Follow Us on Google Discover

Follow Us on Google Discover

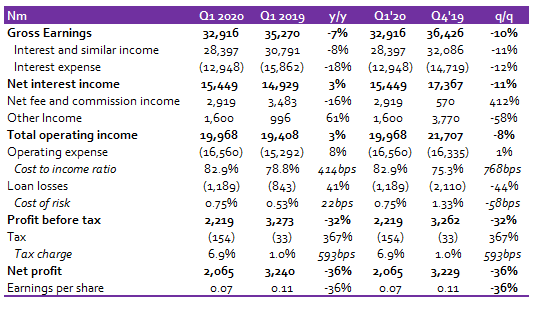

Sterling’s Q1 2020 UNAUDITED report showed a decline in Interest Income to N28.4bn, largely due to a decline in Interest Income on Loans and Advances (down 10% y/y) which mirrors the flattish growth in the loan book (Net loans to Customers declined 0.4% y/y).

Interest Expense on the other hand, declined 18% y/y to N12.9bn, despite the substantial growth in Customers Deposits (up 15% y/y), reflecting improved funding costs. Notably, CASA ratio rose to 64% in Q1 2020 compared to 60% in Q1 2019.

We expect the improvement in the bank’s deposit mix to remain supportive of lower funding cost. Overall, Net Interest Income grew 3% y/y to N15.4bn in Q1 2020.

Despite the modest growth in Net Interest Income, Pre-tax Profit declined significantly, down 32% y/y to N2.2bn in Q1 2020, due to weaker Net Fee and Commission Income (-16% y/y) and weak operating efficiency, given the increase in OPEX (up 8% y/y) compared to the increase in Operating Income (up 3% y/y).

Other News

The downward adjustment in fees on banking transactions by the CBN took a toll on the bank’s earnings, as Net Fee and Commission Income declined 16% y/y to N2.9bn.

The decline in Net Fee and Commission Income was primarily driven by a reduction in E-business commission and fees (down 10% y/y; accounted for 35% of Fee and commission income) and Other fees and commission (down 31% y/y; accounted for 32% of Fee and commission income). Going forward, we expect the bank to accelerate the deployment of its digital channels in improving the volume of transactions to partly offset the impact of the regulatory induced fee cut.

However, Other Income grew 61% y/y to N1.6bn, largely due to higher gains from bonds and treasury bills classified as FVTPL.

The bank’s Impairment Charge rose 41% y/y to N1.2bn in Q1 2020, leading to a 22bps rise in an annualised cost of risk to 0.75% in Q1 2020.

Despite the flattish loan book of the bank during the period, we believe the higher loan loss provisioning was due to the deterioration in macro conditions brought by the global pandemic. We expect the uptick in Impairment Charge to persist in the short to medium term.

(READ MORE: Access Bank Plc reports profit of N40.9 billion for Q1 2020)

Overall, both Pre-tax Profit and Profit After Tax declined by 32% y/y and 36% y/y to N2.2bn and N2.1bn respectively. Annualised RoAE moderated sharply to 7.1% in Q1 2020 compared to 12.6% in Q1 2019.

We have a BUY rating on Sterling Bank, with a target price of N2.71/s.

Operating Expenses grew 8% y/y to N16.6bn in Q1 2020. The faster growth in OPEX compared to growth in Operating Income (up 3% y/y) led to a 414bps increase in Cost to Income Ratio (CIR ex-provisions) to 82.9% in Q1 2020.

The increase in OPEX was due to higher regulatory charges emanating from AMCON charges (up 13% y/y) and NDIC premium (up 20% y/y) alongside increased Depreciation and Amortisation (up 42% y/y) arising from higher investment in computer equipment.