That’s right. You can actually get free petrol in Nigeria if you are lucky enough to be at a fuel station that is selling petrol at more than N145.00 per liter when the Nigerian National Petroleum Commission (NNPC) comes visiting.

Nigeria is a wonderful country, I tell you. We believe that market forces are like witches and wizards from the legendary Nigerian villages that have been sent to oppress the poor and suck our destiny dry.

So the back story is that the NNPC has been going on raids to clamp down on petrol stations that are selling fuel above N145/liter. Once they get there, they give all motorists who are there free petrol until it finishes. So you get free petrol, as much as you want, and when it finishes, you go back to the queue for more. The issue of fuel scarcity has not been resolved — it was just made unwittingly harder. Petrol stations are simply going to start hoarding the limited product they have now and sell only in the dead of the night. Yep, that is the true definition of ‘black market’.

So let’s talk about market forces, demand and supply, and how the cost of ‘free petrol’. Don’t worry, I am going to make microeconomics as engaging as possible, so stay with me.

Equilibrium

Once upon a time, the picture above was the equilibrium price for petrol in Nigeria. At N145/liter, Nigerians consumed about 40 million liters of petrol per day. At this point, supply and demand were at equilibrium and the petrol sector of the economy was ticking over at N5.8 billion revenues per day.

Then the music stopped.

We started hearing stories and grumblings that landing costs of one liter of petrol was now N170. Just like that. And we were busy paying N145. The signs were ominous and it became apparent that a scarcity was on the way. First petroleum marketers were blamed for hoarding products, and then Nigerians were blamed for panic buying. Meanwhile the queues got longer. What just happened?

Apparently, the landing cost of petrol has jumped to N171. If the landing cost has gone up, then for petrol marketers to make any kind of meaningful profit, the pump price would have to be somewhat higher than N171. Well, because the regulated price remained at N145, petroleum marketers stopped importing petrol. Before now, petroleum marketers provided 80% of Nigerian’s daily needs, according to DAPPMA. So, if DAPPMA owned 80%, that means NNPC could only supply 20% of Nigerian daily needs, which accounts for 8 million liters per day.

Now, there is a supply shock. Look at the last picture above. Supply shock means that the supply curve will move left from Supply 1 to Supply 2. The supply curve will move along the demand curve, thus moving the from Equilibrium E1 to Equilibrium E2. At E2, the price of petrol has to go up, according to the law of supply and demand, until demand drops to 8 million liters per day. At this point E2, the price should be somewhere around N200 per liter or more. So we are looking at a margin of around N29 per liter or more to cover for costs of transportation, taxes, other levies and profits.

This is how supply shocks affect economies. Assuming a pump price of N200 per liter, all of a sudden, the vibrant downstream petrol sector that was ticking merrily at N5.8 billion per day has dropped to about N1.6 billion.

In a market driven economy, it will be difficult for the price to stay at N200, when the supply just dropped by 80%. Prices should double at the very least until a clearing price is found. But this is Nigeria, where we are so suspicious of market forces that we believe everyone is a monster who is out to suck the poor dry. Therefore, we have to create our own equilibrium.

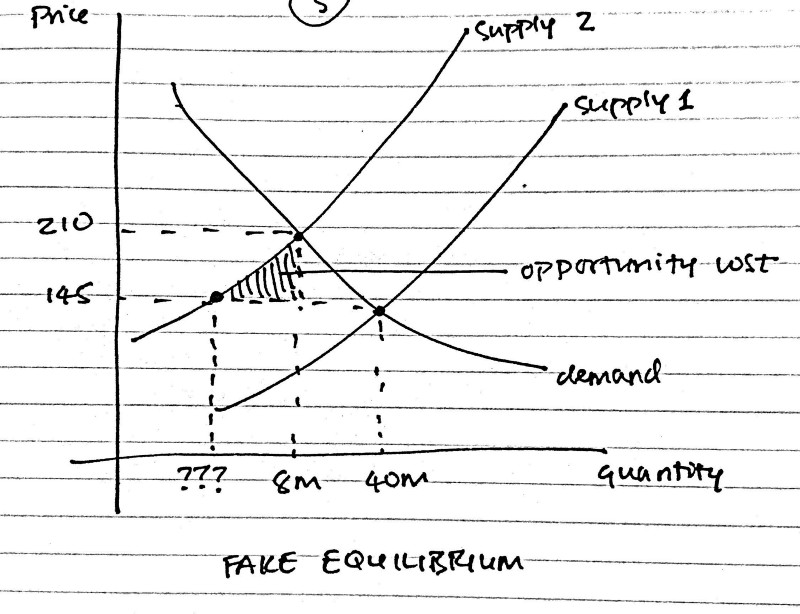

Fake Equilibrium

I call this new equilibrium, the fake equilibrium. The Government says the price of petrol is N145, therefore, the price of petrol is N145, because the poor must not suffer.

Now, this chart is a little bit complex.

We can see that the supply shock is still there and there is a hard cap of 8 million liters of fuel available per day. We are now operating along the Supply Curve 2, but we are stuck to the price at Supply Curve 1. What’s going on here? Can you see the “???”? That’s the volume of petrol per day that Nigerians actually get to buy at N145. No way in hell is everybody paying that N145, not even the poor masses we are protecting.

Only very lucky people who drive in, just when a petrol station opens, people with serious connections, and the rich people actually get to pay N145. The rest of us pay more. Now, the excess that we are paying above N145 is not necessarily in Naira and Kobo, but the opportunity cost of spending endless hours on fuel queues. The time that we could have spent on more productive economic activities is wasted on fuel queues.

The time you could have spent to gather your thoughts and come up with crazy ideas to move the country forward, you spend it on the road, burning fuel you don’t have to look for a long fuel queue to attach yourself to. And the painful part is that a lot of people spend hours on fuel queues only to be told that fuel has finished, and then you buy black market, at a minimum of N250 per liter, if you are lucky, to continue for another fuel queue hunt. All these things are costing the economy a huge loss.

Now, not only the masses are suffering. Even NNPC is suffering. Instead of them to do useful things, they are now hunting down fuel stations, stretching already thin resources, and burning scarce petrol to execute their N145 per liter mandate.

I have heard a lot of excuses that Nigerians are monsters and that if fuel prices are deregulated, they will collude to raise petrol prices through the roof. While I concede that there is a possibility of that happening, the Department of Petroleum Resources (DPR) should look for ways to ensure that such collusion does not happen. That’s what we are paying them to do with our taxes. Have we ever wondered why telecommunication giants have not been able to collude to raise calling tariffs through the roof?

When fuel prices were raised from N86.50 to N145, I saw a couple of petrol stations with fuel queues while others were virtually empty and I wondered what was going on until I discovered that the ones that had queues were selling at N143. That told me something. Many Nigerians were ready to stay on some queue because of N140 max (that is N2.00 per liter for maximum of 70 liters). Likewise, many others felt, that have better things to do with their time.

Now, I am not saying that NNPC should scrap their N145 per liter. But if petrol stations want to sell at N300 per liter, let them be. As long as NNPC stations are selling at N145, those who want cheap fuel can go and buy the cheap fuel. Economics allow for discriminatory pricing — those who pay for economy class and those who pay for business class are still going to fly from Abuja and land in Lagos. The extra comfort the business class tickets provide is worth it for some, but for many, it is not worth it. Let everyone find their level.

So, when I hear argument that petrol stations selling petrol at N250 are doing economic sabotage, I disagree. The real economic sabotage is not allowing everyone who wants to import petrol, import petrol.

There is a standard pricing for imported refined petrol. The DPR/NNPC should look for ways of allowing people import the products freely, agree to an embedded profit margin that will adjust with market prices, and let us all flourish.

{kind=link}