I was privileged last week to join the closing gong event for at the Nigerian Stock Exchange yesterday and to give a speech addressing the stakeholders of the Exchange. While we celebrate the inflow of foreign capital into local technology businesses, it is critical to consider both the long-term and short-term impact of this capital inflow.

In the short-term, there is the supply of capital and the badly needed expertise/non-financial support for technology businesses to thrive. This is critical especially in a market with poor infrastructure and a number challenges facing these businesses. Strategic counsel and expertise that comes with foreign capital are vital and necessary for the development of the local ecosystem.

The potential of Nigeria’s Digital Economy

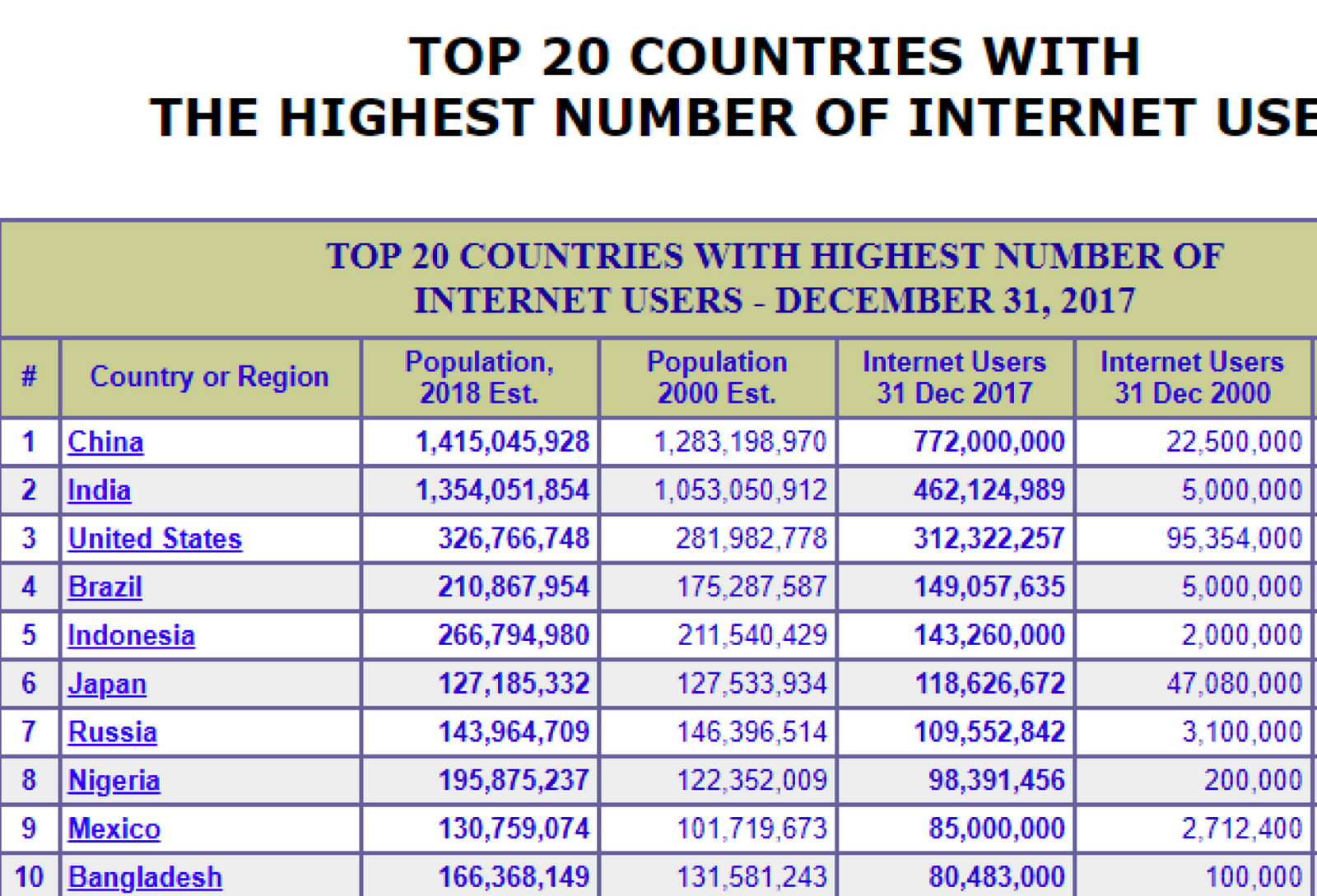

Nigeria is Africa’s largest digital market and the 8th largest country in the world regarding internet users. More internet users than the UK, South Africa, Egypt, Portugal, Spain and Italy, obviously due to mobile penetration and the country’s population.

This is both good and bad news. The good news is the size of the population/market with access to the internet while the bad is millions of unskilled/semi-skilled internet users with abysmally low purchasing power. Nigeria was recently crowned country with the world’s poorest overtaking India.

What does this mean? It’s simple when you look at the literacy & unemployment rate and the average age of our population; millions of poor uneducated people with access to mobile internet from Nigeria will be potential nuisance to a connected world…..this is a Medium publication for another day.

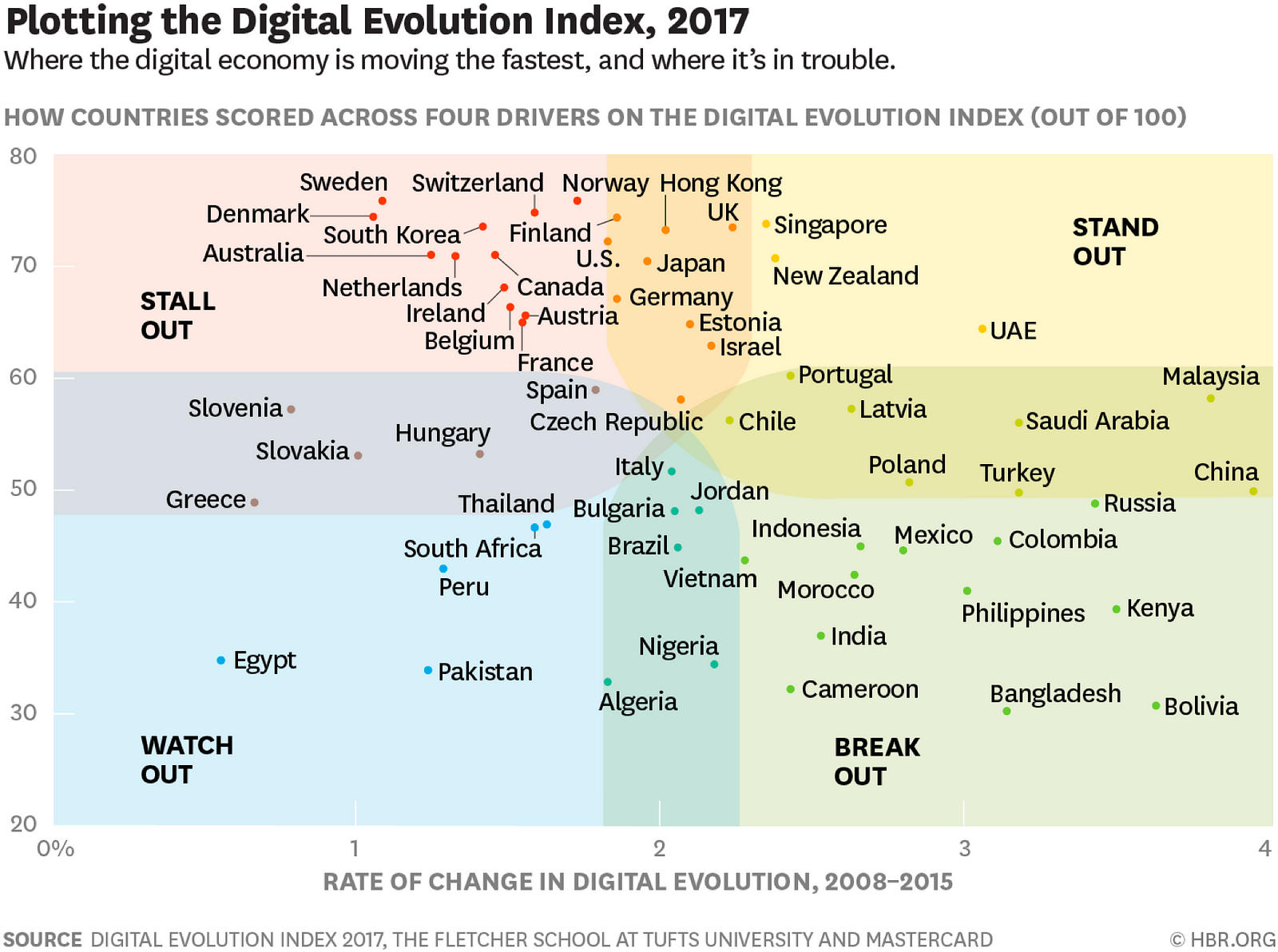

Let’s look at how the Nigerian digital economy is evolving.

From the above chart, Nigeria straddles Break out (Countries held back by infrastructure deficit though with huge potential to join the Standouts) and Watch out (Countries facing significant digitisation challenges). Nigeria has vast digital possibilities and with the right policies and infrastructure, the balance could tilt significantly raising millions out of poverty while moving Nigeria to the standout league.

The size of our digital economy or knowledge economy is enormous and potentially could be twice its current size within the next decade. The Nigerian economy of the future (a knowledge economy) should not be built with foreign capital alone; there must be a healthy mix of local and international capital.

Foreign Capital is building the Nigerian Tech Ecosystem

Let’s look at the news headlines over the last seven days.

Last Tuesday, Paystack raised $8m from some investors including Stripe and Visa, on Thursday UK Government announced 70 million pounds fund for tech and innovative start-ups in Nigeria during Theresa May’s visit. Yesterday our president signed a $328m facility for ICT development from the Chinese EXIM Bank. Funding this digital evolution shouldn’t be with foreign capital alone, there is a need for a hybrid of local capital from private investors, crowdfunding sources, local banks, government grants and foreign capital. The much bigger technology companies could get listed on the stock exchange reflecting the maturity of the industry and strengthening investors confidence.

While I do celebrate the good news received these past seven days, my favourite being Paystack (for obvious reasons), I cannot get past the fact that in one week over $406m in capital pledge is going into the technology sector from foreign sources.

Downside of building Tech Ecosystem exclusively from external capital

Is there any potential downside to this?

Of course.

The downside in building the ecosystem with foreign capital exclusively will be visible in the long term. A knowledge economy wholly owned by foreign companies/stakeholders. Our intellectual capital, proprietary assets, data will be domiciled offshore, solutions to local problems will be owned and controlled by foreign companies. Tax on revenue made in country will be paid to foreign governments while profit will be repatriated offshore. Whoever owns technology determines who has access and how the politics of the technology could evolve.

Whenever there is a change in technology usage by the society (which happens from time to time), there is a resultant impact on local politics and culture. With allegations that Russia relied on technology to influence social and political changes in Europe and the United State still being investigated, it is critical to have these considerations today.

Technology is powerful and has much more impact on a people and society than a lot of us can envisage. Whoever wields its power (inventors, shareholders and technology owners) are pivotal to the socio-political placidity of the society.

This is why as a people, we must think, deliberate and work towards our technology autonomy, our technology future and have an understanding of the status quo what my friend Nkemdilim Begho refers to as digital colonisation.

If the ecosystem is funded wholly by foreign capital, local investors will miss a great opportunity to sit on the table of the future economy. Interesting how Warren Buffet a seasoned investor admitted missing tech opportunities years ago because he didn’t understand the tech business model. Businesses need capital from any source so I will encourage wealthy individuals and organisations within the country to invest time and resources in building the local tech ecosystem.

It is one of the reasons I accepted to co-found Greentree to provide support for early technology businesses to thrive.

Nigerian Stock Exchange NSE is a viable option for the Tech ecosystem

The local bourse, the Nigerian Stock Exchange has taken some steps to encourage listing for smaller businesses. From my initial conversation and listening to the CEO of the Exchange Mr Oscar Onyeama last week, I learnt this is of great interest to the exchange and some steps have been taken creating possibilities for technology businesses to get listed.

An example of this is the Alternative Security Exchange and the requirements can be found here. A number of technology companies looking for capital have met these requirements.

Budding tech companies should aspire to list someday and there are a number of benefits of listing.

Let me try to break this down. It is important to note there are minimum requirements for listing. The benefits are:

- Access to Capital. This is critical especially in our market and being able to access capital unlocks the potential for your tech company. Do also note by listing your company more capital inflow from local and international investors is available creating value for your business and existing shareholders.

- Better transparency and Business Integrity. Due to the strict governance compliance requirements, your business becomes more transparent and sustainable de-risking the company further and ensuring longevity. The corporate governance framework is critical for long term growth of a business.

- Risk of Ownership is spread creating more value for the shareholders while eliminating key man risk which is a common problem in the local ecosystem.

- With more tech companies listing, more venture capital or early stage deals will be encouraged as there are potential for exit.

- Listing incentivises employees while motivating and improving value for employees stock options.

Technology service and product companies like MTN, Interswitch, MainOne, Jumia, Iroko, Hotels.ng (great to see possibilities here), Piggybank, Wild Fusion, Andela, Farmcrowdy, Paystack, Anakle, Afritickets to mention a few could consider listing when they are ready to raise capital. Hopefully someday, creating opportunities for local and international investors.

El Dorado will be a tech ecosystem built by international and local investors in a sustainable manner creating a win-win scenario for all parties alike.

Abaiama is CEO & Founder Wild Fusion Group, Director & Co-Founder Greentree Investment Fund (Tech-focus VC) and a firm believer in the rise of Africa.

{kind=link}