Follow Us on Google Discover

Follow Us on Google Discover

Nigeria entered 2026 with momentum on its side: a recovering naira, declining inflation, and an economy that had grown faster in 2025 than the year before.

By the time June closed, some of those tailwinds had held, while others had not.

Inflation reversed direction, government borrowed more aggressively than ever, growth continued but left most Nigerians behind, and the naira, against all expectations, held steady.

These four variables, although not all the stories, explain how all of that happened at the same time, and what it means for the rest of the year.

Other News

Gross Domestic Product (GDP)

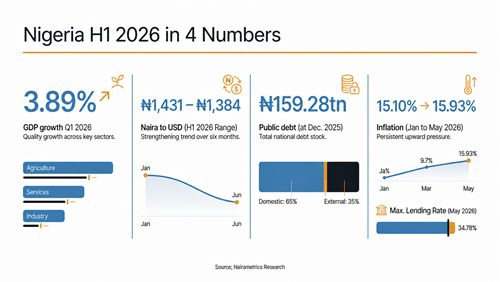

One of the defining variables of Nigeria’s first half was its economic growth rate. In the first quarter of 2026, GDP expanded by 3.89%, according to data from the National Bureau of Statistics, an improvement from the 3.13% recorded in the same quarter a year earlier and marginally above the 3.87% growth posted for full-year 2025.

On paper, the economy is growing. In reality, it is still not growing fast enough to transform living standards.

Economists generally agree that for a country with Nigeria’s rapidly expanding population and labour force, GDP growth needs to consistently exceed 5%—and preferably remain there over several years—to generate enough jobs, reduce poverty meaningfully and absorb new entrants into the workforce. Achieving that level of growth requires sustained investment in large-scale infrastructure, manufacturing, agriculture, energy, logistics and other sectors capable of creating employment at scale.

For now, the benefits of Nigeria’s economic reforms remain unevenly distributed. Consumers continue to shoulder the burden through higher living costs, while the government enjoys stronger tax collections, investors benefit from elevated yields on government securities, and exporters gain from a more competitive exchange rate. The broader economy has yet to translate these reforms into widespread improvements in incomes and employment.

A closer look at the GDP numbers explains why.

Services once again carried the economy in the first quarter. Telecommunications expanded by 12.24%, financial services grew by 8.54%, while cement manufacturing rose 11.53%.

These are important sectors that generate significant revenues, profits and market capitalisation, but they do not employ enough Nigerians to fundamentally alter the country’s employment profile.

Meanwhile, agriculture—the country’s largest employer—grew by just 3.15%. Manufacturing expanded by only 3.29%, while oil and gas, the sector that still finances much of government spending and foreign exchange earnings, recorded growth of just 2.57%.

The imbalance becomes even more striking when viewed through the structure of Nigeria’s economy. Crop production, trade, real estate, telecommunications, construction and livestock together account for roughly 65% of nominal GDP. Yet, apart from telecommunications, most of these sectors continue to record low single-digit growth rates. As long as the economy’s largest components continue to expand at this pace, Nigeria is likely to remain trapped in a cycle of respectable but ultimately subpar economic growth.

This also explains why the International Monetary Fund became more cautious. In its April 2026 World Economic Outlook, the Fund revised Nigeria’s 2026 growth forecast down by 0.3 percentage points to 4.1%. With first-quarter growth coming in at 3.89%, the economy will need to accelerate meaningfully in the second half of the year to achieve even that target.

More importantly, the quality of that growth matters as much as the headline number. Faster expansion driven solely by finance and telecommunications will continue to support corporate earnings, but it will do little to change employment outcomes or household incomes. Sustained improvements in living standards will require stronger growth in agriculture, manufacturing, construction, trade and energy—the sectors where most Nigerians work and where government policy can have the greatest multiplier effect.

If these sectors fail to accelerate, Nigeria risks ending another year with GDP growth that looks respectable in official statistics but remains largely invisible in the daily lives of ordinary Nigerians.

The exchange rate: From N1,431 to N1,384

Another factor that shaped H1 is the stability of the exchange rate, unlike what we had in 2023 and 2024, which affected corporates.

When the NFEM window opened in January 2026, the naira was exchanging at N1,431 to the dollar. By June, it had moved to N1,384; an appreciation of N47 across 118 trading days, with an average of N1,375.93.

In 2024, the naira was more volatile, creating enough uncertainty to make business planning almost impossible

However, by H1 2026, the naira was not just stronger; it was steady. For businesses pricing imports, manufacturers planning production, and households budgeting for school fees, the steadiness mattered as much as the direction.

Three things drove that stability: diaspora remittance inflows, CBN’s managed float, and Dangote Refinery’s growing petrol output that began cutting into Nigeria’s dependence on refined product import, one of the biggest structural sources of dollar demand.

The rate movement shaped more than the foreign exchange market. A calmer naira meant companies recorded fewer foreign exchange losses, which fed directly into profitability. The parallel market gap narrowed, though it did not close, but the direction was right.

For H2, the naira trajectory depends on whether the same variables that drove H1 hold. Remittance flows are seasonal. CBN intervention capacity depends on reserves, and Dangote’s import substitution effect depends on both refinery output and global product prices.

If those conditions persist, the band holds. If anyone weakens, H2 will quickly test how much of H1’s naira stability was structural and how much was simply circumstantial.

Total public debt and government borrowing

Federal Government borrowing is one of the critical numbers that shaped H1 2026 and will continue to shape H2.

The Debt Management Office puts Nigeria’s total debt stock at N159.28 trillion as at December 2025; external obligations of N74.43 trillion and domestic debt of N84.85 trillion.

But by May 2026, credit to the Federal Government had jumped to N40.38 trillion, up 75.6% from N22.99 trillion in May 2025, rising another N779.7 billion in a single month. Nigeria was not just carrying a heavy debt load into 2026. It was actively adding to it.

The consequences ran through everything in H1. Banks found government paper irresistible — risk-free, high-yielding, and in endless supply. Credit to the private sector grew only modestly to N81.04 trillion even as government borrowing surged.

Manufacturers, farmers, and small businesses were crowded out; many resorting to commercial paper at even higher yields.

The result was a financial system that looked healthy on the surface; banks were profitable, yields were attractive, while the real economy remained starved of the affordable credit it needed to grow.

Inflation and the cost of money

Another variable is inflation, which entered 2026 at 15.10% and edged to 15.93% by May, moving in the wrong direction.

More telling was food inflation, which nearly doubled from 8.89% in January to 16.96% by May. For households where food consumes the largest share of monthly spending.

The CBN cut its benchmark rate once from 27.00% in January to 26.50% in February, then held. That single 50 basis point cut was the entirety of H1’s easing.

The cost of that caution showed up immediately. Maximum lending rates reached 35.17%, making productive borrowing almost impossible for most businesses.

Savings deposit rates sat at just 7.24% against inflation of 15.93%, meaning Nigerians keeping money in the bank were losing purchasing power every month.

For the economy, the combined effect was a squeeze from both ends. Businesses could not afford to borrow and expand; households could not afford to spend, consumer demand stayed weak and private investment remained suppressed, directly limiting the GDP acceleration Nigeria needs in H2.

The outlook for the second half hinges on whether food inflation reverses during the harvest season and whether the CBN feels confident enough to cut again.

If both happen, borrowing costs ease and consumer pressure softens. If food prices stay elevated, the MPC stays cautious, and the squeeze continues into 2027.

Uncertain Second Half

Taken together, these variables describe an economy where growth is real but narrow. The naira is stable but fragile. Public debt remains large and continues to climb. Inflation has moderated at the headline level but is still accelerating where it matters most to households through food prices and the high cost of borrowing.

The second half of 2026 will also coincide with the early stages of Nigeria’s 2027 election cycle, introducing another layer of uncertainty. Historically, election seasons have tended to shift the attention of policymakers away from economic reforms toward political calculations and campaign activities, often slowing the pace of policy implementation and delaying difficult fiscal decisions.

Fiscal execution is another area to watch closely. Budget implementation has been weak over the past three years, limiting the government’s ability to translate ambitious spending plans into tangible economic activity. While official implementation data for the 2026 budget is yet to be published, the recent extension of the 2025 budget suggests execution remains behind schedule, raising questions about the pace at which capital projects and economic stimulus will reach the real economy.

The second half of 2026, therefore, will not be defined by a single event. It will be shaped by whether oil, agriculture and manufacturing can accelerate enough to lift GDP growth to levels that ordinary Nigerians can feel; whether the pillars supporting the naira remain intact despite external pressures; whether government borrowing slows sufficiently to free up credit for the private sector; and whether policymakers can maintain economic reform momentum as political activity gathers pace ahead of the 2027 elections.