Follow Us on Google Discover

Follow Us on Google Discover

Earlier this year, the CEO of Guaranty Trust Bank Plc, Segun Agbaje, disclosed ongoing plans by the tier-1 bank to switch to a holding company structure. Apparently, there are other financial services, besides core banking, that are now quite profitable. As Nairametrics reported, Agbaje explained that GTBank will not be left behind as the new wave of Nigerian banking gradually takes effect. Therefore, the bank will fully take advantage of these other profitable businesses by diversifying into a holding company structure.

Note that when Agbaje made this disclosure in March, Nigeria was yet to really feel the impact of the COVID-19 pandemic. Now, Fast-forward to May 2020 and it is a different story altogether. As Nigerian banks continue to grapple with the negative impacts of the pandemic, some experts have opined that those with diversified operations are better-positioned to excel. However, it is not as straight-forward as it seems, as you shall see shortly.

READ ALSO: Ratings firm explains why bank non-performing loans could be worse than expected

Understanding the situation; A quick overview of Nigerian banks amid COVID-19

The COVID-19 pandemic has birthed a new era of Nigerian banking where banks will have to be a lot more strategic and diversified in order to excel. At a time when the economy is suffering and loans are at risk of going bad, many banks are projected to underperform in 2020. It, therefore, behooves of the banks to find viable businesses that will help them cushion the impacts of the pandemic.

Other News

As you may well know, the key assets on most banks’ books are basically loans and financial assets. For Nigerian banks whose loans are often skewed towards the oil and gas sector (about 26%), there are growing concerns over possible write-downs on loans or worst still, a sporadic jump in non-performing loans.

(READ FURTHER: GTBank Plc to consider a holding company structure)

According to Gbenga Sholotan, an Investment Analyst and Portfolio Manager who spoke to Nairametrics, no bank will be spared from the negative impacts of COVID-19. However, the impact on different banks will depend on the degree of their loan exposures and in what sectors of the economy those exposures are in. He said:

“If you have a bank whose loan book is highly-skewed towards oil and gas or commodities, then you will see a lot of restructuring or a possibility of non-performing loans in the event that there is no restructuring. So, there will be a little bit of write-down to these assets.

“For banks whose books are skewed towards consumer-lending (that is retail banking), this is also not a good time. This is because a lot of their customers are losing their jobs or even collecting half pay. And what this means is that these customers will not be able to repay their loans to these banks. And this will impact the banks.

“I really don’t think any bank will be spared. It just depends on how their loans are skewed. So, for banks whose loans are skewed towards heavy-duty industries… Let’s use an example – the cement players. If I have given most of my loans to the cement players, there’s a lockdown in Nigeria. So, no one has actually been building/constructing over the last three weeks or thereabouts. This simply means that sales will be down for the cement companies and they can only be able to repay loans with the cash they already have; if they do. If they don’t, then the banks who lent to them are also in trouble.”

Are banks with holding company structures better-positioned to survive COVID-19?

Having established that all the banks will be impacted by the fallouts of the pandemic, Sholotan went further to point out that some of them might be better positioned to survive. According to him, these are banks with holding company structures.

“I agree with your view on the holding company structure because these guys have other subsidiaries that make money for them. An example would be Stanbic IBTC where they have an asset management business; they also have a pension fund business. They will likely fare better…” Sholotan admitted.

Similarly, the head of marketing at Chapel Hill Denham, Lanre Buluro, had earlier told Nairametrics that banks with holding company structures might just have it easier compared to their competitors. According to him, banks whose business model entails more than typical banking tend to have more diversified revenue streams that help them to supplement revenue from their core banking operations. He also mentioned Stanbic IBTC and FCMB as two banks whose diversified businesses could really help during this difficult period.

Focus on bank Hold-Cos in Nigeria

In Nigeria, there are currently three banks with a holding company structure, according to information obtained from the Nigerian Stock Exchange. The banks are – FCMB Group Plc, Stanbic IBTC Holdings Plc, and FBN Holdings Plc. These companies’ subsidiaries operate in businesses outside of core banking, including asset management, pension fund administration, investment banking, insurance, stockbroking, and many more.

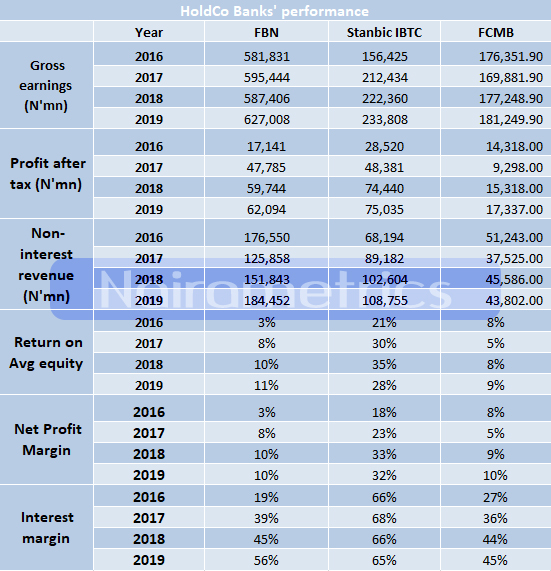

Now, it is one thing for a company to have many subsidiaries, and then something else entirely for these many subsidiaries to actually be profitable. This is why we ensured to cross-check these companies’ financial records just to see how profitable they have been over the last four years. As you can see from the table below, these holding companies’ gross earnings and profits have relatively grown consistently over the last four years. Stanbic IBTC Holdings Plc also appears to have recorded the most profits between 2016 and 2019, even though FBN Holdings Plc generated the most revenue during the 4-year period.

The table also shows the difference between these banks’ non-interest revenues and their gross earnings during the period under review.

READ ALSO: Top 10 Stockbroking firms trade shares worth N138.1 billion in January

Asides FCMB Group Plc, both FBN Holdings and Stanbic IBTC Holdings recorded significant growths in their gross earnings and profit during the 2016/2017 recession. In specific terms, FCMB Group’s gross earnings had declined by 3.8% to N169.9 billion in FY 2017, down from N176.4 billion in FY 2016. The group’s profit after tax also declined by 53.9% to N9.2 billion in 2017, down from N14.3 billion in 2016.

On the other hand, FBN Holdings Plc grew its gross earnings and profit by 2.3% and 178.8% (respectively) in 2017. In the same vein, Stanbic IBTC’s group revenue grew by 35.8% in 2017, even as profit equally rose by 69.6% compared to how much profit was recorded in 2016. This could be seen to support the argument that bank Hold-Cos are better prepared to withstand economic upheavals such as recessions. However, there is a concern…

Not all the bank Hold-Cos have strong subsidiaries

According to Dolapo Ashiru, a Financial/Capital Market Analyst who spoke to Nairametrics, not all banks with holding company structures have strong subsidiaries. Therefore, even though a holding company structure should ideally help banks to fare better, this may not really be the case for some of Nigeria’s diversified financial institutions. He said:

“Let me use the example of Stanbic. Stanbic has subsidiaries like asset management and so on. In the pension space, Stanbic IBTC’s pension subsidiary is number one. But in the banking space, are they number one? The answer is no. So, the non-banking subsidiaries of Stanbic are better market leaders than the traditional banking subsidiary. But then again, inasmuch as Stanbic IBTC Pension Managers Ltd is doing so well in the pension space, you cannot compare that with FCMB. The non-banking subsidiaries under FCMB are generally not as strong as the non-banking subsidiaries under Stanbic.

“But ideally you are right, companies that have a hold-co structure should be better prepared to do well because their income is not just purely from banking. But not all the hold-cos have very strong non-banking subsidiaries like Stanbic IBTC. I am of the opinion that GTBank will do better than most hold-cos because GTBank has, to a very large extent, been very cost-efficient. More so, GTBank’s returns on investment and assets are far better than any other bank.”

(KEEP READING: Zenith Bank CEO admits COVID-19 will severely impact banks)

But the future of banking is indeed Hold-Co

Speaking to Nairametrics, Investment Advisor and Fixed Income expert, Igho Alonge, stressed that the future of successful banking is Hold-Co. According to him, this has nothing to do with COVID-19 because prior to this time, it was already clear that banks with holding company structure were better positioned to excel. He said:

“You see the way CBN has been regulating banks… LDR is so high, CRR for some banks is above 60%. So, with this kind of tough regulation on banks, I expect that holding companies will do better. Banks that have a holding company structure will survive this over-regulation from the CBN. If you look at Stanbic, the pension arm’s contribution to the group is higher than its cost deduction from the group. FBN Holdings has been paying dividends. The bank itself has not been able to pay dividends because of its non-performing loans. So, other arms of the business have been helping to pay dividends.

“I think the future of the best banks (i.e. banks that will return more money to shareholders) by surviving this strong regulation by the CBN, will be the guys that have other businesses.”

Commenting further, Alonge argued that COVID-19 will affect all the banks, regardless of whether they are focused on core banking or diversified in a holding structure. For instance, the fact that many companies are laying off their staff means that there will be less remittance to pension funds. Also, asset management companies and investment banks will take various forms of hits from the pandemic because there will be less business for them to do.

“COVID-19 will slow down everybody’s business. It will slow down banks without hold-co, and banks without hold-co. Investment banking will suffer because there will be fewer mergers and acquisitions, PFAs will suffer because people are losing their jobs, asset management will also suffer. So, I don’t really think there is any clear-cut advantage for banks with hold-co and those without hold-co as far as COVID-19 is concerned. Also, do not forget that banks with hold-co structures are taxed twice. The subsidiaries are first taxed, and then when they remit all their profit to the group they get taxed again. So, that is a disadvantage,” he stated.

In the meantime, some tier-1 banks and banks with strong technology will excel

For now, Nigeria’s largest banks by assets and profitability (Zenith Bank and GTBank) are not Hold-Cos. As a matter of fact, some experts believe that some tier-1 banks such as GTBank, Zenith, and UBA will always do well. Also, banks with good technological innovations will equally do well. According to Lanre Buluro, “GTBank will do well because their cost structure is one of the lowest in the market.” He also cited Sterling Bank Plc, which he said has recently been very innovative with its use of technology.

For US-based Nigerian Financial Analyst, Wole Oluyemi, the survival of Nigerian banks will depend on their ability to make good use of technology in their operations. He told Nairametrics that he believes “all banks would experience some level of impacts from COVID-19 but their ability to absorb the shocks is highly dependent on their operational and IT resilience that has been built pre-COVID. So, I believe that those banks with good digital platforms (both infrastructure and deployment capability to customers) would come out of the crisis with very minimal impact.”