UPDC’s share price has surged a whopping 94.97% YTD, making it the third-best performing stock on the Nigerian Exchange as of February 21, 2025.

That’s an impressive rise, but the real question is: Does this meteoric climb truly reflect the company’s fundamentals, or is it just another speculative fever dream in the making?

Investors have been willing to assign a generous 44x PE ratio to UPDC’s earnings, a hefty premium that raises eyebrows.

For context, 44 times earnings means investors are betting heavily on the company’s future growth.

But after three out of the last five years of losses, can UPDC justify such a lofty price tag based on this year’s N0.07 per share earnings?

Also, with an EPS growth of 600% from N0.01 per share last year, is this sustainable, or should investors brace for a reality check?

Revenue growth: More than just numbers?

UPDC seems to be riding a strong wave of growth, with revenue soaring by 123% to N11.935 billion.

Most of that growth is tied to its property development business, which contributed 88% of total sales.

The hospitality segment also crossed the N1 billion mark, signaling more expansion. Sounds like a success story, right?

While gross profit margins have improved to 35.89%, a far cry from the -40.70% seen in 2019, the net profit margin remains relatively modest at just 11.31%. That’s a lot of revenue, but it’s still a narrow window for profit.

What’s eating into UPDC’s margins? High costs are still a thorn in its side, despite improvements in operational efficiency.

So, what about that 44x PE ratio?

A 44x PE ratio is eye-popping, but when you add in UPDC’s 600% EPS growth, things start to look a little less absurd.

Let’s do the math on the PEG (Price/Earnings to Growth) ratio:

- EPS growth: A 600% jump from N0.01 to N0.07.

- PEG ratio = PE ratio / EPS growth rate = 44 / 600 = 0.073.

A PEG ratio of 0.073 suggests the stock may be undervalued relative to its earnings growth. This implies that despite the high PE multiple, UPDC’s valuation might be reasonable if earnings growth is sustainable.

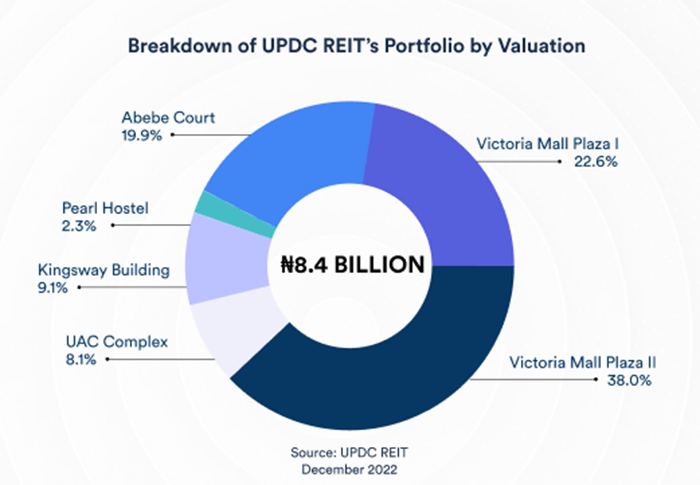

The Gruppo Limited_Brompton City factor

UPDC’s N5.2 billion in revenue from Gruppo Limited_Brompton City certainly gave the numbers a boost.

- But let’s not forget: the Brompton City project, a massive 30-hectare development on Ogombo Road in Lekki Scheme II, is still in its early stages. Sure, they’re optimistic, but is it all just a long-term gamble?

- On top of that, UPDC made another N4 billion in property stock sales, up from N1.9 billion in 2023. That’s a solid increase, but as mentioned earlier, the status of Phase 1 sales remains uncertain.

It’s all well and good to make projections, but until those developments start turning into cash, we can’t fully rely on them to fuel the stock price.

The macroeconomic elephant in the room

While UPDC has managed to keep its debt levels relatively low; N3.1 billion in borrowings and a negative net debt (-N8.36 billion); several macroeconomic hurdles remain.

These could hamper UPDC’s ability to sustain its recent run:

- High borrowing costs: The MPR is still at 27.50%, making financing expensive.

- Inflation pressures: Inflation has eased to 24.48%, but consumer purchasing power remains weak.

- Liquidity concerns: UPDC’s free float is a paltry 4.89%, making its stock prone to volatility.

Can the stock rally be sustained?

UPDC’s high PE ratio, despite its strong growth in EPS, still raises serious questions about the stock’s future trajectory.

- While the PEG ratio suggests that the current multiple isn’t as outrageous as it may first appear, the real estate market is a fickle beast. If UPDC can’t deliver on its promises, particularly around Brompton City, it may struggle to keep up the momentum.

But here’s the kicker: UPDC’s stock is priced as though the growth is set to continue at breakneck speed.

If the company’s developments don’t live up to expectations, or if macro pressures like inflation and high financing costs take their toll, investors could face a rude awakening.

Buy, Hold, or Sell?

- For those in the Buy camp, the real estate boom and expanding property portfolio suggest strong growth for UPDC in the long run.

- For those on the Sell side, the low free float, ongoing cost pressures, and potential real estate slumps are cause for concern.

- As for the Hold crowd, it’s all about whether you believe the 44x PE ratio can hold its value in the face of macroeconomic uncertainty.

In short, investors should proceed with caution, as UPDC’s stock remains a bet on the future rather than a reflection of the present.

{kind=link}