Nigeria will be the third most populous country on earth by 2050.

Its population, currently about 235 million, will reach roughly 401 million at mid-century and approach 791 million by 2100, a figure larger than Europe and North America combined.

These projections come from the United Nations Population Division’s median model and have been consistent across successive revisions.

What is genuinely contested, and what actually matters, is whether that population represents an economic opportunity or a humanitarian emergency.

The answer is not determined by demography. It is determined by what Nigeria chooses to do in the next ten to fifteen years.

The demographic dividend, formalised by Harvard economists David Bloom and colleagues drawing on the East Asian growth experience, refers to the period during which a country’s working-age population is large relative to its dependent population: more producers than dependents, rising household savings, and, if institutional conditions allow, a virtuous cycle of investment and growth.

Nigeria currently sits at the leading edge of that window. Approximately 63 per cent of the population is under 25, and four million young people turn 15 every year. The window, on credible projections, stays open until roughly 2050 to 2060.

That is not unlimited time, and the actions that determine whether the window delivers its dividend, such as education investment, fertility reduction, job creation, and security, require fifteen to twenty years to take effect. The effective policy window is already narrower than the demographic one.

The dividend is not automatic. Three conditions must be met simultaneously: a workforce that is educated and skilled enough to be productively employed; an economy that generates enough jobs to absorb it; and a governance environment that channels the savings a young population generates into investment rather than into corruption and capital flight.

Countries that have met these conditions, such as South Korea, Taiwan, and Bangladesh, produced growth episodes of extraordinary speed. Countries that have not converted their demographic windows have consistently met a different outcome: mass youth unemployment, social unrest, and political instability. Nigeria, on current trends, is meeting the second set of conditions more reliably than the first.

The education deficit is the most visible structural barrier. Nigeria has the largest number of out-of-school children of any country in the world, with approximately 20 million primary and secondary school-age children not in class.

The gross enrollment ratio of 84 per cent conceals dropout rates and quality failures severe enough that the World Bank classifies Nigeria as having a “learning poverty” crisis in which a majority of Nigerian ten-year-olds cannot read a simple sentence with comprehension. Secondary enrollment stands at roughly 45 to 50 per cent of eligible adolescents.

Tertiary enrollment is approximately 10 to 12 per cent, one of the lowest ratios of any large economy. The World Bank’s Human Capital Index places Nigeria at 0.361, meaning a child born today will realise only 36 per cent of their productive potential given current education and health conditions. South Korea scores 0.84. Even poorer countries such as Ethiopia, at 0.38, and Ghana, at 0.44, exceed Nigeria.

The fertility rate is the variable that determines everything else. Nigeria’s total fertility rate stands at 5.1, one of the highest for any large country. The dividend window opens properly only when the dependency ratio falls, and the dependency ratio does not fall without a fertility transition, and the fertility transition does not happen without girls in secondary school.

The relationship is causal: women with secondary education have, on average 1.5 to 2.0 fewer children over their lifetimes than women without it. The fertility rate is not uniform across Nigeria. In Lagos, urban professional women average two to three children.

In Kano and Zamfara, the average is six to seven, in communities where girls’ secondary enrollment is among the lowest in the world and child marriage rates are among the highest. Nigeria has two demographic trajectories operating simultaneously within the same country, and the more severe is concentrated in Northern Nigeria, a region where insecurity and educational exclusion are also most acute.

The employment arithmetic is blunt. Four million Nigerians enter working age each year, and Nigeria’s formal sector absorbs an estimated 500,000 to 800,000 new workers annually. The remainder flows into the informal economy of petty trade, subsistence farming, motorcycle taxis, etc, where no skills accumulate, no taxes are paid, and no productivity growth occurs.

The mechanism linking growth to jobs is captured in the employment elasticity of output: standard estimates from the World Bank and Nigeria’s National Bureau of Statistics place Nigeria’s employment elasticity at between 0.5 and 0.75, meaning that every one percentage point of GDP growth generates between half and three-quarters of a percentage point of employment growth.

Applied to a labour force of Nigeria’s scale and given the size of the annual entry cohort, this elasticity implies that absorbing four million new workers per year into the formal economy requires sustained GDP growth of at least 7.5 per cent annually, representing the midpoint of the seven to eight per cent range that the full modelling supports. Nigeria is currently growing at approximately 3.9 per cent.

The gap of roughly 3.5 percentage points of annual GDP growth, compounded across a decade, is not a marginal shortfall but the difference between a demographic dividend and a demographic crisis. It cannot be closed by monetary policy or exchange rate reform alone. It requires structural transformation of the manufacturing base, agricultural value addition, and a digital economy that extends well beyond Lagos’s top income tier.

The security dimension compounds every other challenge. Boko Haram’s insurgency in the North-East has destroyed thousands of schools since 2009 and displaced more than two million people; approximately 600,000 school-age children in that region alone are not in class because of conflict.

Each year they remain out of school is a year subtracted from their human capital development and from the fertility reduction that the dividend requires. The bandits of the North-West have rendered vast areas of Zamfara, Katsina, and Kaduna states ungovernable for farmers, traders, and teachers alike. In the South-East, the sit-at-home order enforced since mid-2021 has removed one working day from the regional economy every week, at a cumulative cost economists estimate in tens of billions of naira annually.

The combined effect is to compress the geographic space within which the dividend can be captured, concentrating it in the South (with less of the problem) and in urban centres while the North, which has both the highest fertility rates and the youngest populations remains precisely where the dividend is most needed and least accessible.

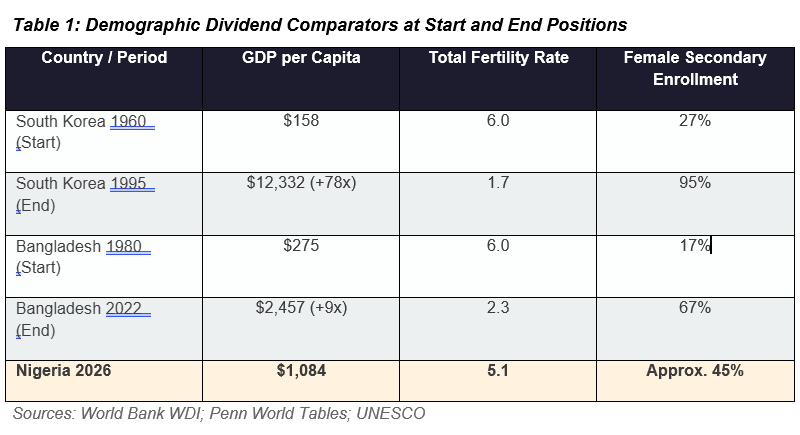

Table 1: Demographic Dividend Comparators at Start and End Positions

Table 1 depicts the comparison of demographic dividend across relevant countries, with Nigeria 2026 column showing its current position at the start of its dividend window. The historical record offers both a template and a warning. South Korea in 1960 had no meaningful natural resources and a GDP per capita of $158. It invested in universal secondary education and labour-intensive manufacturing, which saw GDP per capita rise 78-fold in 35 years. Bangladesh is the more instructive comparator.

In 1980, it had a total fertility rate of 6.0, female secondary enrollment of 17 per cent, and a GDP per capita of $275, which is lower than Nigeria’s at that time, with no oil wealth, weaker geography, and a smaller domestic market. It invested in girls’ secondary education and light manufacturing employment.

By 2022, its TFR had fallen to 2.3, female secondary enrollment had reached 67 per cent, and GDP per capita had risen ninefold. Nigeria enters 2026 with better natural resources, better geography, and a larger market than Bangladesh ever possessed. It has also, to this point, made different choices.

The Tinubu macroeconomic reforms, consisting of subsidy removal, currency unification, and fiscal consolidation, are necessary but not sufficient. Macroeconomic stabilisation creates the fiscal platform; it does not build the schools, train the teachers, or generate the four million formal sector jobs the demographic clock demands each year. The building must now be constructed on the platform that stabilisation provides.

The policy agenda follows directly from the evidence: universal girls’ secondary education as an urgent national priority; a sustained national fertility strategy, delivered through women’s healthcare and school access concentrated in the North; manufacturing and agro-processing industrial policy scaled to absorb millions of workers annually; security restoration that reopens the geographic space where the dividend is most needed and least accessible; and a governance framework that channels investment into these priorities rather than into the informal arrangements that have historically consumed them.

The window is open. The clock is running. A girl who enters secondary school in 2030 enters the labour market in 2036 and makes her fertility decisions in the 2040s. The policy choices that shape her educational trajectory must be made now, at a scale and pace that Nigerian education budgeting has not yet reached.

Bangladesh made those choices in 1980 with fewer resources, worse starting conditions, and no oil revenue to draw on. The question is not whether Nigeria can do what Bangladesh did. The question is whether the political will exists to try.

Akinola Morakinyo (Ph. D) writes on MINT economies from the Department of Economics, Finance & Quantitative Analysis, University of Kennesaw, GA, USA

For full writeup, go to https://docs.google.com/document/d/1S_Wm1UYWc7KBp832G808f_iS3hpilo9T/edit?usp=sharing&ouid=115902141979210189388&rtpof=true&sd=true

{kind=link}