria

This suggests direct interventions in private sector initiatives that cater to the masses were a fraction of the total amounts.

This trend also shows up in the average size of the amount disbursed for each project. Whereby the Agricultural sector intervention of N1.467 trillion was disbursed to 2.5million projects (i.e. average of about N577,000).

The interpretation of this data indicates the CBN’s approach to intervention appears to be too fragmented to yield any expected reduction in unemployment nor lead to sustained GDP growth rates. This is despite all key sectors being targeted by the bank.

READ: How to access CBN’s N250 billion intervention fund for gas sector

C) Where are the Repayments?

So which projects are generating poor repayments for CBN? We have already seen that 73% of the N4.2 trillion is being distributed to 1,166 large ticket projects. Whilst 27% of the funds were distributed to over 3 million smaller size projects.

- Typical trends for Non-Performing Loans would suggest that there is a higher propensity for folks with smaller loan sizes to repay (think MFBs, credit unions, etc.) whilst borrowers with larger loan sizes arguably have a higher propensity to default.

- Remarkably, the CBN intervention fund appears to show a different trend where BOTH low-ticket sizes and high-ticket sizes are NOT repaying!

In the table below, both large-ticket and small-ticket borrowers have NOT repaid 72 to 73% of their loans.

READ: CBN introduces ‘Naira 4 Dollar Scheme’ for diaspora remittances

This begs the question, who exactly is tasked with collecting these funds for/by the CBN and how exactly is their performance appraised? One can only imagine the degree of angst if commercial businesses had these sorts of outstanding debt statistics.

Nairametrics however understands most of the intervention funds include terms that give its borrowers generous moratoriums on principal repayments allowing them to defer payment on the principal portions of the loans until later. The CBN extended waivers on principal and interest repayments of the loans in the wake of the Covid-19 pandemic-induced lockdowns.

But if the CBN is to continue down this path of direct intervention to stimulate the economy, there needs to be more assessment of the magnitude and efficacy of these interventions.

READ: Central Bank of Nigeria forex policy timelines 2020-2021

According to the apex bank, “improved credit delivery and intervention programmes are expected to stimulate output, thereby easing inflationary pressure, particularly, food inflation.”

However, The latest data from the National Bureau of Statistics states Nigeria’s inflation rate at 17.33% (4 years high) and food inflation at 21.79% (highest since 2005). One can argue that the intervention funds are for now failing to deliver on their core objective. The CBN may also site Nigeria’s surprising quick exit from the recession as a key benefit of its intervention programme, however at what cost?

The repayments of these funds need to be pursued more aggressively, not least because the CBN needs to facilitate money velocity in the economy by ensuring a higher turnaround of loans from existing beneficiaries to enable more Nigerians to benefit from the available funds.

This would be preferable to CBN printing more money and NOT chasing outstanding debt which economists would argue contributes to inflation without associated productivity growth.

I thanks the government for this plan, but some greedy people never allowed us to receive

Thank you for the contribution