Following the Presidential assent to the Finance Bill, the Minister of Finance, Zainab Ahmed, disclosed that the new tax reforms as contained in the Finance Bill would help the Federal Government (FG) achieve its 2020 revenue estimate of N8.16 trillion.

She further noted that although the Finance Law proposes an increase of VAT rate from 5% to 7.5%, a large sum of money (50% and 34%) realised from the taxation would go to states and local governments respectively while the balance of 15% will go to the FG.

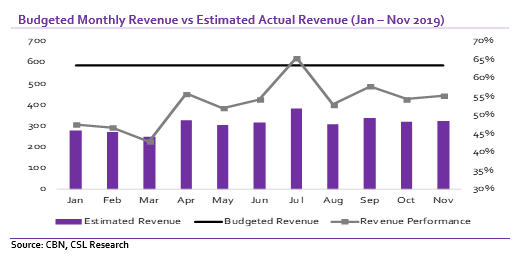

Over the years, the Federal Government has struggled to meet up with its revenue target owing to persistent shortfalls in its two major sources of revenue; oil and non-oil revenues. On one hand, the underperformance in oil revenue has often been attributed to volatilities in oil prices, disruptions to crude oil production caused by militant activities, shut-ins and shut-downs at NNPC terminals, due to pipeline leakages and maintenance activities.

On the other hand, the sub-optimal performance in non-oil revenue has alluded to the decline in revenue from VAT, Education Tax and Federal Government Independent Revenue (funds generated by agencies). Based on data obtained from the CBN’s monthly and quarterly economic report, total revenue came to N3.4 trillion for the first eleven months in 2019 compared with prorated budgeted revenue of N6.4 trillion, translating to a performance of 53%.

Considering the changes made to the nation’s tax laws particularly in Value Added Tax (VAT), Customs and Excise Tariff, Stamp Duties Acts, we ask; How far can the various tax reforms go in supporting government revenues in 2020?

In our opinion, we think the amendments to the tax laws will bear some fruits and improve government revenue, however, we believe revenue will continue to lag budgetary estimates owing to OPEC+ production cuts which limit the nation’s ability to reach the budget assumption of 2.18mbd.

[READ MORE: Now that President Buhari has signed the Finance Bill into law)

________________________________________________________________________

CSL STOCKBROKERS LIMITED CSL Stockbrokers,

Member of the Nigerian Stock Exchange,

First City Plaza, 44 Marina,

PO Box 9117,

Lagos State,

NIGERIA.

{kind=link}