Follow Us on Google Discover

Follow Us on Google Discover

China recently became the first MAJOR economy to create its Central Bank Digital Currency (CBDC).

Specifically, China’s CBDC has gone from the testing phase to actual implementation. Such that the digital yuan is now ready for use in regular transactions. The expectations are that by the time athletes gather for the upcoming Winter Olympics, visitors to the country can pay for a wide range of goods and services using the Digital Yuan. (Think about using government digital currency to settle Hotel and Restaurant bills, Taxi rides, etc.).

Across the world, Central Banks are racing to implement Central Bank Digital Currency (CBDC). The latest BIS 2021 survey identified that 86% of Central banks are engaged in developing a CBDC.

In this article, we ask the question: What exactly are Central Bank Digital Currencies (CBDCs), and why are so many central banks are working towards their implementation?

Also Read

READ: Very few nations permitted to issue their Crypto – IMF

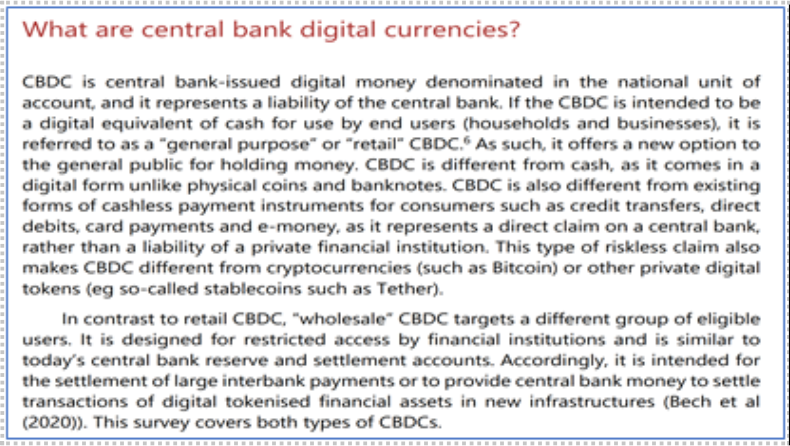

What is a Central Bank Digital Currency (CBDC)?

Specifically, CBDCs are legal tenders issued by a country’s central bank which will only ever be available in digital format AND will be acceptable from day one for payments of goods and services once implemented.

Fund settlement will be facilitated by the issuing Central bank who may / may not choose to partner with an approved list of institutional counterparties. The Bank of International Settlements (BIS) has a more technical definition here.

READ: U.S Central Bank leader says no rush into crypto dollar

For the avoidance of doubt, CBDCs are neither the same as Electronic Funds Transfers (EFTs) nor are they Cryptocurrencies. Despite many similarities such as contactless settlement between counterparties, key differences are that Central Bank Digital currencies are legal tender AND represent a direct claim on a central bank by end-users.

- So, if you are one of those people who likes to “spray” very crispy notes at Owambe… better be prepared as with digital currency, you will never see any physical notes to “spray”.

READ: Leader of world’s most powerful central bank says Crypto unreliable for wealth preservation

Which countries have CBDCs on the horizon?

The latest BIS 2021 survey of 65 central banks identified that 86% of Central Banks are engaged in developing digital currencies. Out of which 60% of central banks have begun research work whilst 14% of central banks are already in the pilot and proof of concept phase.

- Bahamas (Sand Dollar), China (Digital Yuan), and Sweden (e-Krona) are the nations most advanced with implementation.

For a list of countries at various stages of CBDCs implementation, you can click here and here or view the image below.

READ: U.S. dollar share of global currency reserves rose to 61.9% in Q1 2020 – IMF

How will the CBDCs work?

For now, each Central Bank is determining its own scope and CBDC functionality as there is no standard global framework regarding infrastructure requirements and functionality scope (e.g. some central banks simply want to focus on domestic payments whilst others want both domestic and international payments focus).

However, having said that, the underlying workflow will likely be similar across the world, in the sense that workflow will include solutions on distribution and utilization.

READ: Computers might steal Satoshi Nakamoto’s Bitcoin fortune

- Distribution: Central Banks will create the digital currency and permit a list of commercial banks to access to the central payment network for onward distribution to end customers. Given that CBDCs are digital, the Central Banks will be able to track exactly who is holding how much of their currency and how exactly their currency is being spent.

- Utilization: End-users will have a tool (e.g. digital wallets) to help them be aware of their CBDCs balances. Further, these wallets can be presented (i.e. scanned) at participating locations for transaction settlements (think QR codes on a phone app).

In other words, as a CBDC end-user, you only need access to the internet and electricity for spending. Intermediaries such as SWIFT will be bypassed. (You can read more about how the digital yuan will work here).

Why are so many Central Banks rushing into CBDCs?

Firstly, faster cross-border trade settlements / International Trade ambitions:

The widely accepted use of CBDCs will facilitate faster cross-border settlements between participating counterparties. Regardless of your location, there will be less need to convert from local currencies into reserve currencies such as USD, GBP, EUR, and vice versa via financial intermediaries.

Additionally, for a country such as China which has long sought to expand its global reach in international trade, the digital yuan provides mouth-watering opportunities.

- As a simple example, for international trade facilitation, end-users of smartphones built by Chinese-owned phone companies can potentially be enabled to access the Digital-Yuan, and that digital yuan can be spent with Chinese-owned firms across the world. These payment transactions can take place on the People’s Bank of China (PBOC) controlled network and bypass any existing financial intermediary (you can read more about digital yuan opportunities here).

Secondly, from a domestic perspective, CBDCs will be a potential game-changing macro-economic tool.

For countries not interested in global trade dominance, digital currencies offer Central banks an exciting opportunity to transform monetary policies. Specifically with regards to financial relationships and money transmission mechanisms (too much grammar but we have all heard of stimulus and intervention funds!!)

Under the current state, when a Central Bank wants to increase or decrease money going into the hands of consumers, it does so via a range of tools (i.e. alter interest rates, set reserve ratios, buy/sell short-term instruments, etc.). Unfortunately, this current approach has some limitations which include:

- Transmission mechanisms: Despite all the tools available to Central Banks, they ultimately rely on financial intermediaries (i.e. banks). Existing monetary policy tools simply aim to influence commercial banks to increase or decrease the amount of money/funds available for onward lending to end consumers.

- These tools, as well as, associated end-user responses may not often work as fast as Central Banks would like. As an example, most bank customers will tell you that loan application processes can be extremely cumbersome and sometimes subjective.

- Also, think about folks in remote areas who truly need credit for their business expansion but are not financially included or are not able to complete the plethora of loan application forms or are missing IDs for authentication, etc.

- All these limitations create latency challenges for Central Banks looking to influence macroeconomic indicators quickly.

- Monitoring: Under the current approach, it is cumbersome for Central Banks to continually track existing money in circulation and utilization purposes. Think about CBN intervention funds and how difficult it is for the CBN to know exactly how its intervention funds are being spent once the funds are disbursed to applicants.

Fortunately, with digital currencies, given that they leave digital footprints, Economic Surveillance is facilitated (i.e. Central banks can monitor exactly who owns how much and what it is being used for); arguably giving Central Banks an opportunity to better direct funds to parts of the economy requiring support.

Thirdly, Technology advances driving the growth of the Digital Economy and lowering operating cost dynamics.

- The unrelenting growth of the Digital Economy: The use of physical cash continues to decline driven by the exponential growth of contactless services such as e-commerce (Amazon, Alibaba, eBay), contactless interaction (Zoom, Facebook-Portal, Google-Nest), etc.

- Global eCommerce is now projected to be over 25% of total retail sales across the world and the US estimates that Digital Economy accounted for 6.9% of 2017 GDP which made it the seventh (7th) largest component of GDP and still growing.

- Given that no one needs physical cash for transactions in the digital economy, Central banks are warming up to the need to implement CBDCs for transactions in this emerging digital economy.

- Changing unit cost dynamics: From a central bank perspective, there are significant costs incurred for maintaining oversight of existing payments and settlement systems. Furthermore, there are additional costs for creating cash, transporting, storing, and securing existing stock of physical cash. As existing systems become outdated and population growth continues apace, there will be an inflection point for when it will simply be cheaper to create digital currencies to drive financial inclusion. Especially as cloud computing processing capacity continues to expand at a cheaper unit cost.

Are there risks/issues to be concerned about with Digital Currencies?

The answer is yes, whilst there are benefits, there are also some risks and concerns such as the risk of excessive Economic Surveillance, Privacy concerns, ease of implementing, and Negative Interest (aka financial wealth tax).

Economic Surveillance can easily be a double-edged sword especially in the hands of an authoritarian regime, as an increased level of economic oversight can easily lead to financial repression or targeting opponents. However, just like with CCTVs, the risk of misuse cannot be a unilateral reason to discredit the opportunities available with CBDCs. (You can read more about concerns here)

So, what about Nigeria?

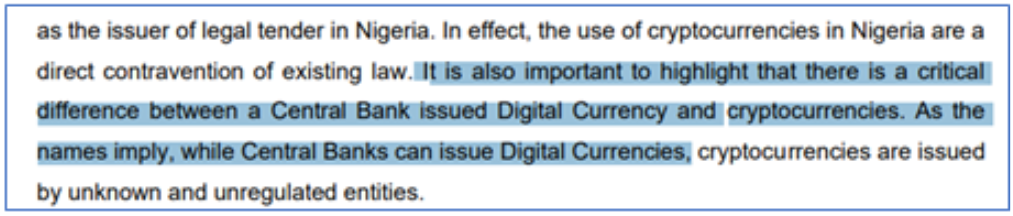

The Central Bank of Nigeria (CBN) was not included in the BIS 2021 survey, additionally, the CBN has not formally outlined its position on whether it plans to implement a Central Bank Digital Currency in the future (e-Naira).

However in February 2021, (as part of its explanation of its regulatory directive on Cryptocurrencies), the CBN acknowledged the emerging trend of Central Banks’ ability to issue legal tender digital currencies.

Nairametrics founder, Ugodre mentioned on his Twitter Spaces show “OnTheMoney” that a senior official at the CBN informed him that the Apex bank was seriously considering digital currency and had put together a team to explore its possibilities.

So, should Nigerians expect an e-Naira soon?

Firstly, with regards to innovation, the Nigerian payments landscape continues to evolve rapidly as the CBN drives innovation as part of its National Financial Inclusion Strategy (NFIS). Thus far, this strategy has resulted in the deployment of new products in the Nigerian payments space such as Money Market Operators (MMOs), Payment Solutions Service Providers (PSSPs), Agent/Super Agents, Payment Service Banks (PSBs), etc.

Furthermore, the CBN is keen to leverage its regulatory sandbox for more innovations and has very recently in 2021 issued new guidelines on open banking, as well as, QR codes.

Consequently, having a digital Naira should not be ruled out as an additional tool to drive financial inclusion in Nigeria,

Secondly, based on industry statistics, Nigerians are quick to adopt technology that facilitates convenience at minimal cost to end-users.

- Specifically, CBN payments statistics reports show that the use of cash and ATMs in Nigeria continues to decline rapidly. The latest annual report shows Cash/ATM usage has declined from 18% of transactions in 2015 to 6% of transactions in 2019. In other words, 93% of activity was done electronically (across platforms NIP, REMITA, MMO, etc).

- Furthermore, NCC reports show high penetration rates for mobile technology with over 195 million active mobile phone subscribers (95% penetration) and 150 million internet subscribers (73% penetration rate).

These reports lend credence to the perception that Nigerians are quick adopters of new technology where the technology enhances convenience at minimal cost to end-users.

Consequently, a digital Naira will likely have high adoption rates to the extent that end-users do not expect to incur additional onerous charges.

Finally, from a CBN perspective, we already know that the APEX bank prefers direct interventions as part of its macroeconomic toolkit. Arguably having a digital Naira (e-Naira) allows the CBN to better facilitate direct transmission to target beneficiaries in key sectors, whilst monitoring the use of the funds disbursed, and expedite recovery when funds are due for repayment.

So, should we expect a CBN announcement on e-Naira soon? Your guess is as good as mine.