During the week, the National Bureau of Statistics (NBS) released the Consumer Price Index Report (CPI Report) for May 2021. The NBS CPI number is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected monthly and used to measure changes in the price level of a weighted average of a basket of consumer goods and services purchased by households during the period. The monthly percentage change in the CPI is used as a proxy for monthly inflation rates.

According to the current CPI Report, on a month-on-month basis, the Headline Composite Consumer Price Index increased by 1.01 percent in May 2021, representing 0.04% points higher than the 0.97% recorded in April 2021. The month-on-month rise is attributable to rises seen in the prices of basic food items such as Bread, Cereals, Milk, Cheese, Eggs, Fish, Soft drinks, Coffee, Tea and Cocoa, Fruits, Meat, Oils and Fats and Vegetables. This is seen in the month-on-month food sub-CPI which increased by 1.05% in May 2021, up by 0.06% points from 0.99% recorded in April 2021.

On a year-on-year basis, however, as at the end of May 2021, the composite consumer price was 17.93%, effectively implying a reduction in inflation by 0.19% points, when compared to the 18.12% rate reported in April 2021. The divergence between month-on-month and year-on-year CPI implies that while inflation is rising marginally from month to month, it is declining more aggressively when the current CPI number is compared to the same period in the previous year.

Core Inflation, which is made up of all items less farm produce, stood at 13.15% at the end of May 2021, up by 0.41% when compared with 12.74% recorded in April 2021. The highest increases were recorded in prices of pharmaceutical products, garments, shoes and other footwear, hairdressing salons and personal grooming establishments, furniture and furnishing, carpet and other floor covering, motor cars, hospital services, fuels and lubricants for personal transport equipment, cleaning, repair and hire of clothing, other services in respect of personal transport equipment, gas, household textile and non-durable household goods.

Are prices of food items really dropping?

Historically, a key driver of inflation has always been associated with changes in the composite food index or changes in food prices, and indeed, the NBS CPI Report confirms that Nigeria’s inflation had been on an upward trajectory for 20 consecutive months from August 2019 until the downward inflationary trend began in April 2021.

The upward trend in inflation during the 20 consecutive months from August 2019 was largely due to food inflation exacerbated by the temporary closure of the Nigerian borders in August 2019. With the year-on-year composite food index reducing to 22.28% in May 2021 (a critical segment in the basket of consumer goods and services purchased by households) compared to 22.72% in April 2021, the composite consumer price was bound to reduce in tandem.

Several sources appear to provide data and reports that are at variance with the CPI reports released in the last few months. Specifically, the Central Bank of Nigeria communique issued after Monetary Policy Committee meetings have repeatedly identified persistent insecurity across the country, protracted structural deficiencies impacting the logistics of moving food items to urban areas such as poor road networks, unstable power supply and a host of other infrastructural deficiencies, persisting impact of coronavirus-induced supply disruptions, hikes in the electricity tariffs, and exposure to international petrol prices etc., as the root causes of the continued rise in inflation as well as persistent exchange rate pressures, dwindling capital flows, weak growth of the foreign reserves, and other structural issues. Most of these structural issues still exist yet, inflation appears to be declining.

In addition, the World Bank in its Nigeria Development Update published in June 2021 reported that rising Nigerian inflation rates were exacerbating impoverishment and depressing the economy; “driven by a steep increase in food prices” with the situation worsened by poor weather, insecurity and conflict, and pandemic-related issues that affect food production and access to markets.

The same World Bank update also pointed out that “prices are increasing rapidly, severely impacting Nigerian households. As of April 2021, the inflation rate was the highest in four years. Food prices accounted for over 60% of the total increase in inflation. Rising prices have pushed an estimated 7 million Nigerians below the poverty line in 2020 alone.”

The consensus amongst economists also, is that cost of basic food items are directly correlated with the level of agricultural activities. With the intractable Boko Haram insurgency in the Northeast, the persistent farmer-herder communal clashes largely in the Middle Belt (the food basket of the country), persistent kidnap of farmers and traders across the country, poor road network and epileptic power supply; all of which contribute to constricting food production, distribution, and storage, it is not clear how NBS CPI data represents that food inflation is improving year on year.

Does the exchange rate have anything to do with this?

A myriad of empirical research confirms that there is a positive and significant relationship between exchange rates and inflation. This implies that we expect inflation to worsen as exchange rates deteriorate and vice versa. In Nigeria’s case, there is a vicious cycle where unbridled demand for foreign currencies using the local currency, to whet our craving for imported goods and services or simply because of personal preferences to hold assets and investments in hard currencies as a hedge against further local currency depreciations, puts constant pressure on the nation’s foreign reserves, causing regular depreciation of the local currency against the United States dollars.

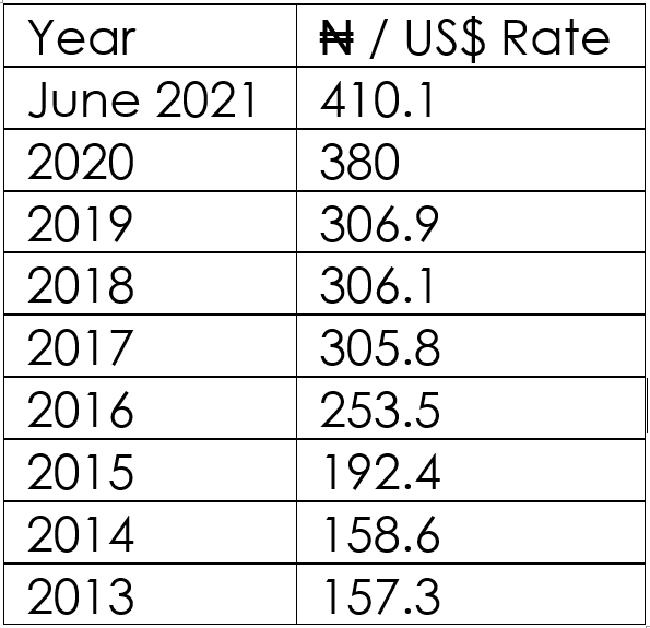

In addition, empirical research shows that over time, extensive foreign exchange controls restrict access to the official exchange market and stimulates the growth and expansion of a parallel market. Central Banks also typically respond to a growing parallel market premium by further tightening exchange controls, particularly where the official exchange rate continues to deteriorate, and so, the vicious cycle perpetuates. Unfortunately, as shown in the table below, currency depreciation only leads to even more demand for the United States dollars while not necessarily stemming the decline in the foreign reserves.

Source: World Bank, Abokifx

Any explanations for the inconsistency?

While not authoritative, a few reasons may explain the inconsistency between the dropping inflation rates as calculated by NBS and the increasing inflation rates as implied by other sources. The construction of the price index is based on a selection of the market basket of approximately 740 goods and services. Practically, some specific goods may not be readily available and as a result, substitute goods are used which may be relatively cheaper than the regular goods which may be relatively more expensive if available. Cheaper substitutes or replacements that cause a downward bias in prices quality should not be considered deflationary, particularly if the substitutes in the basket of goods are not the actual items that households purchase. Also, when prices of existing goods change due to changes in quality, deterioration in quality should not be considered deflationary just as improvements in quality that result in a price increase should not be considered inflationary.

Inflation rates are a composite of urban and rural inflation. In Nigeria, while many states are suffering significant inflationary rates, other states have relatively benign inflation rates. Population growths differ significantly by State, and as a result, the market demand-supply dynamics also differ from state to state. For example, in May 2021, all items inflation on year-on-year basis was highest in Kogi (25.13%), Bauchi (23.02%) and Sokoto (20.11%). The population in these states are not as significant as some more populated states, whereas states like Katsina (15.69%), Imo (15.52%) and Delta (14.85%) that are more populated than the likes of (say) Kogi, recorded the slowest rise in headline Year on Year inflation.

The relevant question, therefore, is to understand where the sample market basket of goods and services are predominantly selected from and how these are proportioned by states as these selected criteria determine to a large extent the prices of goods and services that go into the basket.

{kind=link}