Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price. This report is dated April 8th, 2019.

Funding For CBN Wholesale FX Auction Pressures Short Term Rates Higher

***CBN disbursed N25.4bn to facilitate non-oil exports in 2018*** – Okoroafor

Key Indicators

Bonds

The FGN Bond market traded on a relatively calm note with yields compressing marginally by c.3bps following slight buys on the short end of the curve.

We expect interests in the market to remain largely order driven in the near term, with yields expected to remain relatively stable at current levels.

Treasury Bills

The T-bills market traded on a relatively quiet note, with yields slightly higher by c.5bps, as market liquidity was further tightened due to funding for a wholesale FX auction by the CBN. We however witnessed slight buying interests on some short and mid tenured maturities.

We expect yields to remain relatively stable at current levels, as market players speculate on the possibility for a non-OMO issuance this week, given the relatively minute amount of OMO T-bills (N33bn) maturing Thursday and the tight system liquidity levels.

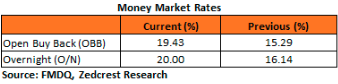

Money Market

Rates in the money market trended higher by c.4pct due to funding pressures from the wholesale FX auction by the CBN. The OBB and OVN rates consequently ended the session at 19.43% and 20.00% respectively.

We expect rates to moderate slightly tomorrow, as banks would be able to access the CBN’s SLF for their funding needs at slightly lower rates.

FX Market

At the Interbank, the Naira/USD rate was unchanged at N307.00/$ (spot) and N355.78/$ (SMIS). The NAFEX closing rate in the I&E window depreciated by 0.10% to N360.68/$, as market turnover fell by 64% to a one month low of $89m. At the parallel market, the cash rate depreciated marginally by 0.03% to N358.40/$, whilst the transfer rate appreciated by 0.14% to N363.50/$.

Eurobonds

The Nigeria sovereigns traded on a relatively flat note with yields marginally lower by c.1bp on the day. Investors were better buyers of the long end and sellers around the belly of the curve.

In the Nigeria Corps, we witnessed slight demand for the DIAMBK 19s and Zenith 22s.

________________________________________________________________________

Contact us:

Dealing Desk: 01-6311667

Email: research@zedcrestcapital.com

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}