Follow Us on Google Discover

Follow Us on Google Discover

This is the summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills and FGN Bonds.

This report is dated August 1st.

***Oil plunges the most in 4 years as trade war escalates***

Other News

Bonds: The FGN Bond Market remained relatively stable, with demand interests still witnessed on the short end of the curve. Yields consequently remained relatively unchanged on the day.

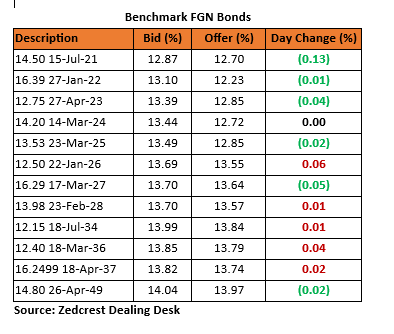

Whilst expecting stable bond yields in the near term, we are wary of the renewed trade tensions between the US and China, which whipsawed oil prices, following the announcement of further tariffs on China by the US President today.

[READ MORE: Investors Renew Demand for Long Tenured FGN Bonds]

Treasury Bills: The T-bills market traded on a slightly bullish note, as the CBN abstained from conducting an OMO auction, despite the inflows from OMO T-bill maturities and relatively ample system liquidity. Demand interests were however subdued, as market players positioned for the Retail FX funding expected tomorrow.

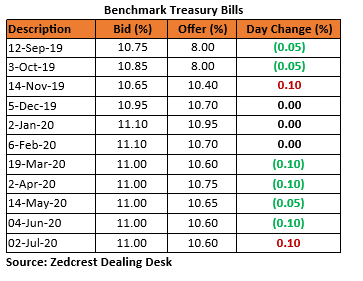

We expect yields to be slightly pressured, mostly on the short end of the curve, as banks fund for the CBN’s bi-weekly retail FX auction tomorrow.

[READ ALSO: FGN Bond Yields Compress Following Robust Auction Demand]

Money Market: Rates in the money market declined by c.1pct as inflows from OMO T-bill maturities further bolstered system liquidity levels. The OBB and OVN rates consequently ended the session at 2.50% and 3.21%, with system liquidity currently estimated at c.N330bn positive.

We expect rates to trend higher tomorrow, as banks fund for the Retail FX auction by the CBN.

FX Market: At the interbank, the Naira/USD rate remained stable at N306.85/$ (spot) and N357.68/$ (SMIS). The NAFEX rate at the I&E window reverted back above the N362.00/$ mark to close at N362.23/$, as market turnover hit its lowest level since January at $64m. At the parallel market, the cash and transfer rates remained stable at N357.50/$ and N362.00/$ respectively.

Eurobonds: The NIGERIA Sovereigns traded on a weaker note, with prices opening about 1pct lower before recouping some gains later in the day. This was due to selloffs by traders following less than expected dovish comments from the US FED following its quarter-point rate cut.

The NIGERIA Corps were also slightly better offered, with more selling interests witnessed in the FIDBAN 22s, ZENITH 22s and ETINL 24s.

[READ FURTHER: FBN 2021 Redemption Boosts Nigerian Eurobond Prices Higher]

Contact us: Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer: Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not a piece of investment advice or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.