Follow Us on Google Discover

Follow Us on Google Discover

Crude oil prices have risen incredibly in 2021 amidst global vaccination, lockdown easing and sustained OPEC+ production cuts.

Analysts all over the world were beginning to speak about a supercycle for oil. Brent crude was gearing towards $70. Big banks in the US like Goldman Sachs and Morgan Stanley all made predictions of a $70 – $75 oil at some point in 2021. Christyan Malek, JP Morgan’s Head of Oil and Gas stated, “We could see oil overshoot towards, or even above, $100 a barrel.”

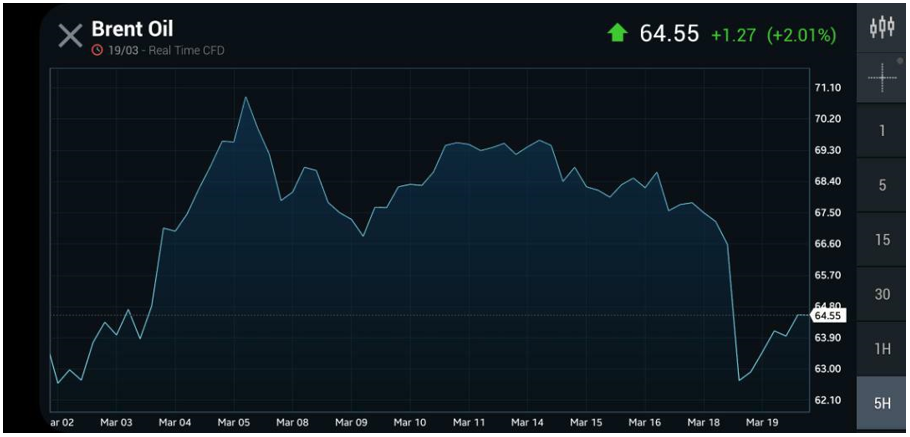

On Friday, 19th March 2021, Brent crude settled at $64 and WTI at $61 after a slump of about 7% last week Thursday – basically erasing all the gains made when OPEC+ sustained cuts in early March.

READ: World’s biggest oil company, Saudi Aramco pays a whopping $75 billion in dividend

Also Read

'/%3E%3C/svg%3E) Data Source: investing.com

Data Source: investing.com

What seemed like an incredibly bullish outlook for oil in early March when oil prices were 30% up YTD have dropped significantly and here is why:

US Bond Yields

The rising yield on US 10-year bonds has caused a stir in the market and it has a domino effect on the global market. How did this happen? The US feds rounds of quantitative easing and stimulus checks in the market have essentially created an inflation problem.

- When fund managers anticipate the inflation is going to rise it pushes the yield on government bonds up.

- As a bit of background, US bonds are classified as the safest investments globally. A promise of higher yield on the fixed-income asset class caused a selloff on oil futures.

- This is not only peculiar to commodities but also to other assets classes like stocks. As long as the US bond yield remains a lingering issue for the Fed and investors, it is very difficult to see a $70 oil.

READ: Number of Bitcoin millionaires worth at least $5.7 million hit one month low

Stronger Dollar Index

- With the US yield rising, this makes the dollar stronger compared to other currencies because other countries cannot compete with the US bonds, you might ask why? But the answer is simple, when the US bonds have higher yields because they have a better creditworthiness than most countries, investors will favour moving their funds to the US.

- As more investors flock to the US bond market it creates a higher demand for the US dollar over other currencies which increases the value of the FX.

- First, oil is priced in dollars. Although the relationship is not perfect with certain conditions responsible for deviations that might occur, there’s normally an inverse relationship between the dollar and oil prices (in fact all commodity prices).

- Historically, the price of oil drops when the dollar strengthens against other major currencies which affects the purchasing power. A stronger dollar means oil becomes expensive to purchase.

READ: Critical times for Nigeria’s oil money as US-China trade war escalates

Weekly EIA report

- The Energy Information Administration released its weekly stockpiles report with 2.396 million barrels last week, marginally ahead of the consensus expectation.

- Basically, the EIA report shows the amount of crude oil barrels in the market, and if there are more crude oil barrels than anticipated it indicates there is a demand problem and the market is oversupplied.

- Some analysts have long questioned the reality of the oil price from a demand perspective, with strong indications that the futures market does not reflect the true reality of the physical market due to backwardation – a situation when the futures prices are below the spot price.

China and India demand

- India and China are net importers of crude oil and with a combined population well over 3 billion people, their moves in the market have a deep effect due to consumption levels.

- The bulk of oil exports go to China and India and the weighting of global demand usually depends on both nations.

- China’s demand has sustained oil prices for months and not much has changed except China’s growing interest in Iranian crude with a reported 856,000 bpd import, which has not gone down well with the US due to stringent sanctions on the Arab nation. Furthermore, this complicates OPEC´s effort to control the market and as a result oil price.

- India never hid their dissatisfaction of high oil prices, Dhamendra Pradhan, India´s Petroleum Minister has on numerous occasions urged OPEC to reduce supply cuts because high oil prices were slowing down the economic recovery.

- India who imports 80% of their crude oil has stated plans to diversify away from the middle east for supply which potentially brings the US shale producers in the market.

Bottomline

- OPEC’s tight control of the oil market seems to be weakening after a very positive early March for the ‘cartel’. The market and geopolitical interests have seemingly slowed down a rallying oil. With these rising concerns, the OPEC meeting on the 1st of April has a lot riding on it than earlier anticipated.

- The consensus is that Saudi will view the recent oil selloff as leverage to call for a rollover as the markets have not rebalanced. Traders are betting on a return to travel in summer to improve jet fuel. The markets are dicey at the moment and the idea of a supercycle might have just been a farce.

This article was co-authored by Adetayo Adesola and Opeoluwa Dapo-Thomas

Adetayo Adesola is a Bloomberg LP trained market analyst and he is the Head of Content & Strategy at Nairametrics. You can reach Adetayo here: https://www.linkedin.com/in/adetayo-adesola-6420496a/

Opeoluwa Dapo-Thomas is an Investment Banker and Energy analyst. He holds an MSc. International Business, Banking and Finance from the University of Dundee and also holds a B.Sc in Economics from Redeemers University. As an Oil Analyst at Nairametrics, he focuses mostly on the energy sector, fundamentals for oil prices and analysis behind every market move. Opeoluwa is also experienced in the areas of politics, business consultancy, and investments. You may contact him via his email- dapothomasopeoluwa@yahoo.com.