Follow Us on Google Discover

Follow Us on Google Discover

Smuggling and Price Cuts Drag Revenue: Dangote Sugar Refinery Plc posted Q1:2019 revenues of NGN38.15bn, which is 7.72% lower than the NGN41.14bn generated in Q1:2018. The decline was fueled by the drop in the price of sugar; average price per 50kg bag of sugar fell from NGN13,054 in Q1:2018 to NGN12,775 in Q12019.'/%3E%3C/svg%3E)

The prevalence of smuggled products in primary markets in the Northern parts of the country also precipitated in NGN1.93bn loss in revenue. The group production and sales volume, however, increased by 34.96% and 3.76% respectively, helping to moderate the impact of the price reduction. The uptick in sales volume in Q1:2019 also reversed a downward trend observed since Q1:2018, reflecting early indications that management efforts at improving the distribution of products are yielding results.

We maintain our previous projection of a 7.00% increase in sales volume. However, considering the pressure on price, we revised our revenue expectation down to NGN154.99bn, representing a 3.08% rise from the revenue in 2018 FY.

Cost Gains Boost Margins: The downtrend witnessed in global raw sugar prices from an average of $14.85 per pound in Q1:2018 to $12.88 per pound in Q1:2019 precipitated an 8.00% drop in the cost to sales ratio to 67.00% in Q1:2019. Hence, the gross margins increased to 33.00% in Q1:2019(vs. 25.00% in Q1:2018).

The management fees, along with selling and marketing expenses, also dropped by NGN241.42mn and NGN178.33mn respectively (vs.NGN420.20mn and NGN213.68mn in Q1:2018), thereby increasing operating margins from 21.74% in Q1:2018 to 28.46% in Q1:2019. In line with the trend witnessed in the gross and operating margins, the net margins increased from 12.85% in Q1:2018 to 18.36% in Q1:2019 despite a higher tax expense of NGN3.70bn (vs. NGN3.11bn in Q1:2018).

The cost gains witnessed in Q1:2019 are expected to remain for the major part of the year. However, raw sugar prices might tick upwards slightly towards the end of the year as the effects of lower sugarcane production and allocation to sugar production begin to pressure prices. Given our revised revenue and cost of sales estimates of NGN113.92bn for 2019 FY, we expect net profit to settle at NGN22.19bn, representing a net margin of 14.32%.

Smuggling Prompts Rise in Receivables: The prevalence of smuggled products in key markets of the company also resulted in the company receivables increasing by 22.33% over the period to NGN9.22bn in Q1:2019 from NGN7.54bn at the end of 2018. The implication of the increased receivables is reflected in the earnings quality of the company as the operating accruals rose to NGN6.19bn from NGN1.78bn in Q1:2018, indicating poorer cash generation from operations during Q1:2019.

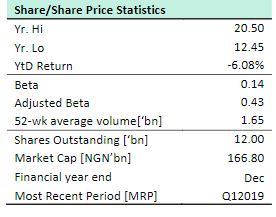

Valuation and Rating: Following due considerations of market and industry risks facing the company, we estimate a target price of NGN13.41 based on a target PE of 7.25x and expected EPS of NGN1.85. The target price has a downside of 2.85% from the share price on May 13, 2019; hence we place a HOLD rating on the stock.