…others rely on cash flow to pay down debts.

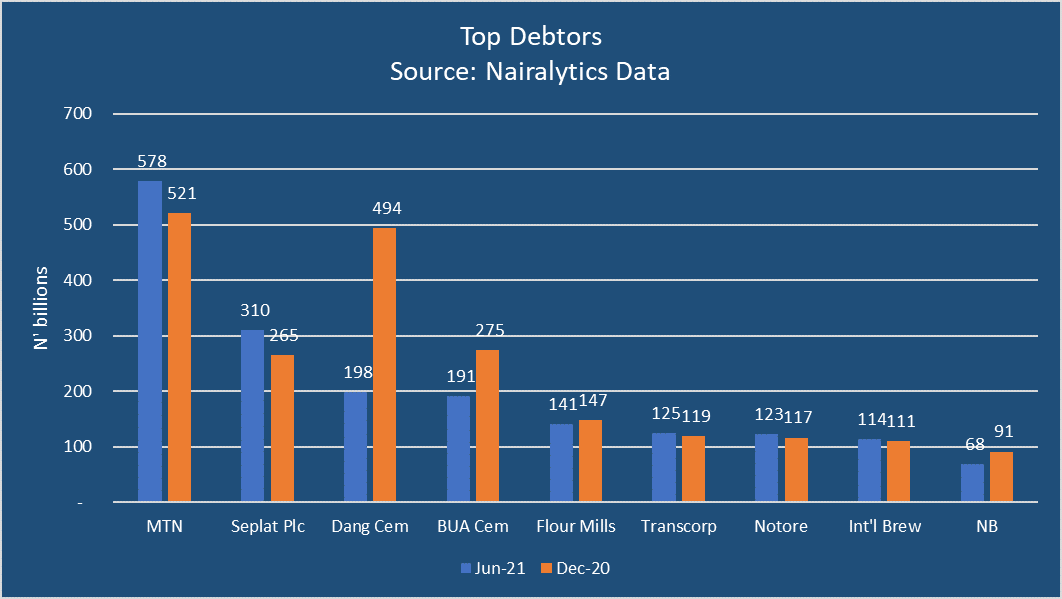

Nigeria’s largest telecommunications firm, MTN retained its position as the largest borrower on the stock exchange after it reported a total short- and long-term loan balance of N578 billion as of June 2021. MTN ranked higher than all the companies listed on the Nigerian stock exchange when it came to borrowing from banks and the debt market.

The company is well known for strategically relying on loans to drive operations resulting in astronomical returns on average equity often in the higher double digits. As of December 2020, MTN’s total external loan was N521.5 billion and has increased by 11% in under 6 months. This places its debt at 2.8x its equity. Closest to MTN in relying on debt to boost earnings and operations is Nestle Nigeria Plc. Nestle’s debt to equity is also 2.27x and posts an annualized return on equity of nearly 60%. MTN’s return on average equity is just over 60%.

Cement Giants

While MTN has focused on increasing its debt profile, Nigeria’s Cement giants, Dangote Cement, Lafarge and BUA have moved in the other direction all recording massive drops in their loan portfolio. Dangote Cement, one of Nigeria’s largest-ever companies by profit and the largest by market capitalization, reduced its total external debts by 30.5% going from N493.9 billion in December to N197.9 billion as of June 2021. Lafarge cut its debt profile by 60.3% to N19.75 billion while BUA reduced its own debt by 30.5% to N191 billion.

No new equity was raised by the trio in the first half of 2021, as they focused on organic cash flows to repay debt. According to our research, the companies have repaid their debts from cash flows generated from operations combining them with higher trade creditors. Between the three cement giants, they generated N469.7 billion in net cash flow from operations paying down N409.7 billion in debts.

Food Processors

Just like MTN, major food processing companies like Nestle, Flour Mills and Honeywell relied heavily on debt to drive operations in the period under review. Their debt profile rose to N260 billion from N247 billion in the six months between December and June 2021. Flour Mills retained the most loan portfolio with N140.9 billion, lower than the N147 billion reported in December. Honeywell, which has been in controversy with the CBN over its loans to First Bank increased its loans to N67.6 billion from N59.4 billion. Nestle also increased its loan portfolio by 29% to N51.9 billion. It appears the strategy for these firms is to fund operations with debt relying on it to boost top-line revenues and improve returns.

Food Processing companies have seen a major profit boost since the start of the border closure and the forex crisis that has hampered the import of competing goods and services. For example. Flour Mills trailing 6 months pre-tax profits of N20.9 billion between January and June 2021 compared to N11.6 billion in the corresponding year. Thus, despite loading their balance sheets with debts, profits and margins remain high despite experiencing increased borrowing cost. The strategy here is to use cheaper debts to fund operations and boost bottom line revenue, a well-known strategy for companies with high returns on assets, especially in a low-interest environment.

Brewery

Guinness and International Breweries also increased their debt portfolio during the period whilst Nigerian Breweries cut debt. International Breweries, the second-largest brewer increased its debt from N110.6 billion to N113.6 billion making it one of the highest borrowers on the stock exchange. Most of the company’s loans are dollar-denominated and obtained from CitiBank, New York.

Nigerian Breweries cut its debt by about 25.3% to N68.2 billion by financing it from working capital suggesting it paid down its loans at the expense of trade creditors. This is also a basic treasury strategy utilized by large multinationals with sound credit ratings among suppliers.

Brewery companies appear to have turned the corner in 2021 with all three recording a boost in revenues generated from selling more volumes while also increasing price. Though margins remain a challenge, it appears they make enough to settle their debts amidst the competition and higher liquor costs.

Energy companies

Two of the major energy companies, Notore Chemicals and Seplat reported higher debts portfolio as of June 2021 compared to December 2020. Seplat saw its debt balloon to N309.7 billion from N265.3 billion while Notore added about N8 billion to its debt to take it to N123.26 billion. For Seplat, its debt to equity ratio is a manageable 0.46, though it spends N46 of every N100 generated from operations on servicing debt. Notore is in a more precarious situation with a debt to equity ratio of 2.61 and is almost certain that the company will raise equity sooner, rather than later. The company’s finance cost of N8.4 billion in the last two quarters is more than its revenue of N5.3 billion in this same period. Other smaller oil and gas firms like Ardova, Conoil and Total also recorded higher debt borrowings in June compared to December. Downstream oil and gas companies typically fund their operations with debt.

Conglomerates

Transcorp and UACN, two of the major conglomerates in the country also loaded up debt in the period under review. For example, Transcorp increased its debt profile from N119 billion in 2020 to N125 billion by June 2021. The company’s debt is now more than its Net Assets. UACN also increased its debt from N4.5 billion to N17.5 billion despite selling its real estate arm to Custodian Insurance Plc. Despite the rise, profits have not been negatively affected. The duo has reported higher profits rise, more than 600% to about 7 billion.

Bottom line

The information suggests the tactics for dealing with debt vary across sectors. However, companies within the same sector have adopted the same strategy for debt. Apart from a few companies, the rest have avoided the negative impact debt has on profits, with some going ahead to even post higher returns on average equity.

Finance cost has been cheap for these businesses, allowing them to tap into a mix of bank debt and long and short term debt securities to finance operations. Also noteworthy is that those who paid down their debts, did so from cash flows generated from the business rather than raise equity.

{kind=link}

Very detailed breakdown. pls keep giving information like this, it’s very helpful in stock picking.