The Nigerian economy grew by 2.54% year-on-year (y/y) in Q3 2023, higher than the 2.25% recorded in Q3 2022. Over the last decade (2013 – 2022), Nigeria recorded an average annual real economic growth rate of 2.4%; same as the estimated population growth of 2.4%.

A 2.4% annual real Gross Domestic Product (GDP) growth rate is clearly below what Nigeria needs to address the multidimensional macroeconomic challenges confronting the nation.

President Tinubu’s administration intends to double the size of Nigeria’s GDP from an estimated $535.34 billion as of 2022 to $1 trillion by 2030.

This report examines the range of annual GDP growth the country should aim at to achieve meaningful economic progress over the next decade.

What economic growth rate does Nigeria need to attain?

There is no gainsaying that Nigeria needs to achieve a higher growth rate that is inclusive, private-sector-driven, non-inflationary and non-oil sector-led.

How the country intends to achieve this will depend on the policy priorities of the new administration and the support of all Nigerians.

A look at the economic growth trend of some notable economies that have attained some level of economic development reveals that they were able to sustain between 5% to 10% GDP growth for decades.

We consider a 5% – 7% annual real GDP growth as the minimum Nigeria should realistically target in the next decade. Our analysis shows that sustaining this growth rate should deliver a $700 – $800 billion economy by 2033. To achieve a $1 trillion economy by the year 2033, the country needs to achieve and sustain a 6.5% minimum average GDP growth rate.

We consider a 5% – 7% annual real GDP growth as the minimum Nigeria should realistically target in the next decade. Our analysis shows that sustaining this growth rate should deliver a $700 – $800 billion economy by 2033. To achieve a $1 trillion economy by the year 2033, the country needs to achieve and sustain a 6.5% minimum average GDP growth rate.

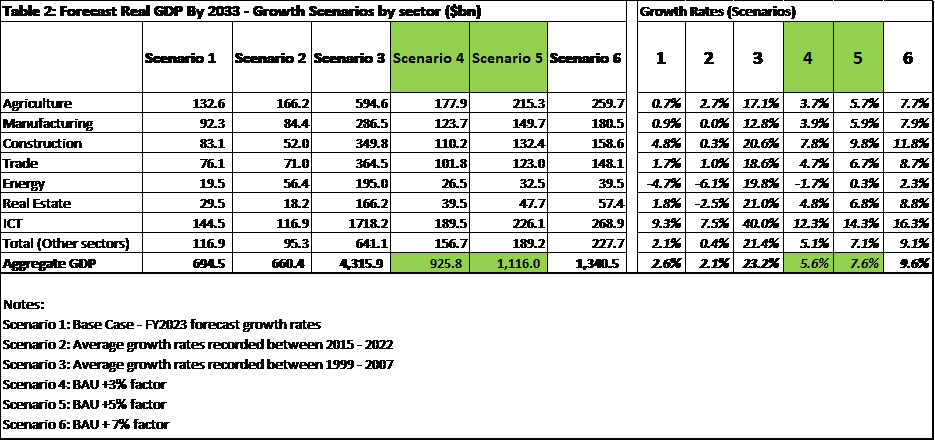

Scenario Analysis – Real GDP by the year 2033

We took a bottom-up approach to see how growth in key economic sectors can drive desired aggregate GDP growth over the next decade under six scenarios.

Source: Verraki Research

Our base-case scenario assumes that the macroeconomic conditions over the next decade will be like the year 2023. Our analysis shows the Nigerian economy will achieve 2.6% average growth over this period and deliver a $694.54 billion dollar economy by 2033.

Call to Action – the role of government and policymakers

We highlighted some short and long-term policy priorities that may help.

In the short term, the government must stabilize the economy in terms of physical security and safety, address inflation, optimize quick wins, and communicate strong political will to act.

The government must immediately address the issue of oil theft which has continued to weaken revenue generation.

There is a need to expand our tax net and boost efficiency in tax collection through better use of digital technologies to strengthen revenue administrations.

There is equally a need to urgently address the depreciation of the Naira and volatility in the foreign exchange market.

To sustain growth in the long term, the government needs to continue the roll-out of visionary infrastructure projects that will support economic diversification, broad-based growth, and better quality of life.

Collaboration with the private sector through public-private partnerships and strategic de-risking should stimulate the deployment of private capital and expertise to strategic economic sectors, particularly Agriculture, ICT, Manufacturing and Services.

{kind=link}