Welcome once again to the summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills, Bonds, FX rates, inflation, oil price.

This report is dated May 10th, 2019.

***CBN debunks report of missing N500 billion***

Key Indicators

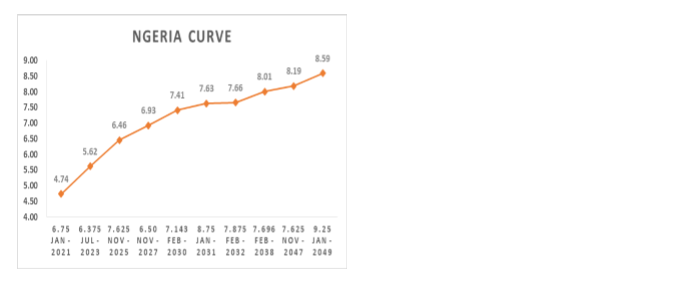

Bonds: The Bond market closed the week on a firmly bullish note, with yields closing lower by c.6bps on the day, largely fuelled by some renewed offshore interest notably on the 2028 bond. Yields consequently traded significantly lower across all tenors, as market players picked on offers in a demand-driven session.

We expect the recent bullish momentum to persist in the new trading week, but with some profit taking anticipated as yields approach the c.14.00% psychological level.

Treasury Bills: The T-bills market remained bullish, with demand noticeably on the mid to long end of the curve, as market players looked to fill lost out bids from the previous OMO auction. We, however, witnessed slight sell on the shorter end of the curve, due to the retail FX funding constraint by some banks.

We expect rates to remain relatively stable on the mid to long end of the curve, in the absence of a renewed OMO auction by the CBN.

Money Market: The OBB and OVN rates increased by c.4.00%, due to outflows for a retail FX auction by the CBN. The OBB and OVN rates consequently closed the week at 9.14% and 10.00%, with system liquidity estimated at c.N400bn positive.

We expect rates to remain slightly pressured opening the new week, due to funding for the weekly wholesale FX auction by the CBN.

FX Market: At the Interbank, the Naira/USD rate remained unchanged at N307.00/$ (spot) and N356.60/$ (SMIS). The NAFEX closing rate in the I&E window declined further by 0.06% to N360.88/$, as market turnover improved by 71% to $367m. At the parallel market, the cash rate decreased by c.0.14% to N358.80/$, while the transfer rate remained unchanged at N363.50/$.

Eurobonds: The NIGERIA Sovereigns found some support in the last trading session of the week, as oil prices gained above $70pb, despite the 15pct hike in the US tariff on $200bn of Chinese imports. Yields were consequently lower by c.6bps on the day, with the most price gains observed on the shorter end of the curve.

In the NIGERIA Corps, we witnessed some renewed profit taking on the FIDBAN 22s and ETINL 24s, in the absence of the significant demand earlier witnessed on the tickers.

Contact us:

Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}