Follow Us on Google Discover

Follow Us on Google Discover

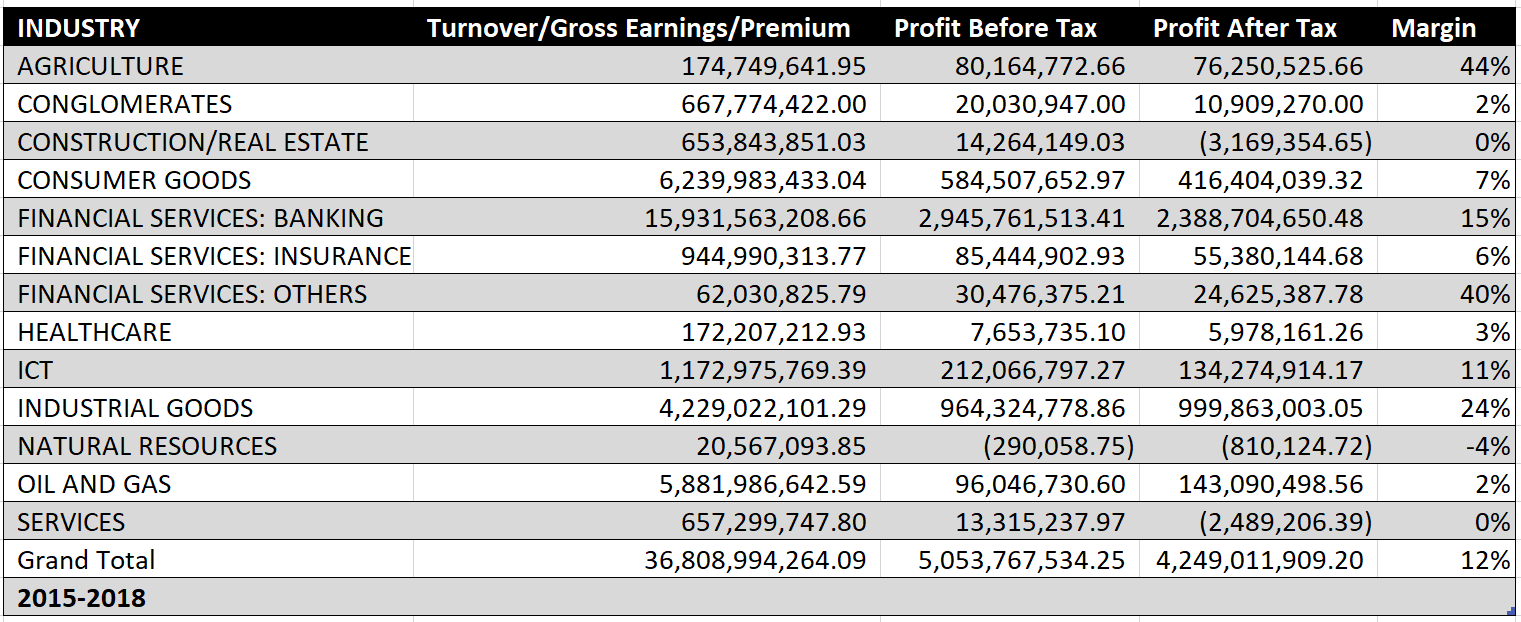

Listed companies on the Nigerian Stock Exchange posted a combined profit after tax of about N4.2 trillion between 2015 and 2018. The companies also reported tax expenses of about N804.7 billion during the 4-year period. Total revenues during this period were also N36.8 trillion. Nigeria’s President Buhari has been in office since 2015 and presided over the economy during this period.

The data looks at results released over the last 4 quarters for publicly listed companies on the Nigerian Stock Exchange for the combined years 2015, 2016, 2017 and 2018. Some of the increase in revenues recorded over the period was also a result of new listing and not necessarily due to organic growth. This is the breakdown;

Total returns

What this means: Over the last 4 years, Nigeria has suffered a drastic recession that reduced growth to an average of 2% per annum. The inflation rate has remained doggedly at double digits, while interest rates remain very high. Government revenues have also fallen significantly during the period and are now accompanied by rising debts and debt service to revenue ratio. Despite strong economic head and tailwinds, it appears that Nigerian companies have continued to perform against all odds and grow their topline revenues.

Important to note that the Nigerian Stock Exchange market capitalization of N13 trillion is about 10% of GDP and does not account for non-listed companies as well as the informal sector. However, it is an important barometer for how the economy has faired over the first 4 years of the Buhari Administration. Because the data is based on revenues from listed companies an important metric to gauge performance will be the profit margin. The data shows profit margin has risen from 10% in 2015 to 15% in 2018. This means companies have kept a higher percentage of their revenues as profits.

Also Read

[READ MORE: 5 Nigerian companies with a combined market value of 5% of Nigeria’s GDP]

Annual returns

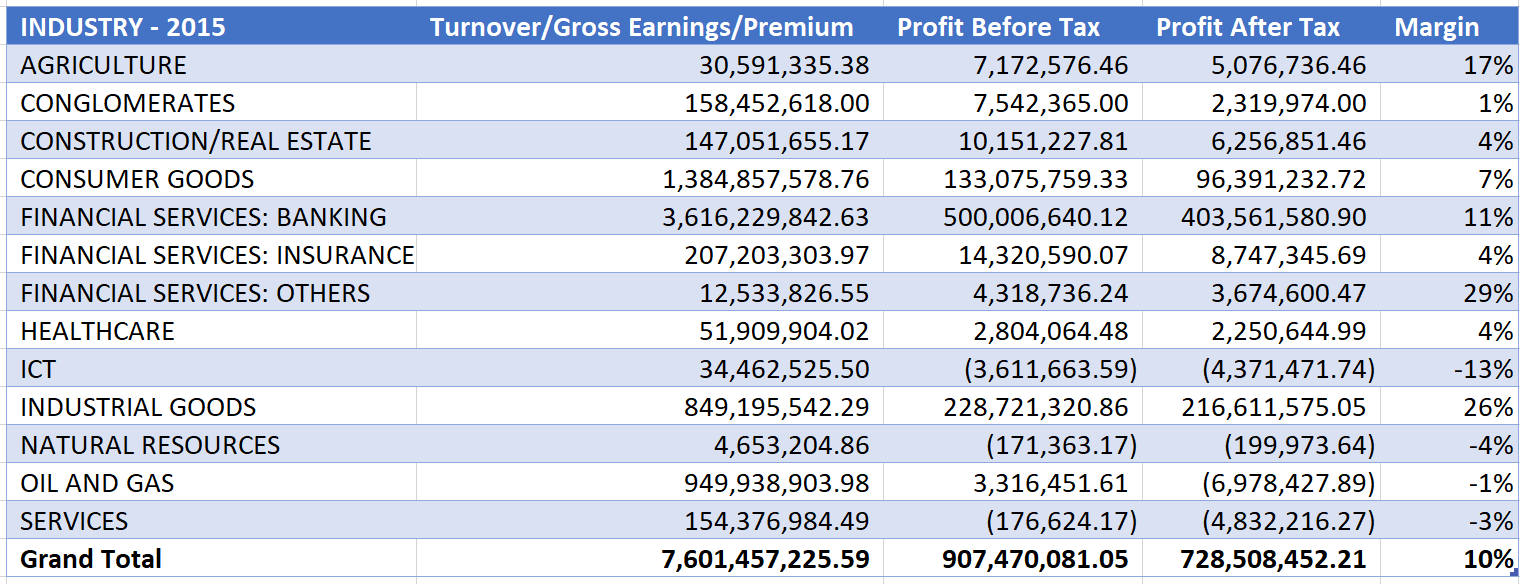

2015: Companies reported a combined profit of N728.5 billion out of a revenue of N7.6 trillion, representing a 9.6% profit margin. Revenue was dominated by the Consumer Goods and Financial Services sector with a combined N4.9 trillion. As expected banks led the way. COnglomerates continue to struggle, keeping just 1% of revenues as profits. We also see recorded losses for the ICT, OIL ad Gas and Services Sectors, in line with negative GDP recorded over the same period.

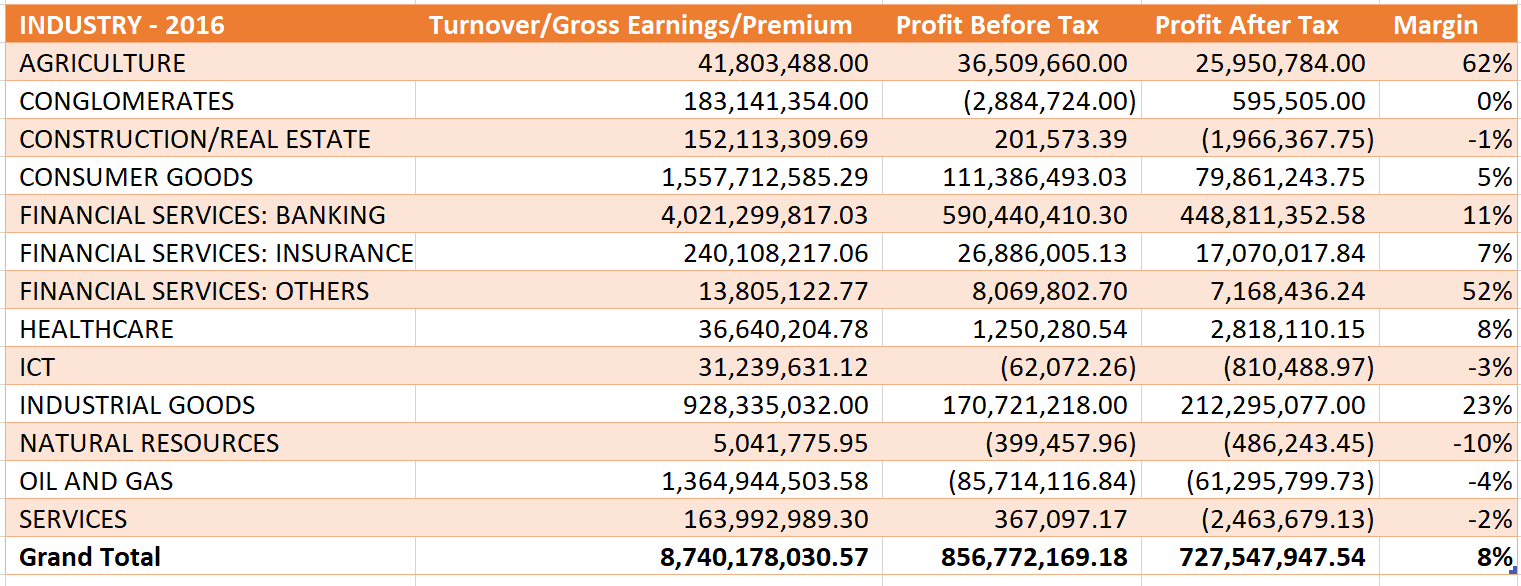

2016: This was the year Nigeria got into a crushing recession. Profit was N727.5 billion and revenues, N8.7 trillion. The total profit margin dropped to 8%. Despite the recession, Nigerian banks earned N4 trillion growing by over N400 billion year on year and accounting for much of the revenues. The construction and real estate sector joined the ICT, Oil and Gas and services sectors in recording losses.

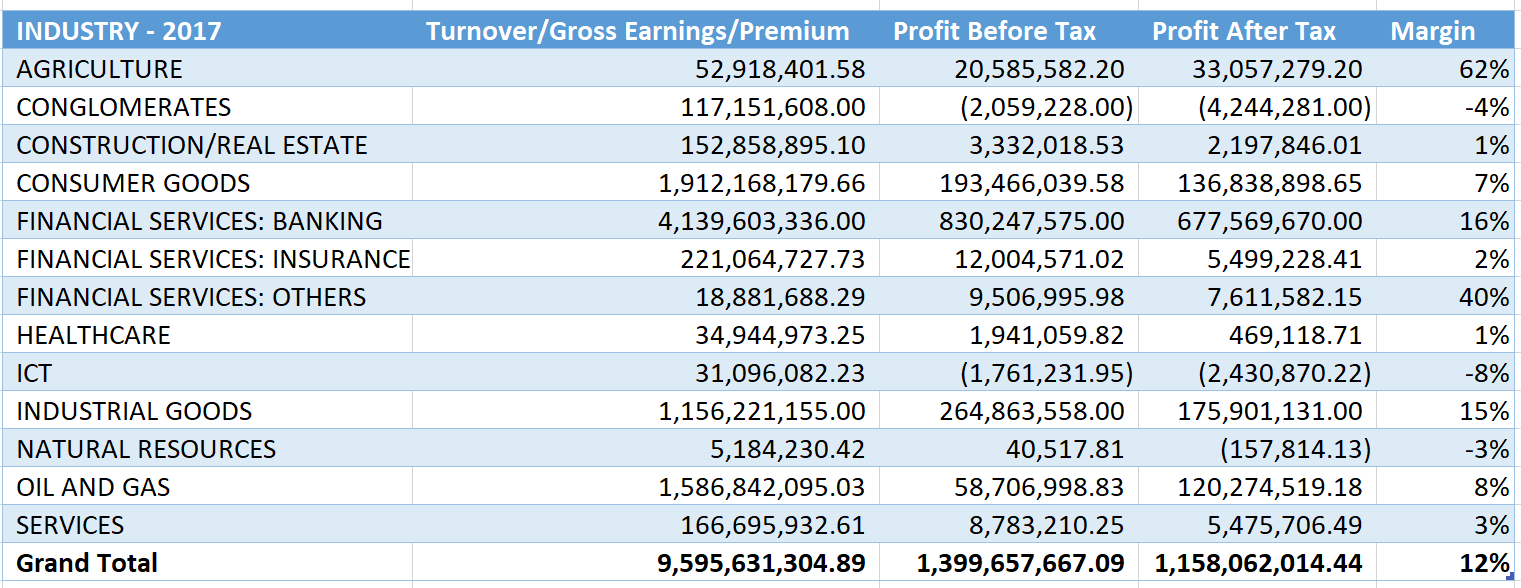

2017: Nigeria got out of recession in 2017. During the year, companies reported a total turnover of N9.59 trillion and profits of N1.1 trillion. The profit margin was 12%. Agriculture and Financial services led the way with double-digit margins. The Agricultural sector is dominated by the likes of Okomu Oil and Presco Plc.

As Nigerian climbed out of recession, Conglomerates and the Natural Resources sector joined the ICT sector with losses. We also observed that the Oil and Gas sector reported an 8% profit margin as global oil prices picked up.

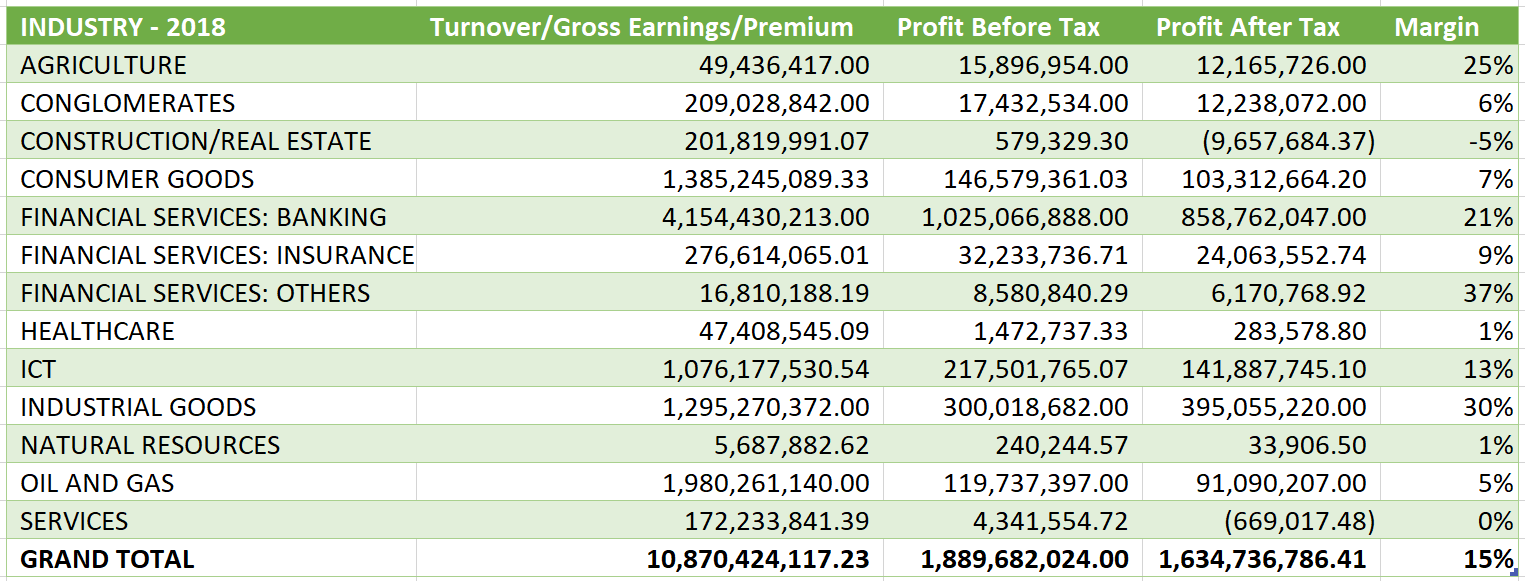

2018: Profit margin improved to N15% at the end of the financial year, with profits rising to N1.6 trillion. Total revenues also hit and crossed the N1 trillion mark, closing at about N10.8 trillion for the year under review. The banking sector alone contributed N4.1 trillion of the revenues in gross earnings. They also reported a profit margin of 21%. The industrial goods sector, dominated by Dangote Cement, also reported a profit margin of 30%.

Only the real estate sector and services reported losses during the year. The sector also posted revenues of just N201.8 billion from N147 billion in 2015 indicative of how poor growth has been for a sector typically pivotal to economic growth in many countries. The Agricultural Sector also reported an impressive 25% profit margin as Okomu Oil and Presco benefit from the government’s agro policies.

[READ ALSO: Some important tips for companies in view of Customer Service Week 2019]

The Future of Nigerian Stock Exchange

At a revenue of N10.8 trillion, Nigerian stocks revenue to GDP is about 8%, one of the lowest in the world. Stocks also have a market cap of about N13 trillion, just 20% more than its revenue (1.2x). Stocks are also priced 8x earnings based on combined profits of N1.6 trillion. We expect revenues for 2019 to be significantly higher with the listing of MTN and Airtel which could boost revenue by over N1.5 trillion.

The Nigerian Stock Exchange has struggled to attract multinationals and large corporations over the years relying on government moral suasion to achieve major listings. For example to major IOC is listed on the country’s bourse while local startups that have achieved maturity stages will rather list abroad than list in Nigeria. Jumia for example, listed on the NYSE and Interswitch is expected to list on the London Exchange. Several reasons for the lack of significant listing is mainly attributed to how shallow the stock market has been over the years.

Retail investor participation is at multi-year lows and the ever reliant foreign investors have reduced their exposure to Nigeria due to its economic policies. Company list on stock markets if they believe their valuations can be rightly priced and can attract significant liquidity and capital whenever they need to. Some analysts believe it could be incredibly onerous to raise as much as $1 billion in equities through the Nigerian Stock Exchange.