Follow Us on Google Discover

Follow Us on Google Discover

Imagine you are China. You sell a lot of stuff to the world. In fact, your whole economy is based on selling things to the world. You have an incentive to make trade as smooth as possible with other countries especially when it comes to making payments.

But you have another dilemma. You are not a wholly open economy. You like to control your currency as much as you can to make it undervalued in a way that benefits your manufacturers. If you let the currency trade freely like the dollar or Pound, the market will probably value it higher than you want which will make your products more expensive.

So, the way you can achieve this is by tightly controlling the amount of your currency that is available around the world. Unlike the US dollar that is widely available around the world to the extent that countries like Ecuador can decide to adopt the dollar as their currency without getting permission from the US, you can’t do that with the Chinese Yuan.

These 2 issues — trading with the world and tightly controlling the circulation of your currency — are in tension with each other. So how to solve it?

A Simple Story of Swaps

Also Read

Or if you prefer the ‘technical’ name — Bilateral Currency Swap Agreements. Depending on who initiates the swap, a simplified version will work something like this.

Nigeria wants to make life easier for its traders who buy a lot of stuff from China. As Nigeria doesn’t sell much to China, it is not easy for the CBN to build up Chinese Yuan reserves. This means that for any trader who wants to buy stuff from China, they have to get prices in dollars. This adds costs and risks given that the person in China giving the quote has to convert Yuan to dollars before sending to Nigeria, bearing in mind the risk of currency moves affecting his bottom line. The Nigerian guy then has to buy dollars to make the payment to him. From the point of view of the CBN, this is extra dollar demand that can be avoided.

So CBN approaches the People’s Bank of China (PBOC) and asks to set up a swap. Xe.com tells me that 1 Chinese Yuan is currently worth about N30. So for the sake of simplicity, let’s say CBN offers to swap N30bn for Y1bn. Both of them agree an exchange rate on the day of the swap (N30 to Y1) and they make the transfer.

Now that CBN has some Yuan, it can then sell it to Nigerian banks in the same way it sells them dollars. The Nigerian trader can then tell his Chinese trading partner to give him a quote in Yuan instead of dollars. Once he has the Yuan quote, the trader can then go to a Nigerian bank and make a request for Yuan in the same way he used to make requests for dollars. Instead of the headache of dealing with 3 currencies, the dollar element is now removed and we have a normal 2-way quote.

This takes off some dollar demand pressure as people who want to buy stuff from China can face their Yuan squarely while the dollar people face their dollars. At least we get to know who is who. All of this is, of course, conditional on the amount of Yuan being swapped.

But what are the Chinese guys going to do with their N30bn? Same thing — they can now pay in naira for anything they buy from their Nigerian trading partners.

Chinese Swaps

For a number of years now, the Chinese have been entering into these swap agreements with various countries on a country by country basis. The swaps typically last for 3 years after which they are renewed or increased. As an example, in 2012, the UK signed a swap agreement for Y200bn with China. Last year, it was extended and increased to Y350bn.

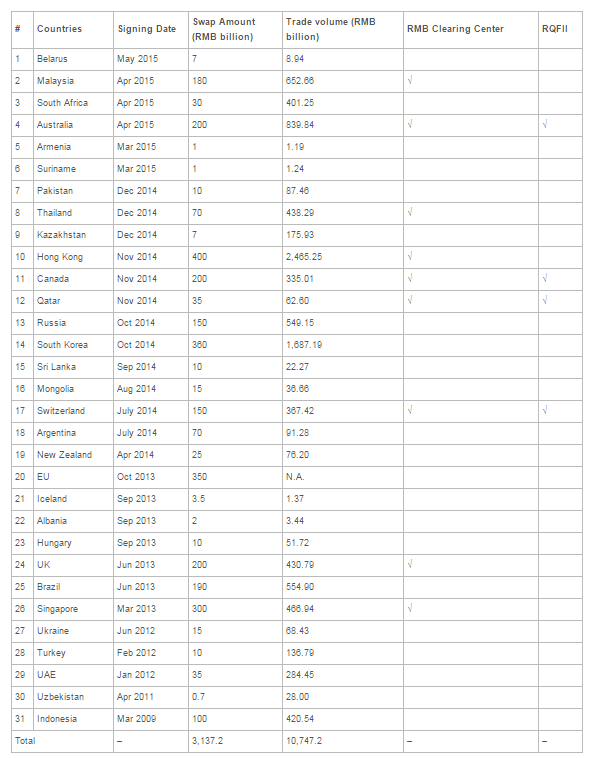

The map below shows the countries that had swaps with China as at 2015, per the PBOC

And here’s a table with the agreements and amounts swapped.

As you can see, Nigeria is coming very late to the party. Perhaps, this might open the gates in Sub-Saharan Africa. It’s also clear they are done on a country by country basis depending on the amount of trade that goes on between them (although the exact correlation is not so easy to work out).

You’re probably asking — if the agreements are for 3 years, what happens at the end? In theory, both countries simply exchange currencies at the same exchange rate they used at the beginning of the swap. Returning to the example above — Nigeria will return the Y1bn to the PBOC and take back its N30bn from them. If this sounds too good to be true, it is. The person who initiated the swap will pay interest on the money it received at an agreed interest rate.

So What Did Nigeria Swap?

Given the above, inquiring minds probably want to know how much Nigeria swapped with China and when does the agreement begin? Well, this is Nigeria and nothing is ever straightforward as it should be.

First of all, it appears that the swap Nigeria entered into was with the Industrial and Commercial Bank of China (ICBC) — the world’s largest bank by assets. That is, the CBN is not dealing with the PBOC but with a ‘private’ Chinese bank (ICBC is owned by the Chinese government).

Second, I have trawled the internet and cannot find the amount that was or is being swapped. As you can see from above, there has to be an amount swapped for it to make any sense. I have searched Chinese news outlets and even ICBC’s news page and cannot find anything on the swap let alone the amount. The news appears to have originated from Nigerian officials who briefed the media. In contrast, Dangote did get a $2bn expansion loan from ICBC and this was announced.

When They Come Back Home

So that’s that about that. Perhaps when they come back home from China, we will get more details from them. But based on this, we know what questions to ask (I’m talking to you Nigerian journalists).

Why was the swap signed with ICBC and not PBOC? How much is being swapped and for how long? And (bonus question), what is the interest rate to be paid? (We can assume the CBN initiated the swap and will be the one to pay interest on the Yuan it receives). How will the Yuan market be priced? Will it be another ‘official’ and parallel rate mess like we currently have with the dollar? This is a trick question because, if it is market priced, we shall have plenty of fun with the contradictions in pricing the dollar ‘officially’ and the Yuan by the market.

But that’s enough speculation for one post.

This article was originally posted in Feyi’s Medium Page and was obtained with permission.

I’ll be the first to admit ignorance on the swap but this article not only cleared up issues, it is making me await the responses to the questions you raised from the Nigerian authorities.

I came here to read the economic benefits of the currency swap, although this is explanatory, but my hopes were not met. *Skipping to the next google search item

I can now clearly see why the Chinese cleverly dominated the world economy. And judging from the current waive of world commerce as is engaging presently, the Chinese will inevitably dominate the world commerce and prosperity. The explanation given above has explained better why the Chinese are speeding up their domination of the world economy. The system that the Chinese approach the world economy appears to be different from the Western approach. Swapping of trade and currency approach undoubtedly will no doubt help the developing world to develop their resources more so on import export trades. Million of dollars are saved by countries that rely on Chinese approach. Direct swapping of trade and currency with the Chinese will eliminate conversion rate from the deal; meaning that a direct dealing with an importer of Chinese product will become cheaper than going through the dollar exchange. This is a very laudable opportunity for Nigeria to patronize the yuan than the dollar. The Chinese are very cleaver and over the years, they have been studying the world economy and having realized the huge advantage of gains that are attributable to their economy quickly and cleverly encourage swapping of their commodities and currency to the entire world! A list of participating countries utilizing the swap system with the Chinese explain why the system is very successful and help all participating countries. My advice is that Nigeria should move quickly by adopting the system and damn the consequences from their current trade partners. Fortunately, Nigeria has a huge population and manpower to address the consequence of trade in balance with the Chinese. Nigeria has the crude oil and minerals to export to the Chinese while we patronize their finished industrial and manufacturing goods. Expectedly, these activities in trade would surely enhance the position of Nigeria’s foreign reserve. After all, Nigeria has been independent from the British for over fifty years, and as a free nation, we are duty bound to trade freely with any economy in the world that will favour the social and economic welfare of our teeming population. Conclusively, this is the best time for Nigeria to take advantage of the usual opportunity. An opportunity once lost can never be regained!

Riveting analysis.i am hooked.

Thanks a lot for this article. It has further broadened my knowledge on this swap thing, But our journalists won’t ask the right questions.

Some Nigerians are jubilating over a $2b loan from China and the so nocknamed the Yuan trading deal.

China wants to lend us 2 billion dollars, but they want to give us in Yuan and not the dollar itself.

They are not handing us cash, but service exchange; meaning if we want to buy iron rods, we buy it from a Chinese company and they pay the company on our behalf. If we want to construct a railway, they will construct it for us and deduct the money out of the loan. In the end, we are bound to award contracts to them, cutting out competition from others and fairplay to others (non Chinese companies can’t bid or compete to reduce the costs). They get to value the contract and determine the price, meaning they can sell something worth 200 Naira for N2000 and we don’t have a choice because it is on credit.

The worst of it is that China wants us to pay back in dollars, that is not all, we are moving our foreign reserve to fake currency (Yuan) a currency that is manipulated openly by the Chinese government. Did anyone ask Lamido Sanusi what happened to some of our reserves he moved to Yuan few years ago? They sold us Yuan at 4 to a dollar, only to devalue their currency few weeks later to 9 Yuan per $.

Many Nigerians don’t know that even Chinese companies don’t want yuan, nobody wants it, Chinese foreign reserve is in dollars, China is the largest holder of US bonds, they want dollars by all means.

Also, China have more lobbyists in Washington DC than any other nations on earth, begging American politicians to always make policy decisions in their favour, how can such country save us from USD? Has anyone asked why China hasn’t built any refinery in Nigeria?? They have the money, they want the profit, but never did it.

If China does anything against Washington’s interest in Nigeria, USA that has too much political power over China will just tell them not to do it. China will continue to inflate the contract price, refuse to complete the project and deceive us further.

I don’t blame Chinese leaders for trying to scam us, I blame our leaders for not being smart enough. What do you expect when you have political hacks negotiating on behalf of Nigeria against smart professionals from China? I was thinking Nigeria political leaders will do research about Chinese lobbyists in Washington and understand the interest they are protecting before believing in this Chinese version of Trojan horse called the Yuan Trading deal.

We are the only ones that can help ourselves, let’s implement true federalism system and free market. Development is a culture and not a product, we can’t buy it no matter how much money we have or borrow.

You must be living in a PARALLEL universe if you think that Nigeria’s intention of being a clearing house for the Yuan in Africa means the naira will now hold steady.

If you like, tie your currency with Thailand Baht or Ghanaian Cedi, the value of your currency will always have the value it deserves.

Hong Kong for instance is an administrative region of China, but guess what, its currency is firmly tied to the US dollar!

The Yuan is not automatically going to be operating independent of the dollar to boost the naira in any way.

The only thing that has happened here is that the Yuan becomes an accepted currency of exchange to facilitate direct business with Chinese people. This will not in anyway strengthen the naira but the gains will be in the avoidance of double exchange from dollar to Yuan.

The Yuan will swing with the wind depending on what happens to the world’s controlling currency, the dollar.

The naira will continue its natural descent as we produce and export very little and even trade with China becomes very expensive as the world’s comparative exchange rate will not wait for the Naira/Yuan pretend marriage.

The value of the naira will continue to be subject to the international exchange rate, which is controlled by and inextricably linked to (you guessed it?) the DOLLAR!

The silly idea that this arrangement could crash the dollar is only palatable to people living in a cocoon, in a cuckoo land (Nigeria), with a totally warped sense of reality.

The real winners here are the Chinese who have found another place to ship their milling population to recolonise on the cheap.

Nigeria has taken the path of double parallel which will be unsustainable in the medium term as a consumer nation.

The naira will continue to fall unless you can sell more oil or start exporting something the rest of the world would pay you for.

My projection for the naira is 500 to $1 by year end if the oil price does not improve drastically and we sell oil, the only thing we ‘produce’.

My small contribution, The dollar today is 310 Naira and trade between Nigeria and China is 13billion USD per year. To buy this in the black market you are looking at 4 trillion Naira. 13billon USD in Yuan is 84billion Yuan. In Naira this comes to 2.5trillion Naira. I really don’t gerrit Professor economist.

This policy saves Nigeria about 1.5 trillion Naira. And its not a forever deal Prof; in essence if tomorrow the dollar becomes cheaper in Nigeria we can simply go back to buying the dollar and changing it to Yuan like we used to do.

is the transaction even up to a trillion

This is good for our economy

The deal is definitely in favour of the higher exporter among the two country. For Nigerian Naira to avoid Dollar influence as the country goes for the Yuan swap, effort should be intensified to export more and more products and services from the country.

Dandago