Follow Us on Google Discover

Follow Us on Google DiscoverThe year 2023 proved to be another rollercoaster year for Nigerian fixed-income markets. Indeed, the year was going to be another inflexion point as the general elections marked the end of the eight-year presidency of Muhammadu Buhari.

The incoming Tinubu administration moved to change things quickly with big increases in petrol prices, the dismissal of the erstwhile CBN governor (Godwin Emefiele) and the removal of the hard peg on Naira trading within the official FX market, which led to a 40% weakening of the currency in June.

In the months that followed, the Naira would lose over 57% of its value in nominal terms (around 20% in real terms) to post its worst year since 1995 and inflation would accelerate to 28%, the highest since 2005.

In terms of fixed income markets, rates across the Naira yield curve climbed on average around 128bps in 2023, driven by sell-offs across the entire curve: front-end (+175bps), middle (+80bps), and long-end (+170bps).

Also Read

The lift-off in rates was driven by a strong repricing on the one-year +350bps) which followed the sale of OMO bill sales by the CBN at yields of 20-21% beginning in Q3 2023.

However, yields retraced strongly in December with the 1-yr trading at effective yields of 12-13% after rising to 17.5% levels in November reflecting a pull-back in CBN liquidity management and as the Debt Management Office closed out its 2023 borrowing cycle after reaching its targets in early December.

From a price perspective, total returns on Nigerian bonds using the S&P/FMDQ bond index came in at 8.1% (2022: 7.8%) with most of the price gains concentrated in December.

Figure 1: Naira Yield Curve

Source: Bloomberg

• Despite policy tightening, Naira depreciation drives above-target expansion in money supply: Looking at monetary aggregates, available data through September reveals strong growth in Broad Money (M3) (+38.4%, annualized) relative to CBN’s target of 28% (2022: +19%) despite the pursuit of contractionary monetary policy.

If anything, the tightening stance over H2 2023 merely helped dampen the robust pace of monetary expansion in the first half of the year when M3 expanded as high as 49% in June 2023.

The rapid increase in money supply reflects a surge in net domestic assets, NDA (up 52%, annualized), relative to a contraction in net foreign assets, NFA (down 86%).

The growth in NDA largely reflected strong credit growth across the public sector (+51% annualized to NGN34.1trillion) and private sector (+54% to NGN58.6trillion) driven by the record fiscal deficits in the former and the translation impact of the NGN depreciation on USD loans in the latter.

Despite stronger oil prices and improving oil production, the steep declines in net foreign assets relative to more modest declines (down 12% to USD32.8billion) in Nigeria’s FX reserves reflects the huge overhang of external foreign liabilities comprising large cross-currency swaps (USD21billion) and USD forwards (USD7billion).

The expansion in money supply comes in the face of higher direct liquidity sterilization via CRR debits as cumulative CRR debts stood at NGN16.7 trillion at the end of September 2023, up from NGN13 trillion at the end of 2022.

• CBN returns to liquidity sterilization but balance sheet matters complicate efficacy of tightening measures: In terms of actual securities supply, after three years of reducing the size of its ‘public’ Open Market Operations (OMO) bill portfolio, the CBN returned to active liquidity management with net issuance of OMO bill to the tune of NGN658billion which compares with the pattern of large redemptions in the prior three years (2022: NGN1.3trillion, 2021: NGN4.5trillion and NGN6.03trillion in 2020) which left the total outstanding stock of public OMO bills at NGN1.2 trillion, the lowest level in nine years.

I use the distinction between public and private OMO bills as following the release of the long-delayed CBN audited financials, it was revealed that the CBN had a much larger OMO bill stock (NGN10trillion) which reflects off-market OMO bills issued to banks and other counterparties instead of the famous cross currency swaps.

The huge liabilities running at elevated interest rates appear to have been the main confounding factor to effective monetary policy as the associated costs raised the risk that the CBN would run a loss.

As I flagged in my note on Nigeria’s central banking, this is the main drawback to asset-driven central banks as effective sterilization of excess liquidity required a profitability trade-off which underpinned CBN’s preference for reserve requirements as the key tool for monetary policy.

How the CBN navigates this trade-off, in my view, will be key in viewing policy credibility over 2024.

• This leaves elevated government borrowings as the main driver of higher yields: The relatively tame CBN liquidity sterilization implied that something else pushed Nigerian yields to record levels in September-November 2023.

In my view, this reflects a return to aggressive borrowing by the DMO late in the year with a ramp-up in sales of Nigerian Treasury Bills (NTBs) where gross issuance climbed to NGN5.8 trillion (compared to NGN4.7 trillion in 2022).

Adjusted for maturities, the DMO effectively borrowed NGN1.3 trillion largely over November 2023 reflecting a desire to hit borrowing targets. In a similar vein, gross bond sales climbed 103% to another annual record of NGN6.2 trillion, including NGN350 billion in sukuk sales.

Adjusted for the April 2023 bond maturity, net bond sales were a record NGN5.5 trillion (compared to NGN2.6 trillion in 2022).

A point to note is that these borrowings were largely financed by domestic investors which speaks to the understated depth and scale of Nigeria’s local debt markets.

In line with rising interest rate trends, the average stop rates on bond sales during 2023 climbed to 15.3% compared to 13.05% in 2022.

However, despite the rise in nominal yields, the acceleration in inflation means that NGN bond yields remain expensive, given the persistence of wider negative real yields (-1273bps compared to -760bps at the end of 2022).

Figure 2: Monetary policy and market interest rates

Source: CBN, FMDQ

• Fiscal and monetary influences to drive bear flattening: Looking ahead to 2024, developments across Nigeria’s debt markets will remain linked to lingering issues in the FX market.

Monetary policy should remain tight to cultivate portfolio flows to bolster USD supply on one hand, while sterilizing Naira liquidity to curb USD demand on the other.

Fundamentally, inflation will likely remain elevated (25-30% region) as fuel and FX shocks continue to propagate over H1 2024, though large base effects will anchor a deceleration towards 20-25% over H2 2024.

• While the CBN should remain hawkish, as I noted in my piece on Nigerian central banking, the key question for an asset-driven central bank like the CBN is how to credibly sterilize liquidity without running unsustainable losses.

To credibly signal to fixed-income markets that it wants Naira interest rates to remain elevated, the CBN must essentially sterilize ALL excess liquidity from the banking system.

There are three means to carry out this effectively: elevated open market operations (OMO) bills (potentially at >20% rates), aggressive hikes in the MPR which raise the SDF (well above 20%) or scorching increments in cash reserve requirements towards 50%.

The problem with the first two approaches is that CBN’s large private OMO bill securities issued as the opposite leg of its cross-currency swaps to Nigerian banks have greatly constrained its balance sheet.

Thus, the likely preference is for low-cost liquidity management options. This leads to my guess that the choices facing the CBN are to either ramp up the scale of ad hoc CRR debits or return to the Sanusi-era public CRR at a high level (75-80%).

Anything absence of this or aggressive hikes in OMO activity and discount window rates will result in non-credible liquidity management.

As we saw in December, this will lead to declines in rates when the CBN turns passive to any build-up in system liquidity.

Overall, I think the CBN will remain in a hiking cycle over H1 2024 with potential 100-300bps increases in policy rates alongside a less tolerant view on system liquidity wherein adhoc CRR will be deployed to fix with the occasional OMO auctions to signal rate levels.

This is a tacky approach but unless the underlying balance sheet issues are addressed and there are significant improvements in organic USD flows, a muddle-through liquidity tightening is what we will get.

On the fiscal side, the proposed 2024 budget calls for NGN6.06trillion in local borrowings which alongside refinancing of 2024 bond maturities of NGN720billion (March 2024) and large NTB refinancings of NGN6.2trillion speaks to a potentially heavy fiscal securities issuance over the year.

The closure of the W&M financing used by the prior Buhari administration suggests that these borrowings remain market-driven.

It is important to clarify that the recent securitization of an additional NGN7 trillion in Ways & Means wraps up the legacy Buhari era overdrafts. Using CBN data through June 2023, W&M overdrafts stood at NGN30trillion at the end of May 2023 implying that the recent move reflects the outstanding portion and not new securitizations.

In the usual manner, FGN borrowings are likely to be front-loaded given the large maturity in March. In terms of target bond tenors for 2024, the debt borrowing plans are likely to remain focused on 4-bonds on offer with re-openings along the 5-year, (FGN 2031), 10-year (FGN 2033), 15-year (FGN 2038), a potential return to the 25-year bucket via a new bond (FGN 2044) and the withdrawal of the 30-yr bond which markets appear to be pricing given the reaction in the 2053s following the December auction.

Figure 3: Nigeria’s Annual FGN Bond Maturity Profile (NGN’bn)

Source: FMDQ

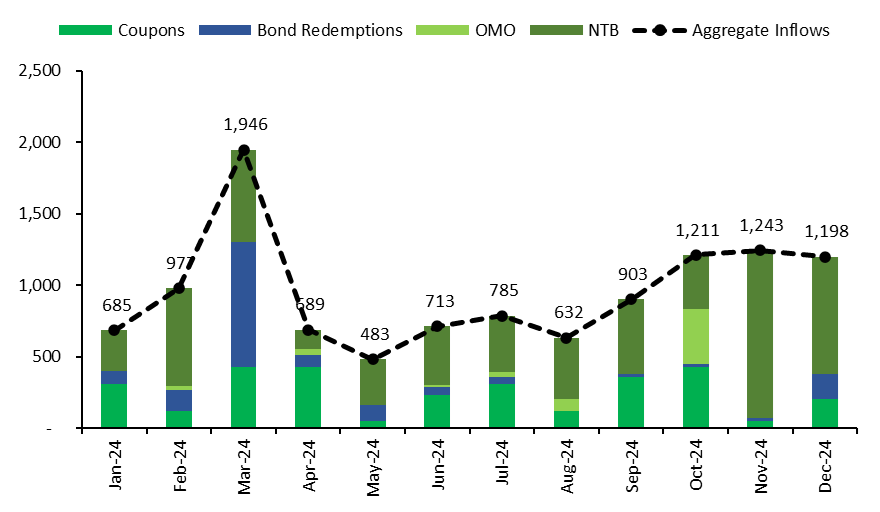

In terms of potential liquidity flows, I estimate that monthly maturities (including Bond coupons, OMO and NTB) over 2024 will average NGN955billion (vs NGN676billion in 2023, NGN620billion in 2022 and NGN720billion in 2021).

On the supply side, my guess is that monthly securities supply (incorporating the FGN debt plans and NTB/OMO refinancings) will likely average NGN1.2 trillion (2023: NGN826 billion) which exceeds system maturities. On balance, my sense is that there will be an excess of securities supply over potential demand for paper which is fundamentally supportive of higher interest rates over 2024.

How high rates go will be determined by the interplay between how hawkish the CBN approaches excess liquidity in trying to signal higher rates (likely in H1 2024) and how desperate the DMO is to meet its FGN borrowing target.

This suggests similar bearish conditions when any overlap occurs such as over Q2-Q3 2024 in a reprisal of the September-November 2023. Overall, a bear flattening over the year is my call.

Figure 4: Maturity profile over 2024 (NGN’ million)

Source: CBN, FMDQ

If you would like to receive this every week as well as other posts or you know someone who will find the information on this site useful, you can add your email using the subscribe button below

Id Like to receive the weekly reports