Follow Us on Google Discover

Follow Us on Google Discover

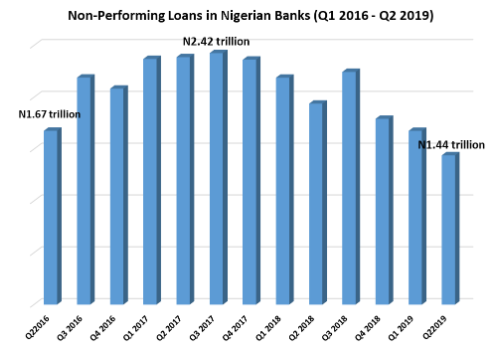

Non-Performing loans in Nigerian banks dropped to a record N1.44 trillion in the second quarter of 2019. This is reflected in the banking sector report released by the National Bureau of Statistics (NBS).

According to the Bureau’s report, non-Performing Loans (NPLs) in Nigerian banks dropped to a 4-year low of N1.44 trillion in Q2 2019 from N1.93 trillion. This suggests in one year, banks recovered N496.22 billion NPFLs.

Number Breakdown: The latest NBS report shows that total gross loans in Nigerian banks currently stand at N15.4 trillion as at the end of June 2019. According to the report, the percentage of non-performing loans to the total loan dropped to a single digit of 9.30%.

Also Read

- The latest drop in non-performing loan to a single digit makes it the first time percentage of non-performing loans to total gross loans dropped to a single digit since the fourth quarter of 2015.

- A further breakdown shows that huge drop in non-performing loans was recorded in oil and gas, real estate sector, information and communication, transportation and storage.

- Specifically, in terms of value, the oil sector, which controls the biggest NPLs across sectors, dropped by N193 billion at the end of June. The real estate sector ranks second declining by 96.4 billion.

- Other major sectors with drop in NPFLs include information and communication (N47 billion), finance and insurance (N31.45 billion), transportation and storage (N41.7 billion).

- However, the major sector that recorded rise in NPLs is power and energy with a 34% rise amounting to N19.7 billion.

Number explained: According to the European Central Bank, a bank loan is considered non-performing when the borrower fails to pay the agreed instalments or interest after 90 days. They are also called “bad debts”.

- Essentially, when banks lend out money, they do so with the hope that their borrowers will make their payments as scheduled. Meanwhile, borrowers sometimes default and are unable to repay their debts. That’s how non-performing loans become a problem for so many banks.

- In Nigeria, NPLs represent one of the most serious liquidity challenges facing the Nigerian banking sector. Bank loans are regarded as regarded as risk assets because the monies advanced as loans by the banks belong to depositors. The risk arises in the event of massive defaults and makes it difficult for depositors’ monies to be available on demand.

- It should be noted that oftentimes, several prudential tools such as liquidity ratio, loans to deposit ratio, large exposure and reserve requirements have been applied to address the issues of banks’ non-performing loans.

- The huge NPLs profile in Nigeria has been a major source of concern as this largely threatens the country’s financial sector. Due to growing concerns, President Muhammadu Buhari recently signed a new Act that gives the Asset Management Corporation of Nigeria (AMCON) more power to enforce recovery of debt from prominent Nigerians and corporate organisations.

The big drop: As earlier explained, the big drop in the NPLs was from the oil sector and this may be traceable to the recent policy move by the Central Bank of Nigeria (CBN). In an earlier publication on Nairametrics, it was disclosed that the CBN had given a directive to commercial banks for the immediate suspension of interests on non-performing loans to oil marketers.

- According to a report, the failure of the Federal Government to pay fuel subsidy to oil marketers has worsened non-performing loans in recent times.

- Confirming the development, the Managing Director of SunTrust Bank Limited, Ayo Babatunde disclosed that there was a 100% suspension of income on the oil marketers’ loans by banks.

- In recent times, AMCON in partnership with the Economic and Financial Crimes Commission (EFCC) have been a premeditating clamp down on individuals and banks on issues surrounding the non-performing loan which has continued to linger.

[READ ALSO: These companies have fallen under AMCON’s hammer]

Time’s up: With the latest drop in NPLs, time may just be up for banks, organisations and individuals responsible for the current N1.4 trillion nonperforming loans.

Recall that the details of the new AMCON law empowers the corporation to access bank accounts, computer system component, electronic or mechanical device of any debtor with a view to establishing the location of funds belonging to the debtor.

AMCON recently announced the take-over of two steel firms in Abuja and Calabar and other businesses. To further clamp down on the defaulters, the Federal Government has also set up an inter-agency committee for the purpose of recovering the debt owed to AMCON.

Or maybe banks wrote off more loans in the current year which shrunk the loan portfolio while also reducing the amount of NPLs