Nigerian Banks increased their total loans to the Nigerian economy by N3.3 trillion in June 2020. This is according to information contained in the monetary policy communique of the central bank read out on Monday by the governor, Godwin Emefiele.

According to Mr. Emefiele, bank aggregate domestic credit grew by 5.6% in June 2020 compared with 7.7% growth recorded in the month of May 2020. This resulted in a total increase in gross credit from N15.56 trillion in May to N18.9 trillion as at end of June 2020. The CBN attributes the increase to its Loan to Deposit Ratio initiative, a policy that forces banks to lend at least 65% of its deposits.

“Aggregate domestic credit (net) grew by 5.16 per cent in June 2020 compared with 7.47 per cent in May 2020. The Committee

commended the CBN Loan-to-Deposit Ratio (LDR) initiative to address the credit conundrum as the total gross credit increased

by N3.33 trillion from N15.56 trillion at end-May 2019 to N18.90 trillion at end-June 2020. Emefiele.

READ NEWS: Non-Performing loans hit 4-year low as Banks recover N496 billion

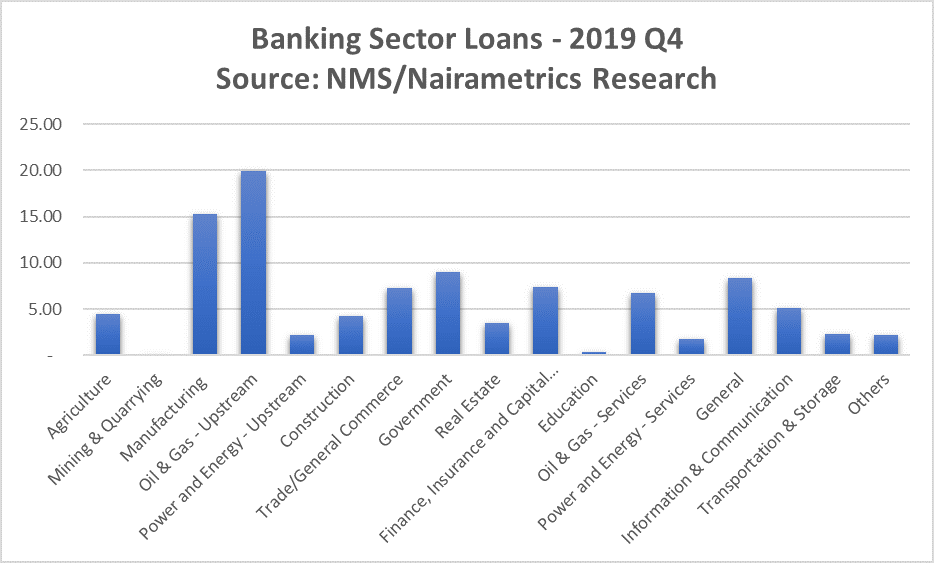

Who they lent to

The MPC reveals most of the loans went to the manufacturing, consumer credit, general commerce, information & communication and agriculture sectors. The CBN favours credit deployment to these sectors which it considers productive. Data from the financial sector reveals most of the banking sector credit goes to the Oil and Gas sectors with the productive sectors (as defined by the CBN) falling behind.

Commercial Banks have been hesitant to lend to these sectors due to its high rate of non-performing loans. Banks recorded an aggregative non-performing loans (specific provisions) of 6.5% as at December 2019. Sectors like the Agriculture sector saw their non- performing loans spike by over 40% last year.

Explore research data on Nairalytics from Nairametrics

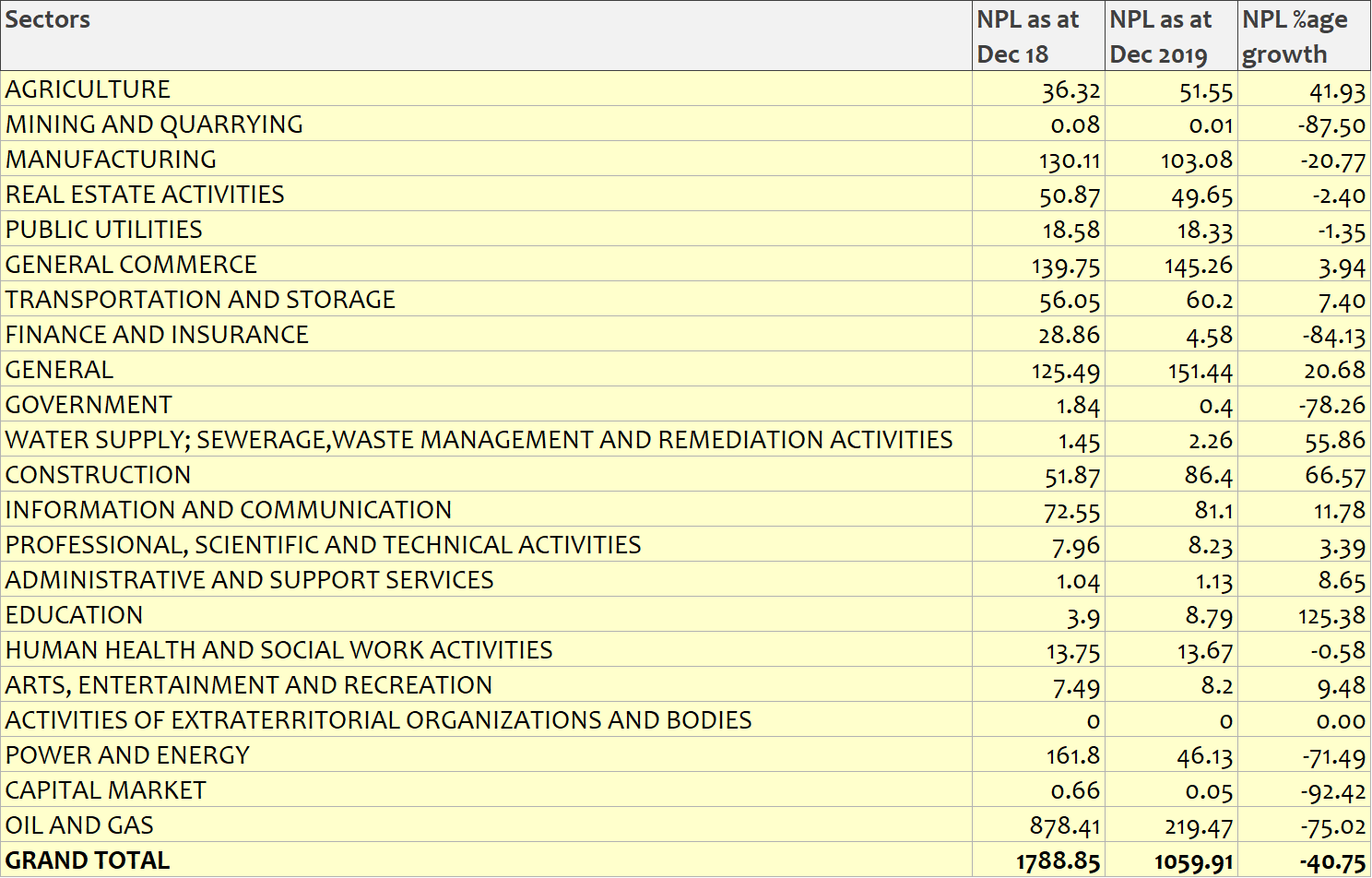

Construction and Educational sector also recorded significant spike in non-performing loans in 2019 compared to 2018. In general total non performing loans dropped from N1.78 trillion in 2018 to just over one trillion in 2019.

A recent research report by Fitch, seen by Nairametrics forecast a slower loan growth in 2020 due to the Covid-19 pandemic. However it does predict banks will lend more in 2021. “The weaker economy and lockdown rules will weigh heavily on client loan growth as demand for credit is hurt by consumer and business uncertainty. We expect client loan growth will decline to 2.5% in 2020 from 14.0% in 2019. However, we forecast growth of 4.3% in 2021 as the economy begins to recover” it reported.

READ MORE: Why the CBN will sack some bank directors soon

What this means: As Nigeria deals with the effects of the Covid-19 pandemic the spate of non-performing loans arising from the shut down in economic activities will be closely monitored when banks release their half year reports in the coming days. CBN’s confirmation of the N3.3 trillion in loans will attract scrutiny as analysts will identify banks that increased their credits and to which sectors. With the economic largely comatose in April and May, activities picked up in June but there is limited data to analyse how much positive or negative effect this may have had on the economy.

An increase in credit to the economy could also be viewed as positive for ban revenues which most analyst expected to come down in the second quarter due to a dearth in economic activities.

{kind=link}