Follow Us on Google Discover

Follow Us on Google Discover

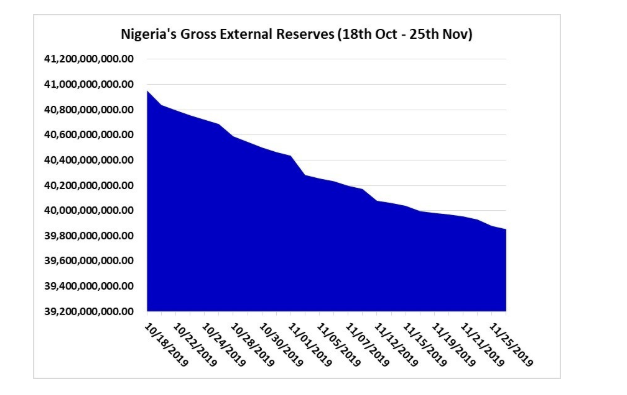

During the week, reports from the website of the Central Bank of Nigeria confirmed that the external reserves stood at $39.8 billion, the first time it dropped below $40 billion in almost two years.

The external reserves depleted by another $1.1 billion in less than 5 weeks, as this is the highest fall it had recorded in the past 22 months.

According to the latest data obtained from the Central Bank of Nigeria (CBN), Nigeria’s external reserves dropped from $40.9 billion on 18th October to $39.8 billion in 26th November 2019.

Why the reserves are falling

Several factors determine the rise or fall in external reserves. In Nigeria, it has always been crude oil earnings and foreign investment inflows into the country.

Other News

- While providing reasons for the latest decline in the country’s reserves, the CBN disclosed in its monthly economic report for October 2019 that the decline was due, mainly, to foreign exchange market interventions, direct payments and foreign exchange sales at the I&E and SMIS intervention window

- Although the decline in the country’s external reserves has coincided with recent fluctuations in global oil price with Brent crude oil hovering around $62 a barrel, the depletion in reserves has more to do with other factors other than the global events.

[READ MORE: Nigeria’s External Reserves plunge to $40.3 billion as devaluation concerns brew]

- For instance, analysts have argued that as capital flows out of the economy, the CBN would continue to actively intervene in the foreign exchange market to keep the Nigerian Naira in check.

- A quick look into capital flows on the Nigerian capital market shows that foreign portfolio outflow stood at N428.8 billion in October 2019 (YTD), while inflow was N363.9 billion. This means capital outflow outpaced inflow on the Nigerian bourse.

- With the latest decline, the external reserves position could only finance 5.1 months of imports of goods and services, and 8.7 months of goods only, using the import figure for second-quarter 2019.

CBN says no alarm

Nigeria’s external reserves may have continued to plummet in recent months, but the CBN has once again stood firmly behind its intervention policy.

While fielding questions from newsmen after the Monetary Policy Committee (MPC) meeting in Abuja on Tuesday, the CBN governor, Godwin Emefiele said the drop in the reserves was not enough to create fear in the economy.

According to Emefiele, “During the period when we had an economic crisis in 2015, 2016 and early 2017 where reserves dropped to 23 billion dollars, the country managed it and it survived. We do know that there is a focus on the fact that crude oil price is not as resilient as it was in 2018.

“We believe that crude oil price today at $63 per barrel, notwithstanding the drop in reserves below $40 should not cause any panic.”

Why investors are worried

While the CBN may have doused the tension with its remark, economic headwinds suggest investors should be worried.

For instance, while reading the communique on Tuesday, Emefiele disclosed that the Federal Government should reduce the $57 oil price benchmark as oil prices would remain relatively weak into the foreseeable future. This means foreign exchange earnings for Nigeria may continue at the low ebb going into 2020.

Investors are already raising concerns as the sustained decline in the country’s external reserves is raising questions about whether the CBN has the capacity to continue to ensure exchange rate stability.

Commenting recently, the Chief Executive Officer, Financial Derivative Company Limited, Mr Bismarck Rewane, said, “Demand for dollars will increase in the coming month due to inventory build-up ahead of Christmas and this will mount pressure on external reserve, hence gross external reserve level may decline further.”

[READ ALSO: External reserves drop by $3.2 billion in Q3’19]

What this means for 2020

With a large chunk of the country’s reserves also used in servicing external debt, the reserves may just continue to deplete, and this may pose a serious threat to the Nigerian economy going into 2020.

Already, more borrowings to fund the 2020 budget has been mooted by the government. This means as foreign portfolio investment declines, rise in debt servicing and continued intervention by the CBN in the FX market will trigger more pressure on the country’s reserves.

The drop in reserves means available buffer for the CBN to stabilise the exchange rate continue to weaken, suggesting devaluation may be on the cards if things get worse next year.

We must try our possible best to keep our foreign reserve steady.