- You would agree that the number of Nigerians keying in to the use of mobile banking apps keeps growing by the minute.

- These days, virtually every bill and monetary commitment can be transacted right from the comfort of your homes and at your convenience without rushing to meet up with bank working hours, viz a viz the queue that welcomes you each time you step into a banking hall.

- Nairametrics has continually reviewed these banking apps to ensure that they meet up to expectations of customers. In keeping with this tradition, we are reviewing them again to see which ones have stepped up their games and those that have not.

The advent of mobile banking apps

Banking reforms in Nigeria have seen many innovations, creativity and changes in the mode of operations of virtually all banks and their relationship with their customers. One of such amazing concepts that have become popular is deploying mobile applications to ease banking transactions across all banking platforms in the country.

It is simply a technology that creates an interface between a bank customer’s account on his/her debit card and a mobile phone. It is downloadable software which comes free of charge and is available on both Apple and Google Play stores.

Some of the applications are as lightweight as 7MB, while others are as heavy as 30MB, depending on the banks involved and the developers. Basically, it is to be assumed that all banks in Nigeria now deploy these mobile apps for the convenience of millions of customers who prefer to sit in the comfort of their homes to carry out simple transactions instead of queuing up for hours in the banking hall. The question which the average bank customer will want to ask is this:

“What is the advantage of these bank mobile applications?”

- Expenditure monitoring: These mobile apps help monitor your daily expenditure and give the user a real time bank expenditure statement, which he/she can find useful in doing monthly budgeting and other useful planning tips.

- An economic life saver: Considering the fact that one may end up spending huge sums of money on transportation to the bank frequently, depending on the dynamics of your business, the use of mobile banking apps makes economic sense.

- Time saver: Some individuals can spend as long as 2 hours trying to carry out simple transactions that can be completed within 3 minutes on your mobile phone. Time is money they say, and mobile apps help echo that sentiment.

- Ease of business: For business people, transfers can be made and goods sent without the buyer traveling or going to the bank to make a transfer. It’s so convenient, safe and fast for business.

Now the review…

The mobile banking app technology is awesome and a welcome departure from what we were used to a few years ago but in all sincerity, not all banks’ mobile apps may be providing the services they claim to be providing. In this review, we shall be looking at major banks in Nigeria and their mobile apps. Their special features and the pros and cons that come with each of their mobile apps will be highlighted. The review will be done alphabetically with the final ranking at the end.

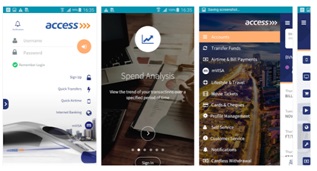

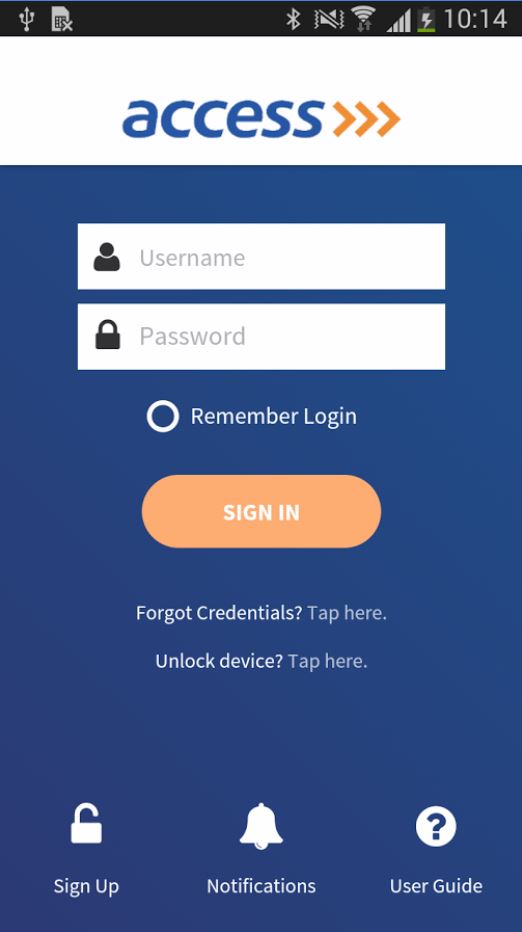

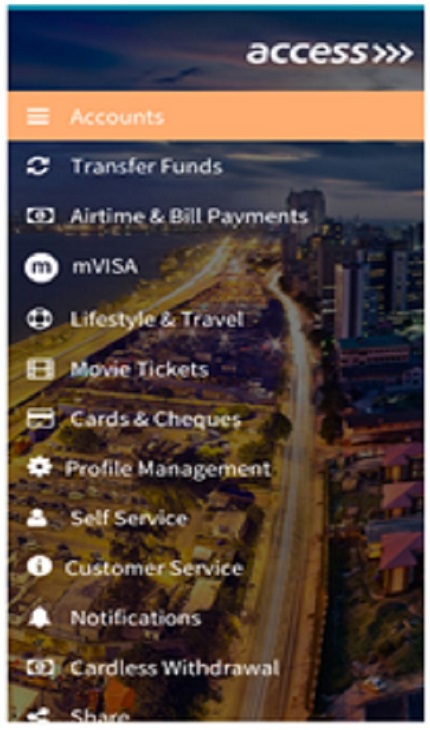

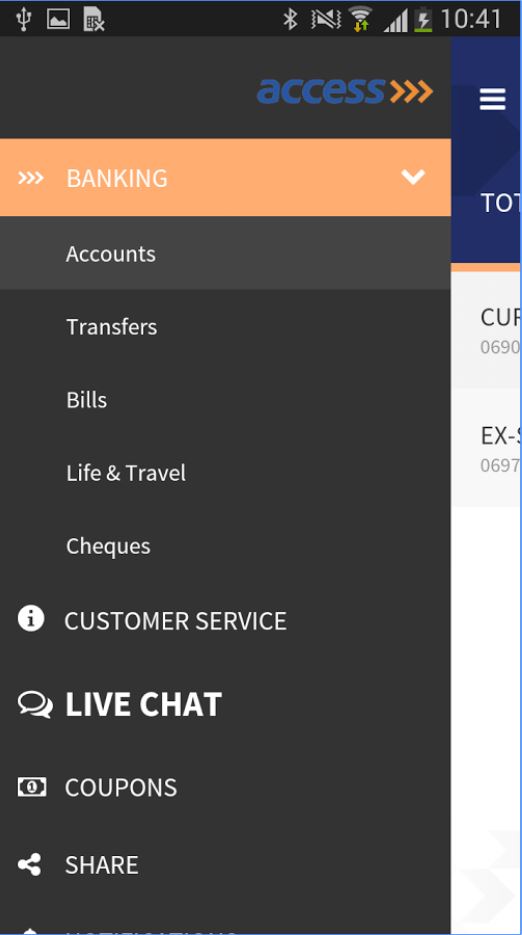

Access Bank

Access bank is one of the commercial banks in Nigeria that has grown impressively over the years. At first sight, the bank’s mobile app is astonishingly beautiful, with a lovely user interface to complement its easy navigation menu. We were wowed by its amazing features which included: quick sign up, quick transfer to any bank within the country, quick airtime purchase and top up, transaction analysis (mini statement of account), payment for Gotv, Startimes and DSTV and payment for utility bills like PHCN bills.

The app comes with a unique finger print authentication as an added security feature. Users of this app do not need a token to perform online transactions. The mobile app also provides a live chat feature that enables customers to get help at any point when they encounter difficulties. It is a stress free app that makes the customer feel at home. For example, one can order a fresh cheque book via the app without going physically to the bank.

Users’ complaints

One of the frequent complaints has to do with the slow speed of the app, especially on phones with low RAM (2GB and less). The app does not have ‘save beneficiary’ features, so one has to input beneficiary details each time a transfer is to be made. The updated version is not popular with customers as it comes with numerous glitches like finger print not working and inability to log in. Most of the icons on the app also go blank and become invisible.

Summary: 500,000 downloads, 61% positive reviews and a negative review of 7% from a total of 7,164 users of the app.

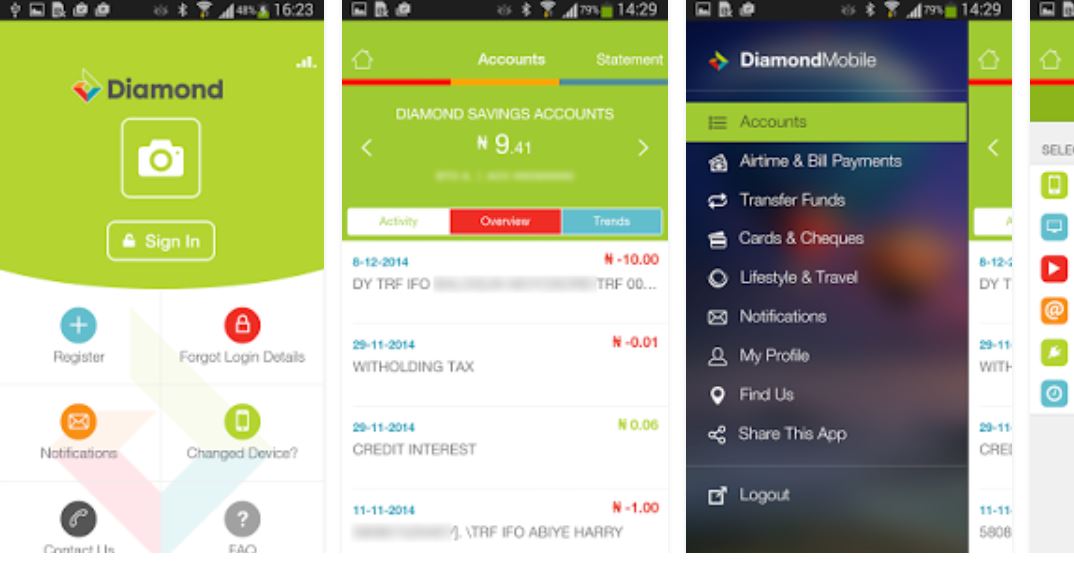

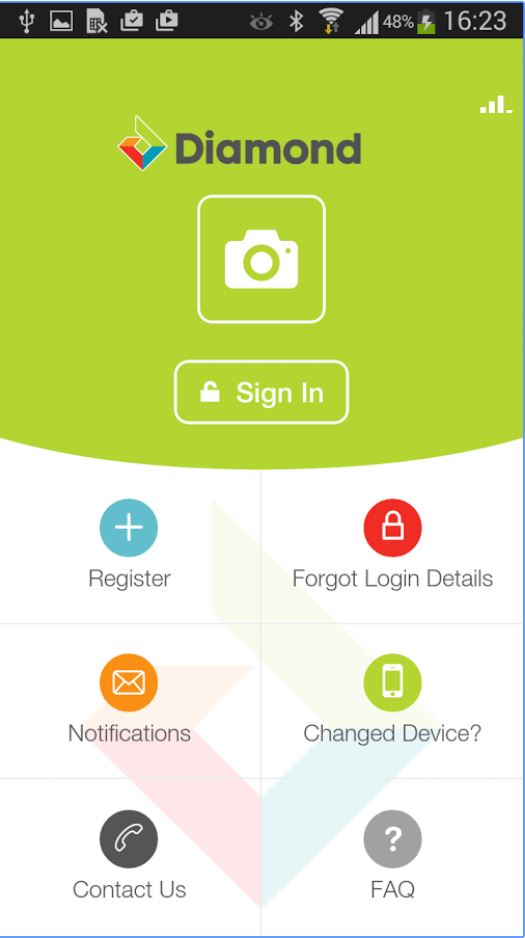

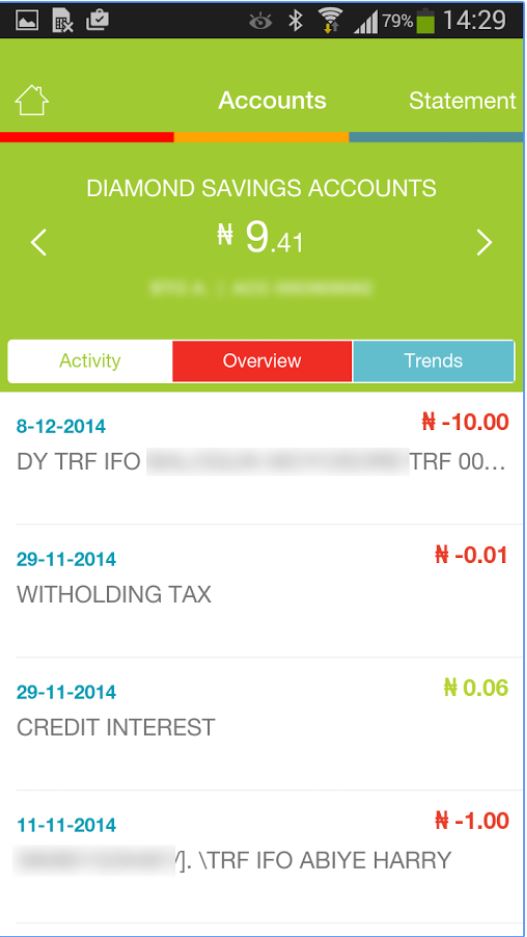

Diamond Bank

With its slogan as “Your Bank”, the bank truly deserves special mention with its deployment of a state-of-the art mobile app that has a beautiful interface. A first time user of the app won’t have problems navigating through, as the Sign in, new user registration, forgot login details are all clearly visible on the app. One can access his/her savings account overview, bank statement and carry out airtime top up and inter/intra bank transfers with ease. The app can also be used conveniently to pay utility bills and make cable TV subscriptions.

The beauty of the Diamond bank mobile app is that it comes with a 2 level security feature. What this means, is that you can create your unique password and also generate a customized four digit PIN. The implication of this security feature is that even if your password is compromised, before any transaction can be authorized, your PIN must be validated. The app is rated highly among customers; it is so convenient that it does not require a token to perform transactions.

Users’ complaints

On the flip side, customers complained of the deactivation of their apps if they don’t use it in a week. Another common issue was that of account balances not updated unless users re-log in. The newer updated version of the app brought a lot of issues like slow loading time of the app and inability to log in.

At other times, the app has doubly credited accounts for just 1 transaction. Another issue is that you can’t ‘exit’ the app normally; it just keeps going back and forth. It is only when left dormant for a few minutes that you can effectively exit the app.

We will be remiss in our review if we don’t mention the ‘eSUSU’ segment of the app which enables you to save a particular amount regularly, for a specific period of time. The edit of time does not work. It is set to frustrate someone if care is not taken. Let me explain: Let’s say you set the 31st of each month for a specified sum of 20k to leave your account and on that 31st, you have no money yet. It forfeits that month and even if you want to send in money on the 1st, you can’t, because you would not be able to edit the day, or anything else for that matter. A call to customer care isn’t going to work magic either as they can’t help you edit from their end.

Summary: 1 million downloads, 60% positive reviews and 9% negative reviews from 13,707 users of the app.

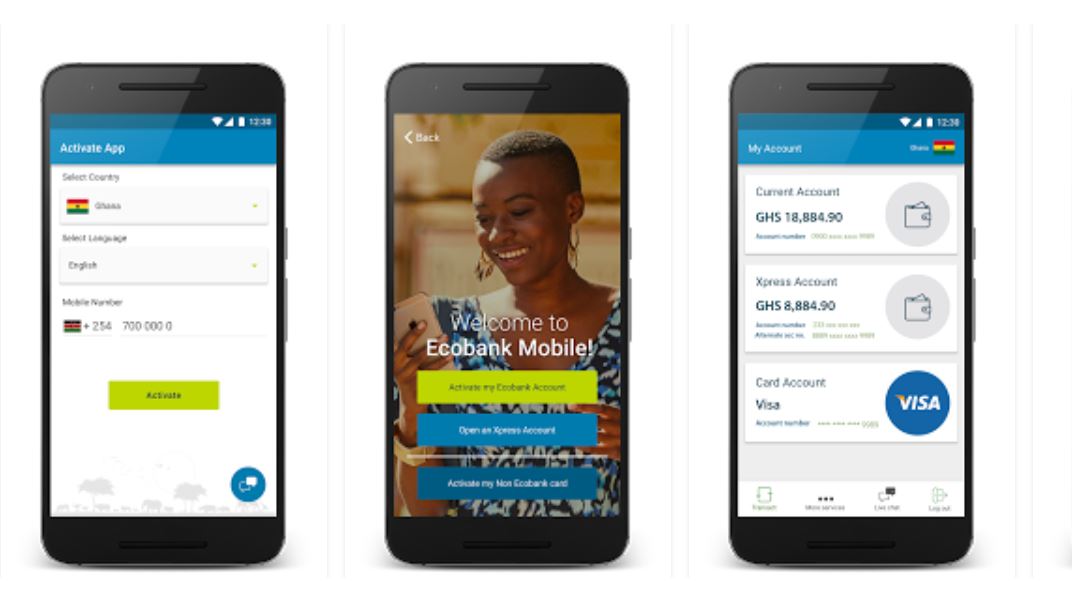

Ecobank

The number of downloads of Ecobank’s app, rivals that of Diamond bank. The app is very useful for interbank transfers, airtime top ups, statement viewing, and payment of internet and cable TV subscriptions.

Log-in is made simple, as a customer just has to input his/her mobile number and password to gain access. Response time for users is extremely fast and the app has a unique payment system for merchants who deploy the scanning of barcode or QR Code.

Users’ complaints

Customers view the use of mobile phone numbers for user ID as a huge security breach.

The app is very heavy at 72MB which is inconvenient for those with small storage sizes.

Funds cannot be transferred to other countries even though the features are present in the app. Updated versions come with numerous glitches like inability to login or logout.

Customers’ can’t log out even when they click logout menu thus making it vulnerable to hackers.

Summary: 1 million downloads, 58% positive reviews and a shocking 14% of negative reviews from 8,754 users of the app.

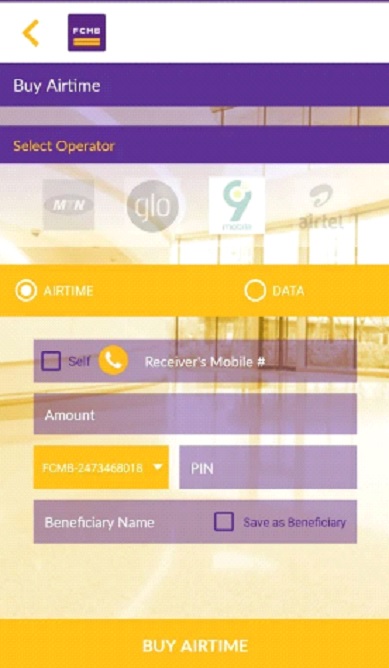

FCMB (FcmbMobile)

The FCMB mobile app is a personalized app that welcomes users by name whether in the morning, afternoon or evening. It has a simple yet lovely interface that requires just a phone number and password for logging into the app.

New users can easily sign up within a few minutes and start enjoying the numerous features that come with the app. Besides the usual inter and intra bank transfers, the app can be used for the payment of bills, top up of airtime, fund transfer and internet subscription.

Transactions on the platform are pretty straightforward because the icon descriptions and subsequent fields in drop-downs are unambiguous and easy to follow.

Users’ complaints

The complaints are similar to those for other mobile apps. Most users complained of receiving “Wrong PIN “error messages whenever they wanted to log in even when the PINs were correctly entered. Another significant drawback of the app is the fact that it keeps crashing during new user registration process.

Customers who change their phones and download the app once again have observed that they had issues with the app not working.

Summary: 100,000 downloads, 57% positive reviews and 11% negative reviews from 3,204 users of the app.

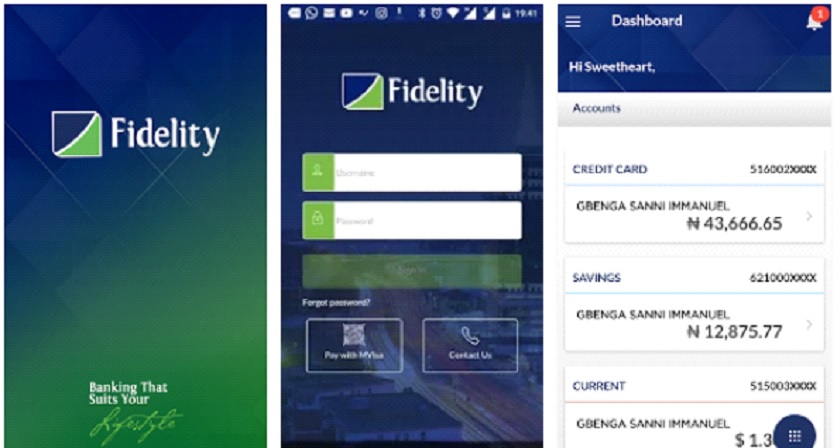

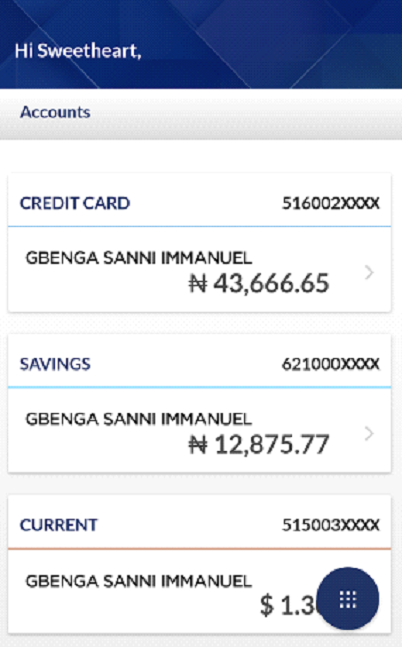

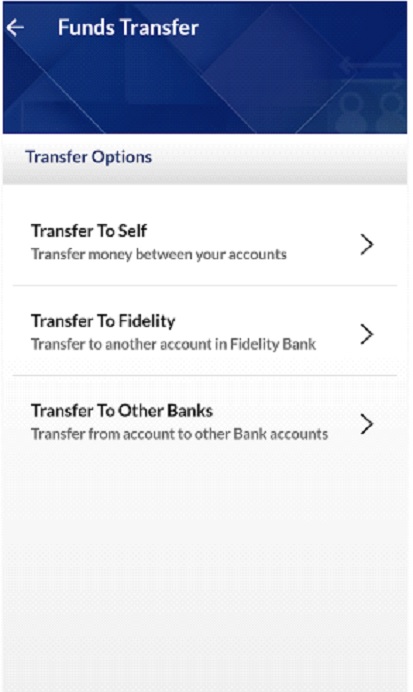

Fidelity Bank

Fidelity’s mobile app is not so popular, but it has an attractive interface and simple design which gives a lot of room for consideration. The user has more than 10 features to choose from the array made available by the bank via this 9.76MB app. Normal transfer to any bank in Nigeria is made available via the app by a simple click.

The app comes with a customized biometric/finger print authentication for easy and safe login operation. Users will have the opportunity to view all their accounts within the app. The app comes with a personalized profile feature, with provision to upload your profile picture. You can manage beneficiaries for fund transfers, payment of bills and airtime top up. Payments of PHCN, Gotv and DStv subscriptions are also possible via the app. One can easily generate account statement within minutes.

Users’ complaints

There is no email verification during sign up and also during password recovery. This is a serious loophole in the app. Those who log in with biometric/finger print require extra three steps to exit the app. To carry out transactions over N200,000, the app requires a hardware token which costs N3000. Also, updated versions come with numerous bugs.

Summary: 100,000 downloads, 55% positive reviews and 15% negative reviews from 1,808 users of the app.

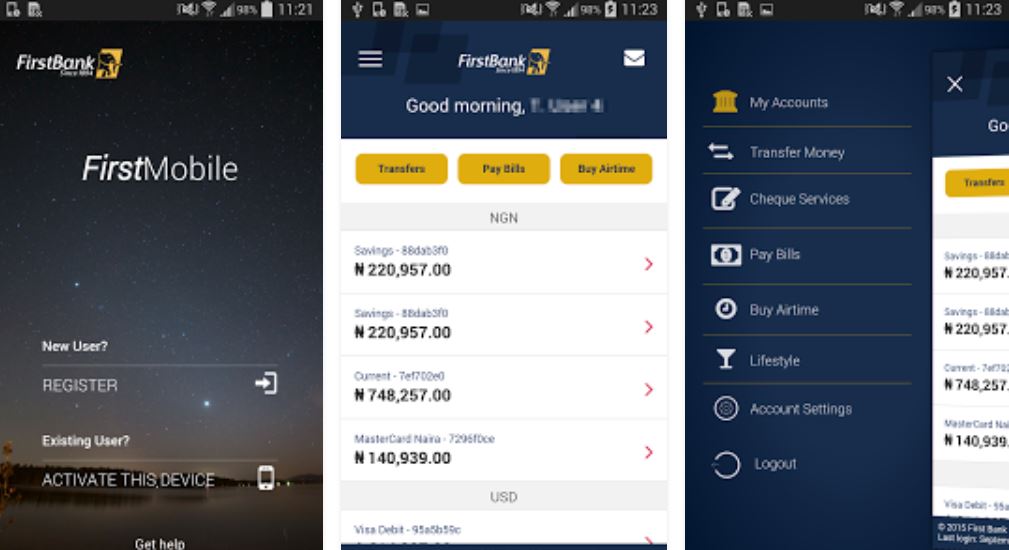

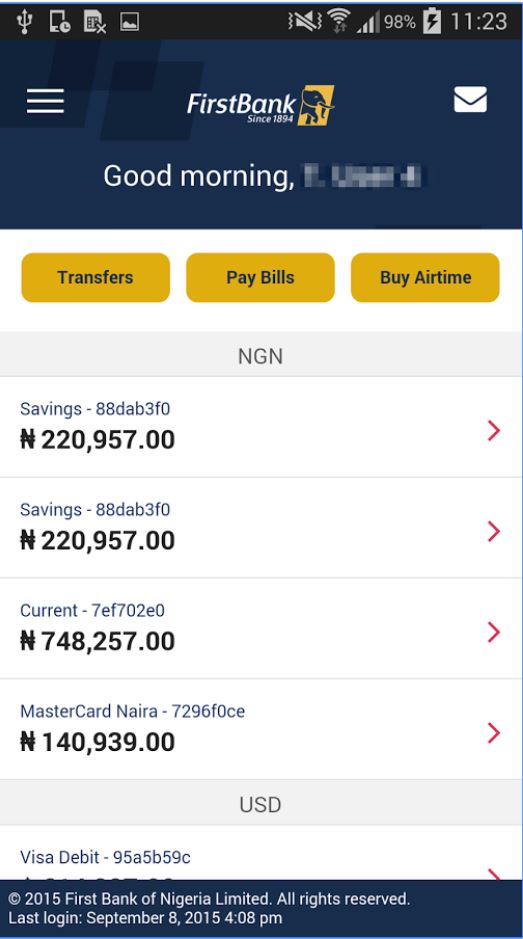

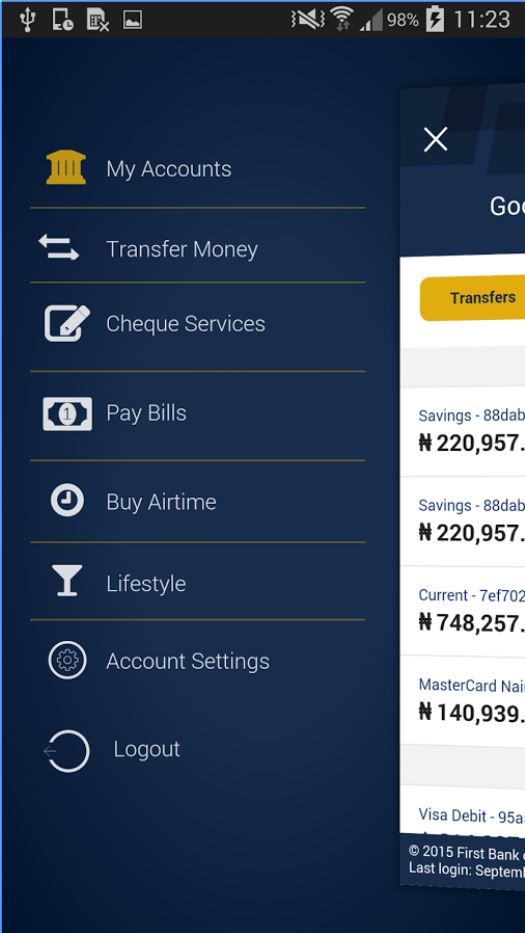

First Bank (FirstMobile)

The First bank mobile app which is popularly called FirstMobile ranks among the best in Nigeria. A peep into the FirstMobile app revealed interesting features, which are likeable and user friendly.

First of all, a first time user is given a 5 digit mPIN while registering. This PIN is needed for logging into the app, before you can carry out any mobile transactions. You also need to input a 4 digit transaction PIN which is used for completing any transfer or payment transactions. It is the only app that allows the transfer of a maximum one million Naira without the use of hardware token.

It has a nice user interface which can be used for not just interbank transfers, but also intra bank transfers. It can be used for purchasing airtime, paying for DSTV, Startimes, Gotv and PHCN bills. It can generate statements of account instantly and even bring back records of transaction up to 2 months back. The transaction successful receipt is beautifully designed and on the account setting, one can easily change his/her mPIN, change his/her nickname, synchronize your token to the app, change transaction PIN and carry out other operations.

Users’ complaints

The FirstMobile though, also comes with some complaints, with some customers complaining about the updated version of the app, which comes with lots of bugs like freezing the transfer pages and login problem. The newer version of the app also requires OTP (one time password), which is a unique 6-character code that can only be used once and is sent only to your registered mobile number as an additional measure of security.

Summary: A total of I million downloads, 65% positive review and a 6% negative review from 13,104 users of the app.

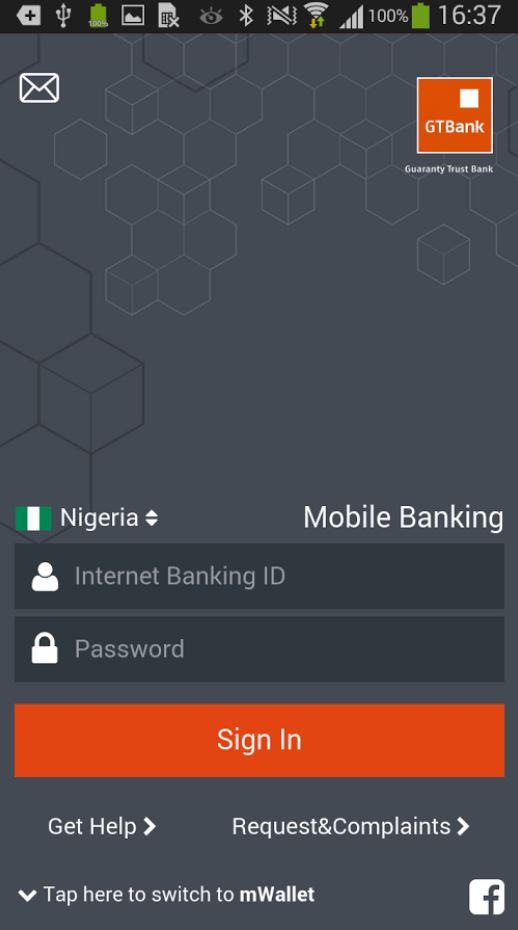

GTBank

The GTB mobile app’s beautiful orange background design makes it enticing and cool for the user to navigate and experience the unique features that the app brings. Log in is simple, as it requires just your internet banking ID and password.

To access your mWallet, you need to input your mobile number and unique PIN. Once you successfully log in, you can view all your accounts (savings, current, fixed deposit, domiciliary) and carry out other transactions like fund transfers, buying airtimes, checking daily history of transactions and ordering for new cheque booklet.

The interface is simply scintillating. One unique feature that comes with the app is that all transactions are done via a token to enhance security.

Users’ complaints

Customers complain of the OTP taking a very long time to arrive and sometimes this prevents successful login as invalid OTP error is highlighted. The app is connected to GTB’s network, so once GTB network is down, the app becomes non-functional. The recent updated version of the app comes with numerous bugs. Sometimes money transfers multiple times when a single transfer is made.

Token validation is complicated. There is a limited number of beneficiaries to add for transfers; you have to add a beneficiary before you can make a transfer and you cannot delete the beneficiary again after that. Registration requires OTP for completion, unfortunately the code sometimes takes forever to arrive. Also, the airtime top up menu is not functional.

Summary: A total of 1 million downloads, 56% positive reviews and 9% negative reviews from a total of 14,537 users of the app.

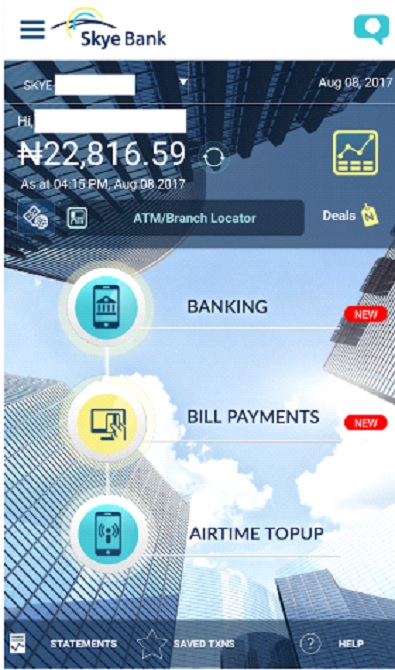

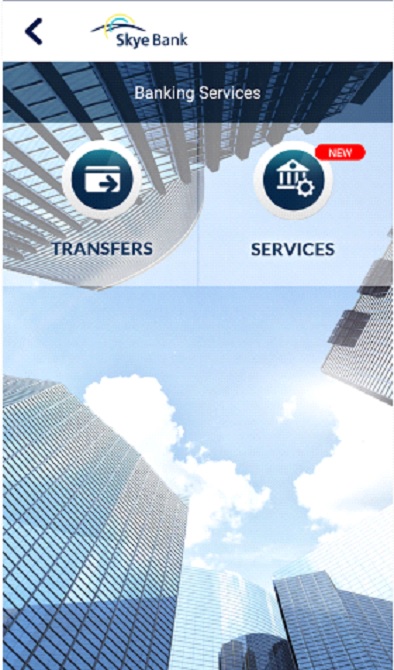

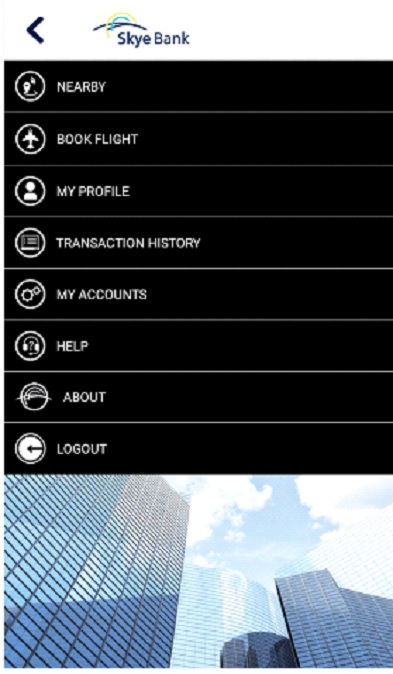

Skyebank (Skyemobile)

The mobile app comes with some innovative features. It comes with an ATM/Branch locator and has a first of its kind feature called cardlex. This feature makes it possible to send money to someone without a bank account. The app also does all other common jobs of fund transfer, payment of utility and cable TV bills and airtime top up.

It has a beautiful user interface with a simple log-in procedure that requires only the user’s phone number and password. Its signup is menu is located at the homepage of the app and is quite smooth.

Users’ complaints

On the other hand, app users have complained about difficulties encountered during the registration process as it usually fails. Users are unable to view transaction statements up to three months back. There is also the incorrect password error message frequently received. As with most apps reviewed, Skyemobile’s updated version comes with numerous glitches that have precipitated users to clamour for the older version which is more stable and robust. There is the thorny issue of daily transaction limit of N1,000. To increase this, customers must visit a nearby branch of Skyebank and fill a form.

Summary: 100,000 downloads, 54% positive reviews and 6% negative reviews from 3,973 users of the app.

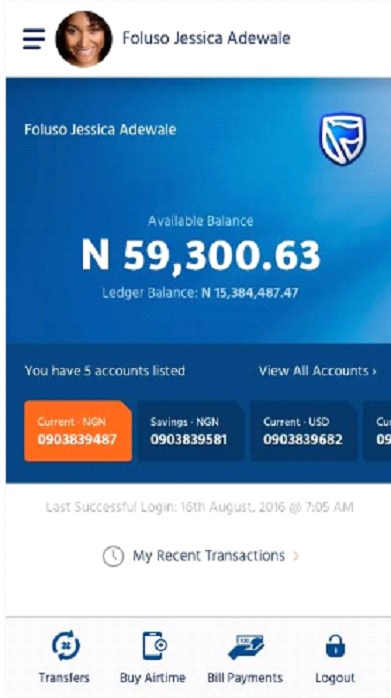

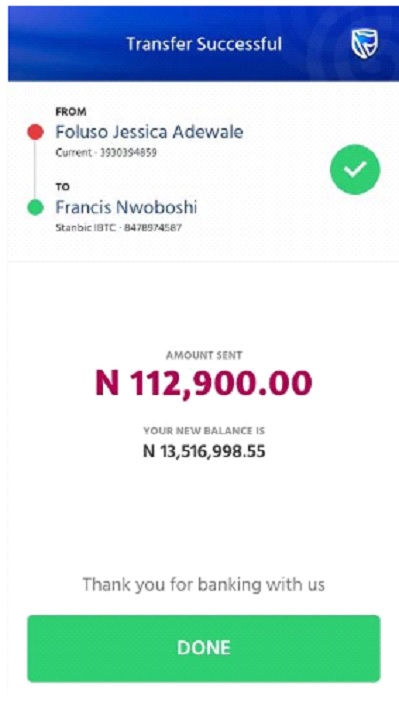

Stanbic IBTC Bank

The Stanbic IBTC mobile app is linked to a Stanbic IBTC debit card and usually requires a 3 digit installation code (*909#) to complete the installation of the app on any IOS or Android device. The app is useful for the payment for goods and services, school fees, bank transfers, airtime purchase even when one is outside the country and payment for internet and cable TV subscription.

It is connected to your savings/current account wallet, pension and mutual fund accounts as well as other linked accounts. At log-in, one can easily view his/her available account balance, ledger balance and all listed accounts. Users can also view their most recent transactions.

The app has the ability to manage financial portfolio with ease. One can also send money to people without bank accounts. A voucher will be sent via SMS to the beneficiary for withdrawal at any Stanbic IBTC ATMs.

Users’ complaints

The first complaint about the app is its huge size. It is 34MB which is quite large for the average user who struggles for connection daily. Connection error during log-in is a common complaint among users. Some users complained about long hours it took before recipients would receive an alert of transfer after their accounts had been debited.

Again, the recent updated version comes with bugs that prevent it from performing optimally. Old transactions cannot be shown, only recent transactions.

Summary: 100,000 downloads, 61% positive reviews, 13% negative reviews from a total of 1,671 users of the app.

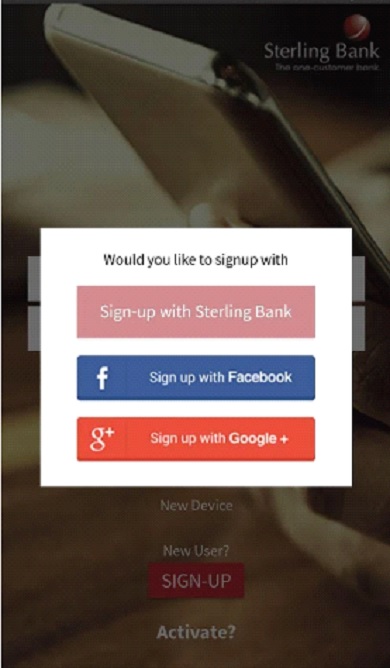

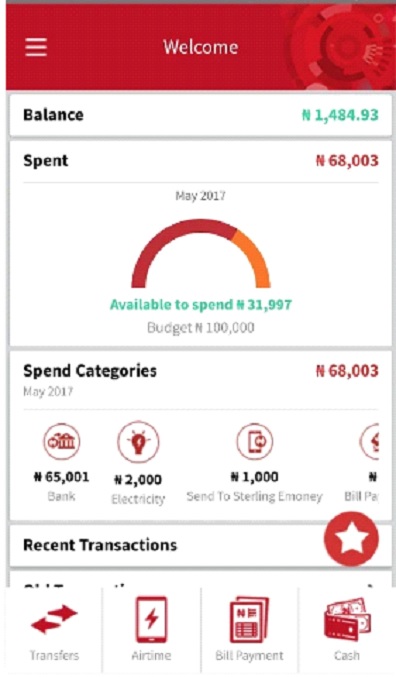

Sterling Bank

The bank’s mobile app offers seamless banking transactions on the go and comes with a not so beautiful interface. Log-in is made simple with the input of just a mobile phone number and a PIN.

The new user signup button on the app is also simplified for convenience of access during registration. The app does not do anything extraordinary, but it does come with a unique feature for budget/spend summary which is not present in other apps. This feature makes it possible to track how much you spend daily.

The app is also linked to your phone book contact. One can do the usual bank transfers, payment for goods and services, swift mobile recharge and payment for DStv, Gotv and Startimes subscriptions. You can set a monthly target of your expenses on the app. The occurrence of downtime on the app is minimal.

Users’ complaints

Going through the app, one can observe that the usual complaints from customers of the app were the same as other apps. The little glitches experienced were associated with upgrade to the recent version of the app. Most users who changed phones and downloaded the app observed that it no longer worked. These and other log-in issues were similar to other banks mobile apps.

Summary: 100,000 downloads, 62% positive reviews, 16% negative reviews from a total of 2,051 users of the app.

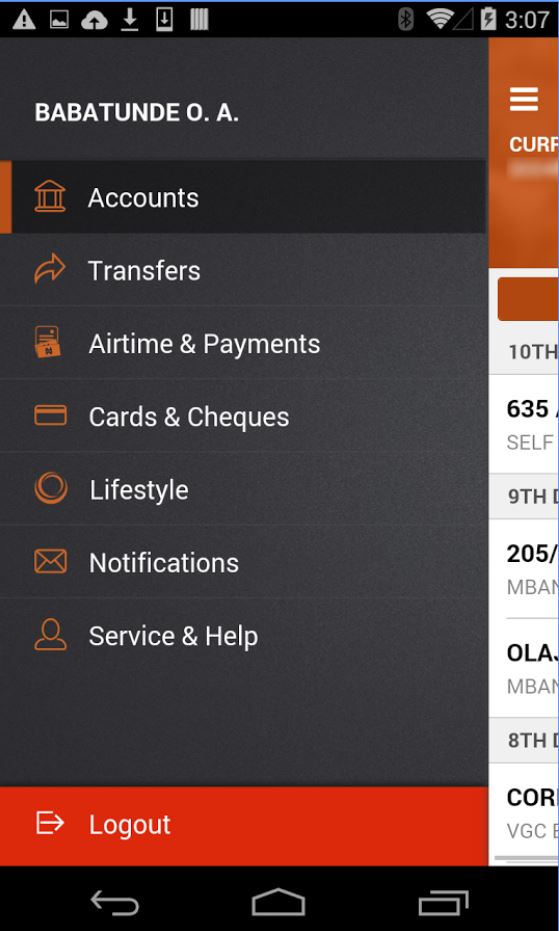

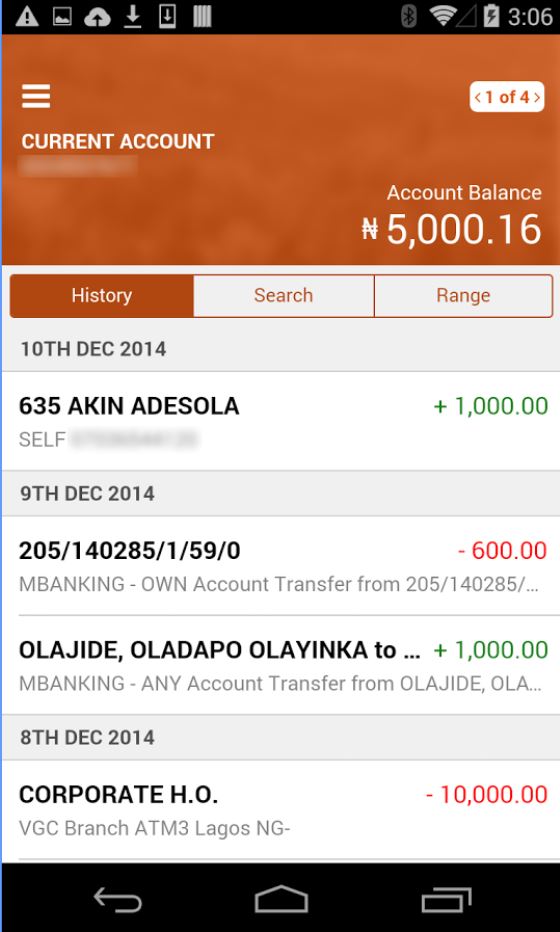

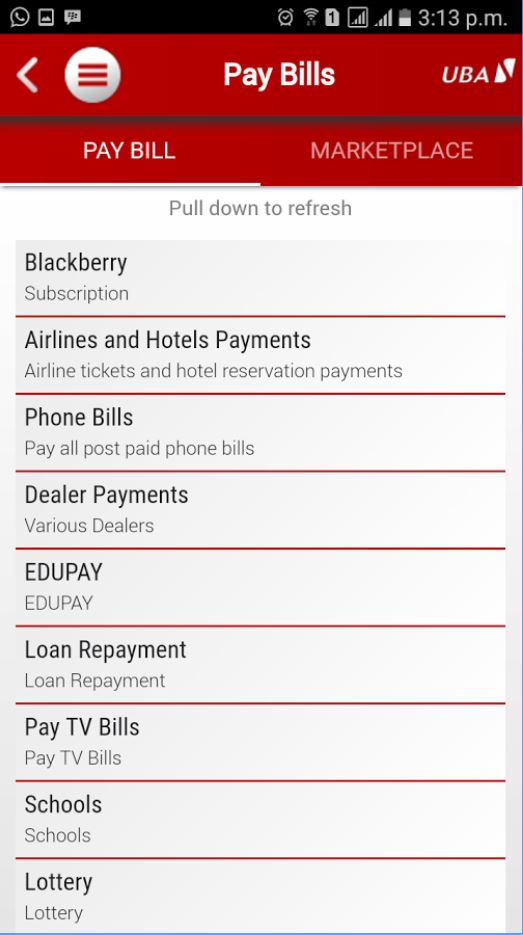

UBA (U-mobile)

The U-Mobile is one of the most popular mobile banking apps in Nigeria. The app is beautifully designed with a red and white user interface background. It comes preloaded with all important icons for carrying out money transfer, buying airtime, payment for bills, blackberry subscriptions, airline ticket and hotel reservation booking, DSTV, Startimes and Gotv subscriptions, school fees payment and instant recharge of mobile phone.

As part of its functionality, the app must be linked to a UBA prepaid debit card, and it works fine on both IOS and Android devices.

Users’ complaints

There are few complaints from the app users like inability to log-in or increase daily transfer limits and problems encountered during airtime recharge. The current updated version has solved some of these issues, but it also has few bugs that tend to slow down the app. Account statement is presently limited to 3 months and getting access to backdated transactions for 6 months is not possible.

Summary: 500,000 downloads, 63% positive reviews, 7% negative reviews from a total of 8,092 users of the app.

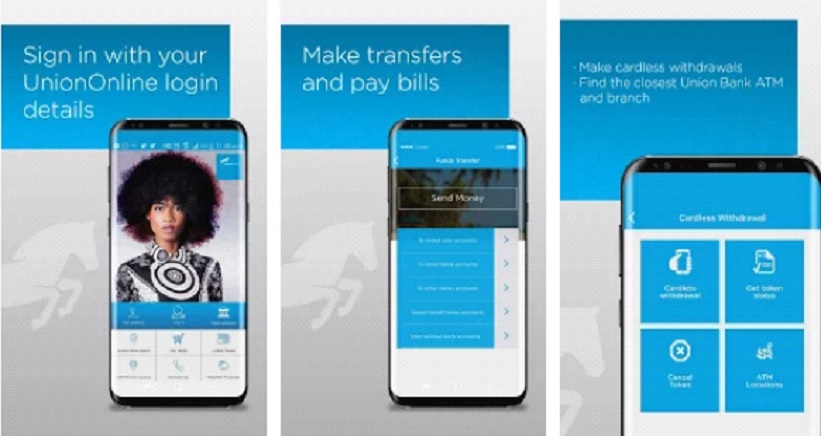

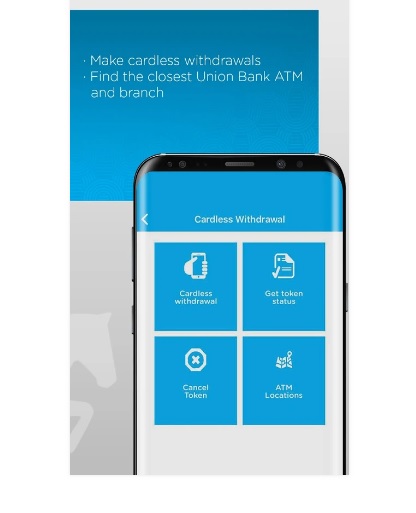

Union bank (UnionMobile)

UnionMobile comes as a pleasant surprise. A quick check on the mobile app shows that Union bank, which usually sticks to the traditional style of banking, has deviated from its rigid stance and created an app that stands among the top ranks in terms of beauty and functionality. The app contains some common and also unique features like: ATM/Branch locator, Instant account statement, Weather forecast, Manage and save beneficiaries, and Personalize profile where one can upload his/her profile picture.

The app also operates a card-less withdrawal system, where a beneficiary can make withdrawals from any of Union bank ATMs without the use of a debit card. This can be done after linking your debit card details to your profile.

The app is quite handy considering the fact that one can make the usual transfer of fund to other banks, make payments for various subscriptions and utility bills and do top up of mobile phone. As usual, it does the normal day to day transactions expected of a mobile app.

Users’ complaints

A quick check will reveal quite a lot of negative comments about the app. It is not reliable especially when in urgent need of funds. Secondly, the security features are not enough, hence many users are hesitant to use the app for fear of being hacked. To compound issues, the app does not have receipt for successful transactions done as the feature has not yet been installed. There are multiple issues associated with the updated version as users cannot log-in using the username option since it wasn’t there in the older version.

Summary: 100,000 downloads, 68% positive reviews, 8% negative reviews from a total of 740 users.

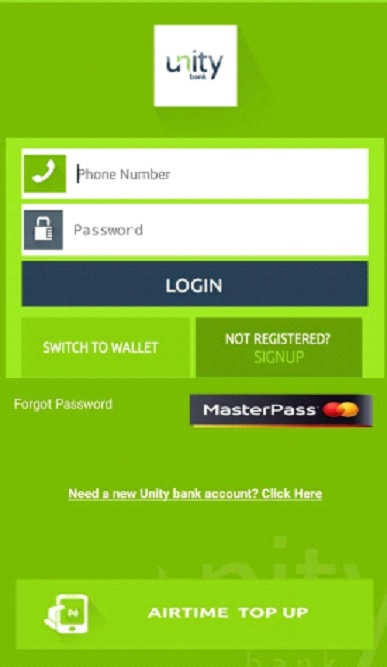

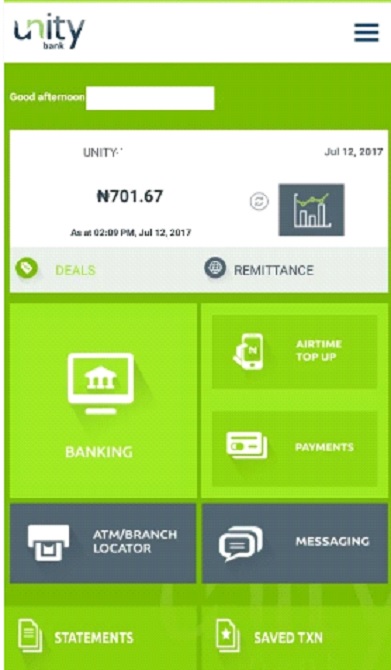

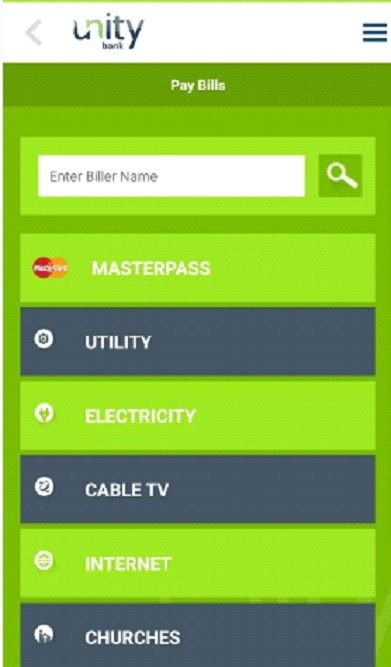

Unity bank (Unity Mobile)

The growth of the bank has stalled over the years and it is a miracle that they have a mobile app called Unity mobile.

The app has a simple look and contains the usual features as with other apps: ATM/Branch locator, instant mobile top up, fund transfer, payment for utility bills cable TV. One unique aspect of the app’s airtime top up feature is that its link is strategically designed at the bottom of the app and you can use it to top up without actually logging into the app.

Users’ complaints

The app has some downsides as expected, with so many users complaining of their inability to access account statements real time. There is the worrying issue of daily transaction limit pegged at N1000. The new updated version makes transfers to other banks, log-in and checking of account balance difficult. The app developers need to update the current version 3.0 to clear the existing bugs.

Summary: 100,000 downloads, 57% positive reviews, 11% negative reviews from a total of 976 users of the app.

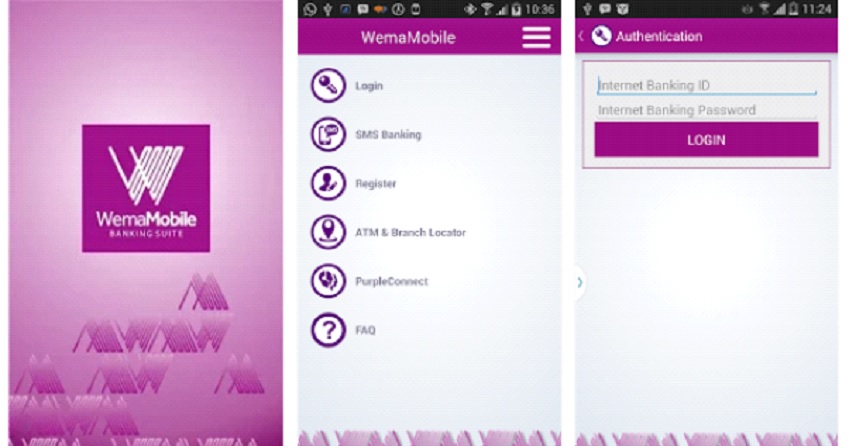

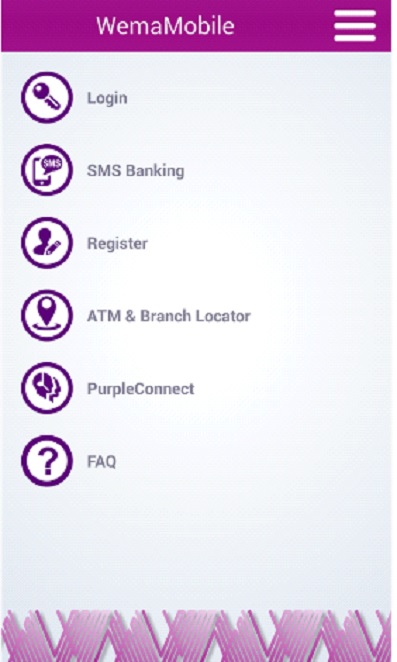

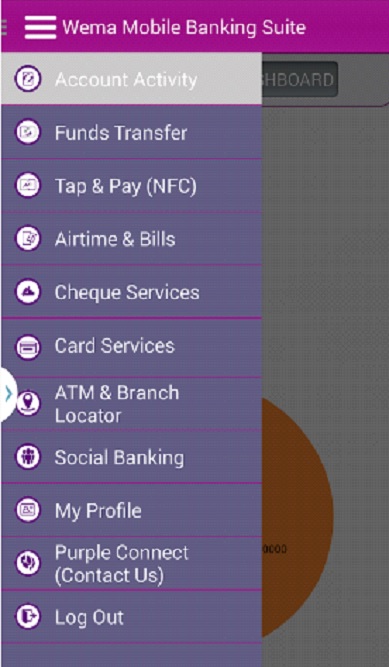

Wema (Wema mobile bank suite)

The Wema bank mobile app is one of the most beautiful apps in the banking sector. The beautiful purple background of the app welcomes users to its simple features which include the log-in, SMS banking, register and ATM/branch locator icons.

The app uses customers’ internet banking ID for authentication, while it uses the internet banking password for login. The app can be used without internet connection and it’s easy to navigate. The card control feature that comes with the app is the first of its kind in Nigeria.

The Wema mobile bank suite comes complete with facilities for cheque request and blocking, and can be downloaded from Google play store. It does the needful fund transfer, airtime top ups, payment for utilities and purchase of movie tickets.

Users’ complaints

Unfortunately, the app can’t be used without a token which presently costs N2000. Some users complained of difficulties experienced in installing the app on their IOS and Android devices. Difficulty in registration and doing transfers, airtime top up and payment of bills is also rampant among app users.

Summary: 100,000 downloads, 71% positive reviews, 8% negative reviews from a total of 863 users of the app.

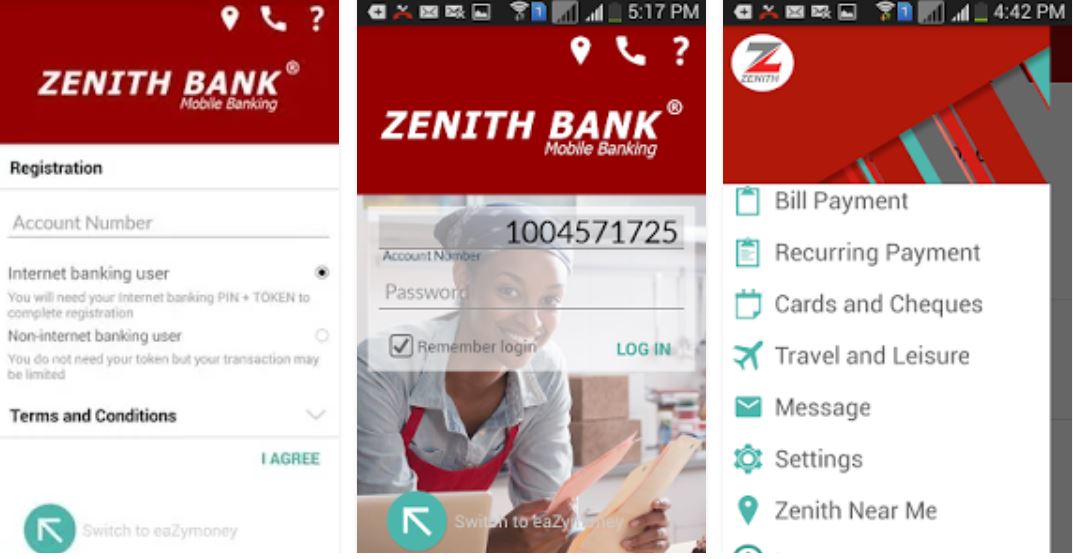

Zenith bank (Zenith Bank Mobile)

Zenith Bank Mobile was created to enhance efficient and convenient banking for its more than 3 million customers nationwide.

With its beautiful white and red interface background, the app requires users to input their account number and 6-digit passwords, before they can log in to their profiles on the app. Cheque and card request, funds transfer, self-transfer, airtime purchase, payment of bills, payment for hotel lodging and branch locator are some of the main features on the app.

Users’ complaints

To most users however, the app is not user friendly due to the stress they encounter while trying to log in to the app as first time users. Registration requires OTP for completion which could take a while to be sent. The app also requires hardware tokens for all transactions above N100,000 which is often cumbersome.

Summary: A total of 1 million downloads, 64% positive reviews and 6% negative reviews from a total of 6,450 users of the app.

Review over and…

Giving a review of the banking mobile apps in Nigeria won’t be complete without a fair assessment of their functionality and true usefulness to the day to day banking needs of Nigerians. Unfortunately, most of these apps have challenges due to our weak internet network in Nigeria.

This has rendered most of the apps ineffective and caused most users to resort to visiting banks for their various transactions; a situation which negates the initial idea behind building these apps.

Every app usually has bugs which tend to create problems for the end user, but the ultimate test of an effective app is the wider acceptability, popularity, user coverage and overall functionality within its customer base.

Based on these criteria, the banks are ranked from best to worst as follows:

WINNER – First Bank

FIRST RUNNER UP – Diamond bank

SECOND RUNNER UP – Zenith BanK

WORST – Unity bank

From the above, you can see that First bank has maintained its first place as owners of the best mobile banking app and Diamond bank has moved up to second place.

See previous ranking here and here for prior ranking positions.

We would stress though, that these mobile banking apps have to do better but then, we are thankful that the Nigerian banking sector has come this far. It is our candid hope that these observations will be looked into and improved upon in no distant time.

FINAL RANKING

- First bank

- Diamond bank

- Zenith Bank

- GTBank

- UBA

- Access bank

- Ecobank

- Skyebank

- Stanbic IBTC

- FCMB

- Sterling bank

- Fidelity

- Union bank

- Wema bank

- Unity bank

Article contribution, Chacha Wabara, Anna Urieto, Mudeerat Olawunmi, Ugo Obi-chukwu

{kind=link}