Follow Us on Google Discover

Follow Us on Google Discover

Welcome to Nairametrics‘ summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills. This is brought to you by Zedcrest.

This report is dated May 16th, 2019.

Key Indicators

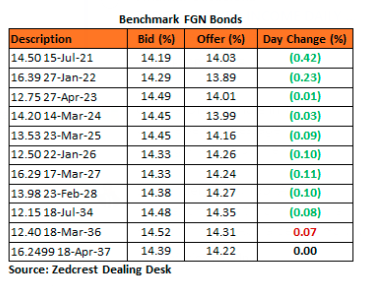

Bonds: The Bond market turned firmly bullish in today’s session with renewed client demand seeping into the bond market on the back of the continued downtrend in T-bills yields, (with the effective yield on the 1yr bill now at sub-14.00%). Yields were consequently lower by c.10bps on the day, with the most decline witnessed on the short end of the curve.

Also Read

With the recent slowdown in OMO issuance by the CBN, we expect demand interests in the market to be relatively well supported in the near term.

Treasury Bills: The T-bills market remained firmly bullish, with yields declining significantly by c.40bps owing to the absence of an OMO auction by the CBN despite the c.N107bn in OMO T-bill maturities. Some market players also sought to cover lost out bids from the previous session’s NTB auction, where rates cleared significantly lower from their previous levels.

The rates on the mid to long end of the curve are all now trading below the 12.50% mark and we expect them to remain subdued at these levels in the absence of a renewed OMO auction by the CBN.

Money Market: Rates in the money market declined further by c.5pct as system liquidity was further bolstered by inflows from OMO maturities up to c.N290bn positive. The OBB and OVN rates consequently ended the session at 5.86% and 6.57% respectively.

We expect rates to remain relatively stable at these levels, barring a renewed OMO sale by the CBN.

FX Market: At the Interbank, the Naira/USD rate was unchanged at N306.95/$ (spot) and N356.60/$ (SMIS). The NAFEX closing rate in the I&E window however declined further by 0.05% to N360.35/$, whilst market turnover fell by 70% to $152m. At the parallel market, the cash rate rose by c.0.03% to N359.10/$, while the transfer rate remained unchanged at N363.50/$.

Eurobonds: We witnessed renewed demand interest on the NIGERIA Sovereigns, with risk clearing across the curve over the course of the session, as oil price strengthened to c.$73pb. Yields were consequently lower by c.7bps on the day, with the most gains recorded on the 47s and 49s, which gained c.0.9pct on the day.

The NGERIA Corps, were relatively muted except for slight interests witnessed on the ECOTRA 21s, UBANL 22s and FIDBAN 22s.

________________________________________________________________________

Contact us:

Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

The value for inflation in the first table of this article ought to have change to its recent value, shouldn’t it?