Follow Us on Google Discover

Follow Us on Google Discover

Nigeria’s economic trajectory under President Bola Tinubu over the past three years has been defined by sharp macroeconomic adjustments, policy shocks, and gradual stabilisation.

The administration inherited an economy struggling with weak growth momentum, rising inflation, FX distortions, and fragile external buffers.

In response, major reforms, fuel subsidy removal, FX market unification, and aggressive monetary tightening, triggered a re-pricing phase across key economic variables.

These reforms produced mixed outcomes. On one hand, they restored investor confidence in some areas, improved capital inflows, strengthened reserves, and supported trade surpluses.

Also Read

On the other hand, they intensified short-term inflationary pressure, weakened household purchasing power, and increased debt servicing costs due to currency depreciation. The result is a complex economic picture defined by adjustment pain and gradual macro stabilisation.

Across 12 key indicators ranging from public debt and inflation to FX, reserves, capital flows, and GDP, the data reveals a three-phase story – initial shock and repricing (2023), adjustment and volatility (2024), and early stabilisation with selective recovery (2025–2026). Together, they reflect an economy in transition rather than one in equilibrium.

The 12 charts that captures the President Tinubu’s 3 years

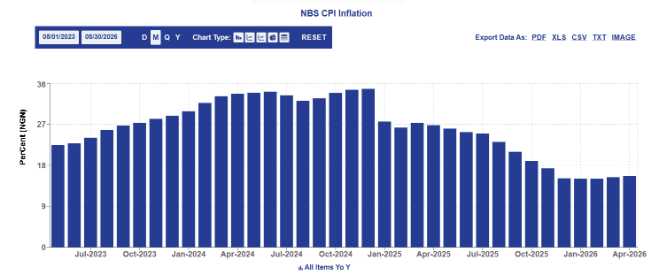

Inflation

Inflation rose from 11.2% in 2019 to 21.3% in 2022, then accelerated further to 28.9% in 2023. The Tinubu era saw a peak of 34.8% in Dec 2024, driven by subsidy removal, FX depreciation, and supply shocks.

Food inflation hit nearly 40% in 2024, severely weakening real incomes and consumption demand. Core inflation also remained elevated, reflecting broad-based price pressures.

Following CPI rebasing in 2025, inflation eased to about 15.1% by Jan 2026, though partly due to statistical adjustments and base effects rather than purely underlying price stability.

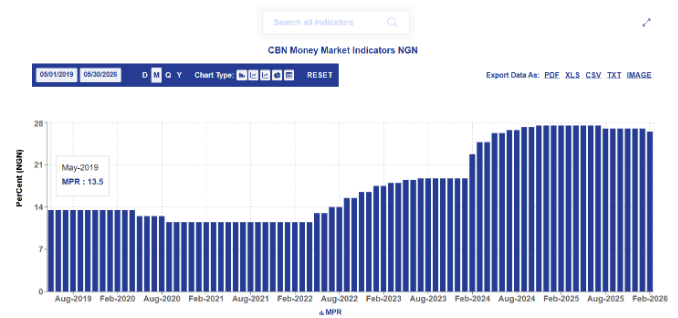

Monetary Policy Rate (MPR)

The MPR was stable at 13.5% pre-2020, before easing to 11.5% in 2021–2022. Tightening began in 2022 and accelerated sharply thereafter.

Under Tinubu, rates rose aggressively to 27.5% by 2024, remaining elevated through 2025 before easing slightly to 26.5% in 2026.

This reflects a strongly hawkish stance aimed at controlling inflation amid FX instability.

The monetary policy has prioritised price stability over growth support, tightening financial conditions significantly.

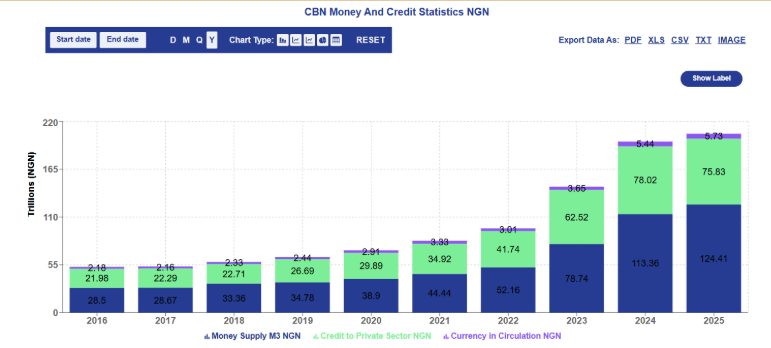

Money Supply

Money supply (M3) expanded from N34.9tn in 2019 to N55.7tn in May 2023, then surged to N124.99tn by April 2026.

The sharpest increase occurred in late 2023 to early 2024, despite rising interest rates, indicating strong liquidity expansion.

Private sector credit also rose to nearly N94.6tn by 2026, though unevenly distributed.

Despite aggressive rate hikes, liquidity in the economy has continued to expand, reducing the effectiveness of efforts to curb inflation.

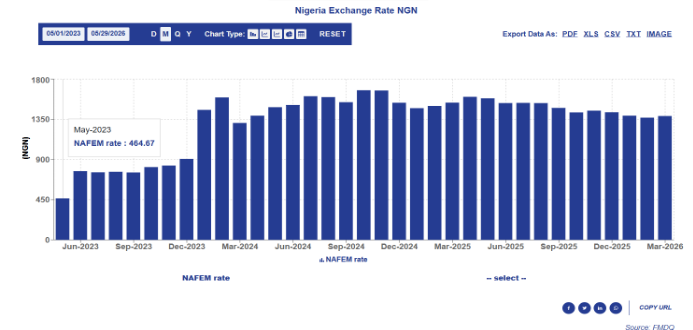

Exchange Rate

The naira depreciated sharply from N462/$ in Apr 2023 to over N1,500/$ in Mar 2024, reflecting FX liberalisation and initial market repricing.

From mid-2024, the rate stabilised between N1,480–N1,650/$, before gradually improving to about N1,363/$ by Apr 2026. This reflects improved FX inflows and policy adjustments.

Parallel market premiums narrowed over time but remained elevated, signalling lingering FX fragmentation.

The naira experienced a sharp decline after the FX reforms, but has since become more stable and has recovered some of its losses.

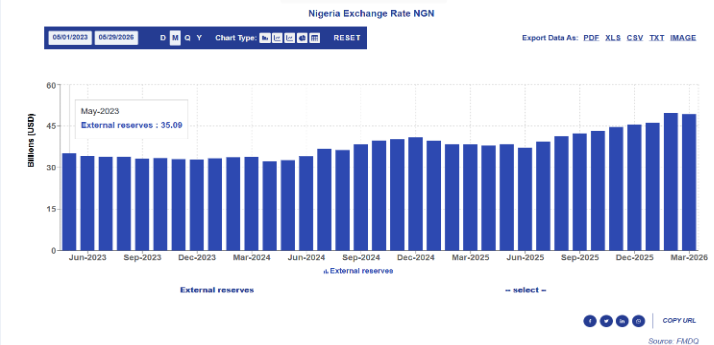

Foreign Reserves

Reserves declined from $35bn in early 2023 to $32.8bn by Dec 2023, reflecting FX pressure and debt service outflows.

A recovery began in 2024, with reserves rising to $40.9bn by Dec 2024, supported by higher oil receipts and capital inflows.

By 2025–2026, reserves strengthened further, reaching about $49.8bn by Mar 2026, marking a sustained accumulation phase. The exchange rate first fell sharply, then became more stable, and has since shown some recovery.

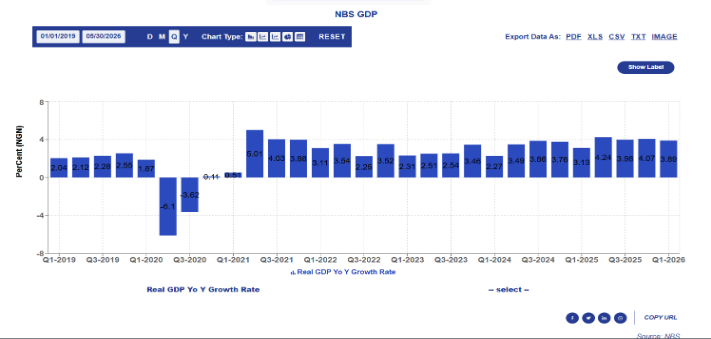

Gross Domestic Product (GDP)

GDP contracted by -1.92% in 2020, rebounded to 3.4% in 2021, and stabilised at around 3.1% in 2022. By 2023, growth averaged 2.74%, with late-year improvement.

Under Tinubu, growth strengthened modestly to 3.38% in 2024 and 3.87% in 2025, with quarterly acceleration peaking at 4.23% in Q2 2025. This reflects gradual recovery despite macro tightening.

Services and non-oil sectors provided the main tailwind, while inflation and FX volatility remained headwinds. Growth remains positive but below potential.

Overall, the economy shows steady but it has not yet experienced a strong surge in growth.

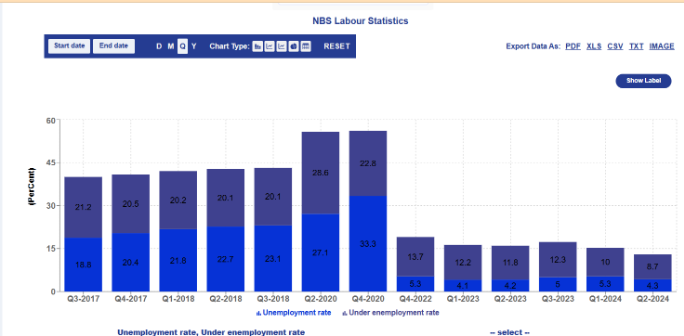

Unemployment rate

Unemployment fell sharply from 33.3% in Q4 2020 to 5.3% in Q4 2022, reflecting post-pandemic recovery and methodological adjustments. By early 2023, it had eased further to 4.1%, indicating a relatively tight labour market entering Tinubu’s tenure.

Under Tinubu, unemployment rose slightly to 5.3% by Q1 2024, showing mild labour market softening. This was driven by cost pressures from subsidy removal and FX reforms, which affected business margins and hiring capacity.

The increase has been gradual rather than abrupt, suggesting resilience in job absorption but weakening momentum in job creation. Sectors exposed to FX and energy costs showed the most strain.

As of Q2 2025, the National Bureau of Statistics (NBS) has yet to release an updated unemployment figure.

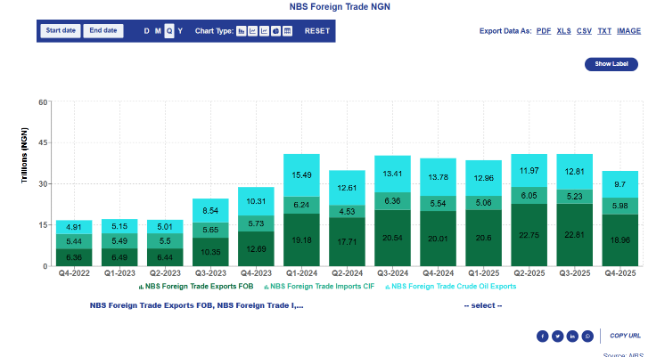

Foreign Trade

Trade balance shifted from volatility to strength. Between 2020–2022, Nigeria frequently recorded deficits, but conditions improved sharply in 2023 with surpluses rising to N3.64tn in Q4 2023.

Under Tinubu, surpluses widened further, peaking at N6.95tn in Q2 2024, driven by strong export growth and FX adjustments that moderated imports in real terms.

Exports rose from N6.49tn in Q1 2023 to over N22.8tn by Q3 2025, with crude and non-crude exports both expanding. Non-oil exports grew strongly, signalling early diversification.

Trade performance has been a major external strength, supported by FX reforms and stronger export growth.

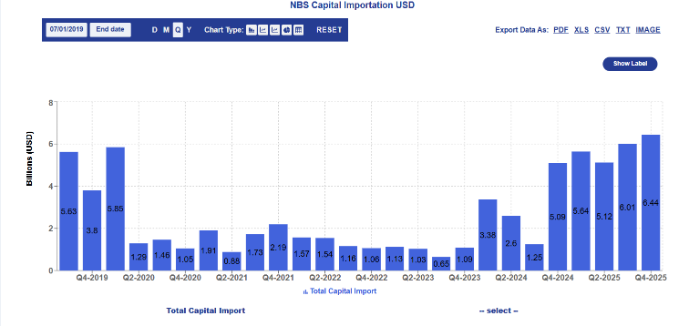

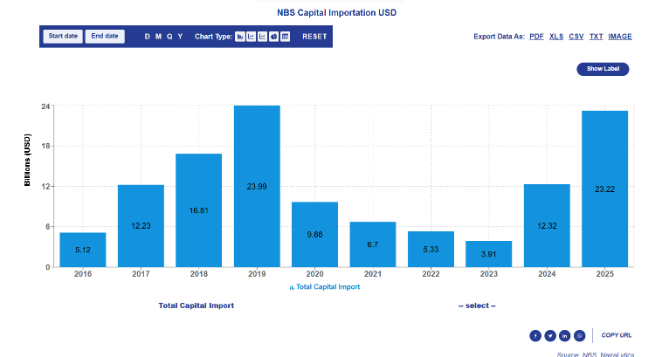

Capital importation

Capital inflows collapsed to $654.7m in Q3 2023, one of the weakest levels in years. FPI declined sharply due to FX uncertainty. Under Tinubu, inflows rebounded strongly, rising to $6.44bn by Q4 2025, driven mainly by portfolio investments.

FDI remained weak, indicating limited long-term investor confidence despite macro improvements.

Capital importation shows a strong financial market recovery, but not yet a structural investment boom.

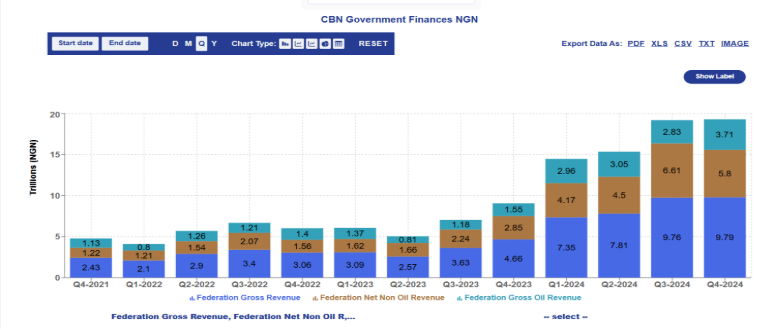

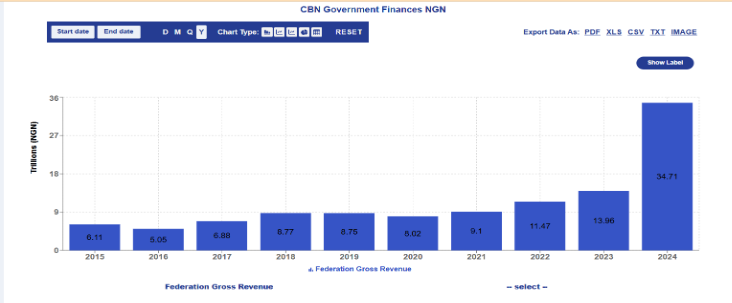

Government revenue

Federal Government revenue increased significantly under the Tinubu administration, supported by fiscal reforms, improved tax collections, and stronger oil earnings.

Gross revenue rose from N987.6 billion in June 2023 to N3.74 trillion in December 2024, an increase of about 279%. Revenue collection gained momentum throughout 2024, with monthly receipts consistently above N2 trillion and exceeding N3 trillion in several months.

Non-oil revenue remained the largest contributor, rising from N749.3 billion in June 2023 to N1.96 trillion by December 2024. This reflects stronger tax, customs, and other non-oil collections, reducing the government’s reliance on crude oil receipts.

Oil revenue also improved sharply, increasing from N238.3 billion in June 2023 to N1.79 trillion by December 2024, supported by exchange rate adjustments, higher oil prices, and improved remittances.

Revenue performance strengthened considerably, driven by growth in both oil and non-oil sources. However, rising debt service costs continue to limit the fiscal benefits of higher collections. The government budget has been in deficit, with expenditure exceeding revenue in recent years, necessitating increased public borrowing.

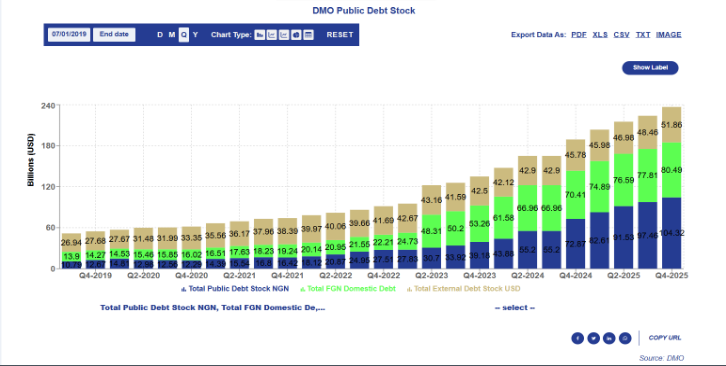

Public Debt

President Bola Tinubu has borrowed about N71.89 trillion from Q3 2023, taking total public debt to N159.28 trillion ($110.97bn) by end-2025. This represents a 116.57% increase compared to the Buhari second-term borrowing level of N61.67 trillion. External debt rose from $43.16bn to $51.86bn, while domestic debt also expanded sharply, amplifying fiscal pressure.

Total public debt rose from N87.91tn (Q3 2023) to N159.28tn (Q4 2025), driven largely by early reform shocks. The sharpest acceleration occurred between Q4 2023 and Q1 2024, where debt jumped over N24tn, reflecting subsidy removal and FX liberalisation impacts.

By 2025, quarterly debt growth slowed significantly, suggesting some fiscal consolidation. However, domestic debt expansion to N80.49tn remains a key constraint, tightening liquidity in the fixed income market and increasing sovereign exposure risk.

Overall, debt growth reflects a front-loaded expansion cycle followed by moderation, but at significantly higher levels than previous administrations.

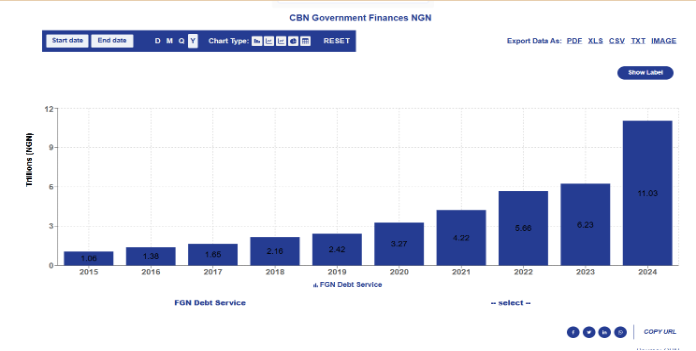

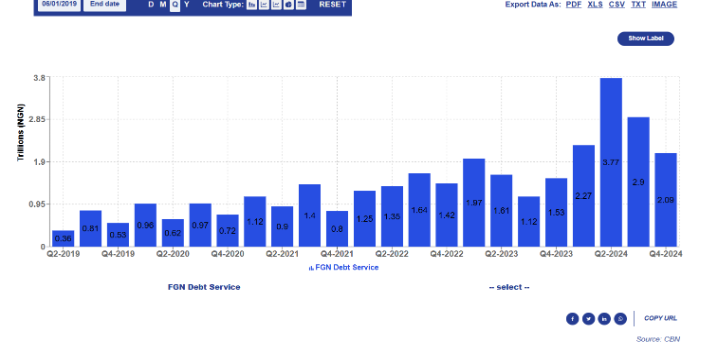

Debt Servicing

Debt service rose sharply from N1.24tn in Q1 2023 to N4.86tn by Q4 2025, nearly a fourfold increase. The sharpest jump occurred in Q3 2023 (N2.84tn) following FX reforms.

From 2024 onward, debt service remained consistently above N3tn per quarter, peaking at N4.75tn in Q1 2025. This reflects higher refinancing costs and FX depreciation impact.

Exchange rate weakening was the key driver, significantly inflating external debt obligations in naira terms.

Debt servicing now consumes a significant share of government revenue, reducing fiscal space for other expenditures and limiting budget flexibility.

What you should know

The Tinubu economic story is not linear, it is transitional. The data shows an economy that absorbed major reform shocks in 2023, adjusted through volatility in 2024, and is now showing early signs of stabilisation in 2025–2026.

Key strengths include improved capital inflows, stronger trade surpluses, rising reserves, and modest GDP recovery. However, these gains are balanced by high inflation, elevated debt service, FX volatility, and weak structural production growth.

In summary, Nigeria under Tinubu is best described as an economy in macroeconomic rebalancing, that is stabilising but not yet fully transformed.

Some things to watch out for

1- GDP growth above does not factor in the post NBS rebasing GDP. In Q4 of 2022 it was 4.32%.

2- Some of the revenue increases, in real terms are not really increases due to value loss.

3- The biggest propelling force behind trade surpluses is Dangote. This means the foresight of those who backed it should not be forgotten and PBAT should be commended for not allowing forces to close it down.

4- Tinubu inherited an economy that had just come out of the biggest economic collapse since 1929. Unfortunately, many economists fail to Frame Covid collapse into the picture.

The recovery efforts are welcome, but we hope they do not end up like the IBB reforms of 1986.

It took IBB five years to admit that the reforms were not working.

Our prayer is that PBAT will recalibrate quickly.

How?

The idea that intervention is bad should end with Wale Edun.

Tinubu should revert to his default, as captured in his article the Jonathan Tax in 2012.

Intervention, monetary policy, ways and means etc were tools he favored and are still useful tools.

Even subsidy is a useful tool. It needs to be recalibrate, not cast away.

Let’s learn from China

Decades of

Currency controls

Export controls

Subsidy

Unprecedented money printing, more than US and EU combined.

Market controls

Protection of local industries

Everything the liberal economists advice against.

Yet producing the highest growing economy in human history.

China refused to buy into liberal arguments, and invested in productive capacity.

Tinubu argued in the past that no country depends on foreign investors to grow. He was right. Foreign investors are complintary.

Dangote built the largest factory in Nigerian history when the investors were not coming so much.

That’s a pattern.

President Tinubu should use ways and means and push trillions into manufacturing and agric. Build production capacity. Clean it up and use it. Let manufacturers not need to worry about borrowing to grow.

Subsidize power for industry and production. Give people money to do business. Don’t worry about success rate, focus on long term impact.