Daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

- Inflows from Paris Club Refunds Bolster System Liquidity amid SMIS Outflows

- Decision on minimum wage will be taken on Monday – Ngige

KEY INDICATORS

Bonds

The bond market was just a touch bearish in today’s session, with yields marginally higher by c.1bp on the day, following slight sell on the 24s and 27s. Yields were however higher by c.12bps w/w, mostly due to the bearish sentiments that followed the OMO rate hike by the CBN on Thursday.

In the coming week, we expect interest from local clients to keep yields moderated, but with slight bearish pressures still expected to persist.

Treasury Bills

The T-bills market reversed losses from yesterday’s session, as market players hunted for yields on the shorter end of the curve, following the significant boost in system liquidity from the net OMO credit, retail FX refunds and Paris Club refunds in the previous session. The Longer end of the curve however remained slightly pressured, with yields closing c.20bps lower on the day.

Opening next week, we expect the market to remain relatively tempered, with inflows from FAAC payments expected to further bolster system liquidity. We however expect yields to become slightly pressured as market players look forward to the PMA on Wednesday, whilst also expecting a further OMO auction on Thursday, with uncertainties around the current spate of rate hikes by the CBN.

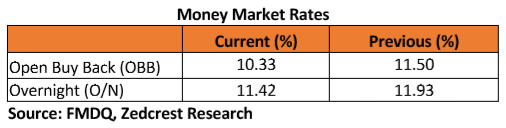

Money Market

The OBB and OVN rates moderated slightly in today’s session to 10.33% and 11.42%, as the market was awash with liquidity from the Retail FX refunds and Paris club payments in the previous session. System liquidity which opened the day at c.587bn positive, is expected to close the week at c.₦237bn, due to outflows (c.₦350bn est) for a Retail SMIS by the CBN.

We expect rates to trend lower opening next week, with inflows from FAAC payments (c.N382bn) expected to further bolster system liquidity.

FX Market

At the Interbank, the Naira/USD spot rate remained stable at ₦306.55/$, while the SMIS rate depreciated by c.0.08% to ₦362.82/$. At the I&E FX window a total of $118.19mn was traded in 480 deals, with rates ranging between ₦358.00/$ – ₦365.00/$. The NAFEX closing rate appreciated further by c.0.03% to ₦363.84/$ from ₦363.95/$ previously.

At the parallel market, the cash and transfer rates remained unchanged at ₦361.00/$ and ₦364.00/$ respectively.

Eurobonds

The NGERIA Sovereigns were relatively flat on the day, with slight buying interests witnessed on the short end of the curve. Yields were however higher by c.16bps w/w as news of the impending Eurobond issuance ($2.8bn) continued to weigh on sentiments in the market.

The NGERIA Corps were mostly flat, except for slight interests seen on the ACCESS 21s Sub and UBANL 22s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}