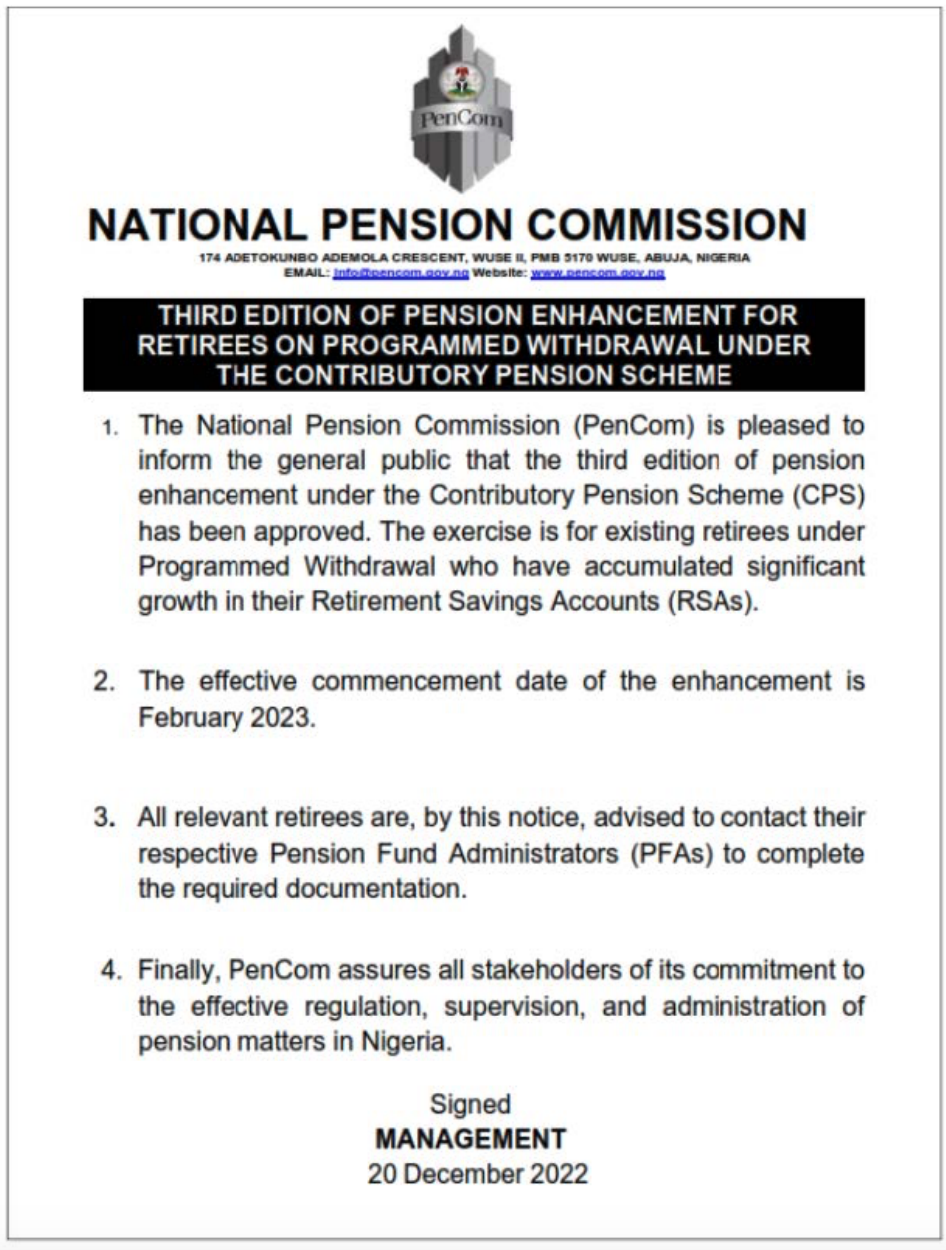

On 20/12/2022 PenCom released a statement that the “third edition of the pension enhancement has been approved” which is for “existing retirees…who have accumulated significant growth in their Retirement Savings Account (RSAs)”.

An enhancement is essentially an increase in the amount paid of pensions paid to pensioners monthly. The amount is paid out of their retirement savings account.

A pension enhancement should be good news to retirees (pensioners on programmed withdrawals), but it may be turning out not to be.

According to the information received, the calculation is based on the following:

- Sometime late 2021 PenCom requested balances on the accounts of all retirees as at

October 2021 o In October 2022, PenCom instructed PFA’s to calculate, using a PenCom-supplied Excel template the amount of pension enhancement for retirees

- In December 2022 PenCom released a statement about their third edition of the pension enhancement (see attached)

According to PenCom’s Q3 report, there are 315,112 retirees on programmed withdrawal amounting to N13.88bn paid out monthly.

A pensioners experience

Nairametrics spoke to a pensioner to get an understanding of the impact of the”enhancement” on their financial well-being.

The pensioner, who preferred to remain anonymous, lamented that while they acknowledge the increase in pension payout, it lags the inflation rate and is not enough considering the level of returns recorded over the years.

- “I began drawing a pension from my RSA in late 2016. Since December 2016, even after the payment of a monthly pension to me, my RSA has risen by 22.75% as of 31 December 2022. My PFA over those 6 calendar years to 31 December 2021, has returned an average return of 14.04%”

- “Since 2016, the average annual withdrawal rate, i.e., pension payments to me, has been 8.05%. In other words, despite me being in retirement and drawing a pension, my RSA balance is growing at a faster rate than I am being allowed to draw”

- “Last week I got a text message from my PFA that, based on the 2022 pension enhancement program, I am entitled to a pension enhancement, and I should call to find out how much. I did call and was told it amounted to an 8.67% rise (still subject to PenCom approval).”

Enhancement not good enough

While the decision to introduce the enhancement at a time of economic difficulty is appreciated, the macroeconomic indicators suggest it is not enough.

- For example, Interest rates – 17.50%, December headline inflation – 21.34% (food inflation is 23.75%), 20-year bond yield – is 14.80% (Jan 2042) o 10-year bond yield – is 14.75 % (Apr 2032) and 5-year bond yield – 13.40% (Feb 2028).

- These indicators suggest the pensioner is still left worse off.

Further checks by Nairametrics suggest the model for determining the enhancement rates is not transparent making it difficult for a pensioner to decipher how their enhancement was derived.

An inquiry with a PFA asking how the enhancement was determined suggests the balance used was October 2021, while an interest rate of 8% was used far lower than the long-term interest rate.

- The response from the PFA was “Kindly note that the calculation on the use of your RSA balance as of October 2021 was based on PenCom’s directive. The interest rate used in the calculation was also obtained from the PenCom.”

A spreadsheet seen by Nairametrics also shows assumptions that were not quite explainable were used in determining the enhancement leaving pensioners confused and with more questions than answers.

Questions to ponder

- Are retirees short-changed?

- Retiree RSA balances are growing but pay-outs are falling. Is this just about accumulating AUM and operators’ earning fees?

- Why are there fees still included in the calculation when the overall fund has paid fees before the NAV per unit which is used to multiply the number of units to get the value of an RSA balance? NB: the custodian fee is missing!

- Why the mystery behind the spreadsheet? Where’s the openness and transparency in the system?

- Why the diktat from PenCom? Why is approval required again from PenCom?

- Why is the enhancement only every 3 years?

- Where is competition if ALL the PFAs are using the same template that spits out the same result?

This article has been updated to reflect new information

{kind=link}

It is really unfortunate that PENCOM may decent so low as yo be shortchanging ret8rees for worldly gain. Going through the write-up, the writer is not a novice in the area of finance and PENCOM should know that there many like him out there. No competition in the operations of pension administrators going by the activities of PENCOM. Thus is Nigeria anyway where anything goes.

What is the way forward? How can we restore the confidence of Pensioners?

Nothing shocks me again in Nigeria. The truth is that government agencies collude with private organizations to rip off innocent Nigerians. Nigerian Electricity Commission (NERC) colludes with DISCOS; NNPC and its affiliates collude with IPMAN, etc to shortchange Nigerians.

PENCOM is a scam. GOVERNMENT is a scam. NIGERIA is gradually becoming a scam where nothing works and anything goes.

Nobody has been able to explain why money set aside for retirement cannot be withdrawn by the owner while alive but all can be paid to the next-of-kin when he dies.

Corruption everywhere!

Indeed, right now CBN is colluding with banks to shortchange Nigerians. Or how else can one explain the inability of CBN to apply MAXIMUM SANCTION on banks for refusing CBN directives to stop paying out old notes? How on earth can banks be purportedly removing old notes from circulation and at the same time paying it out into circulation?

Its worst on Insurance Annuity because all through your life, you receive the same monthly emoluments from your pension fund remitted to them by Pencom at your retirement. No increase, no enhancement whatever and no provision from Pencom.

The word enhancement is ridiculous: one will think is a fantastic amount: I was made by my pension manager to fill a volume of papers, spent N800 on passport; Transport fare there was N1600 only to be told my enhancement is N900: I retired 5yrs ago on GLl6/9(Conhess 14/9). I was very much unhappy.

Pensioners who have suffered accumulating this sum while at work are still suffering getting it in full from pencom. What a shame!. Which area of life in this country can one say I am happy being a citizen. God dey o

That’s why we keep urging all retirees to opt for annuity which pays the highest rate always.

A woman was offer 67k monthly at a PFA for 8yrs life expectancy & at the same time an annuity worth 100k+ for lifetime. That’s over 33k extra monthly!

Which enhancement will meet up with that within 8yrs when she would have received over 2.8m extra from annuity!

Nothing beats making the right decision after retirement. There is no Program Withdrawal in any other countries of the world!!🤷

Yes, that’s the best you can get, but the option now Annuity plan no matter how you intend to frustrate it, surely it will continue to grow

Choose Leadway Annuity now – reach out to me on my email: joelakams@yahoo.com

Retirement savings withdrawal (RSA) and annuity are the same. Because annuity your fund is not growing at all and do the calculation by your self for the years guarantee is your money spreads., then thereon as they will state on the policy. Am yet to see anybody who is on annuity enjoying same after ten years guarantee. Between devil and deep blue sea. Now this scam enhancement my PFÀ are yet to call me for enhancement and am RSA for over seven years.