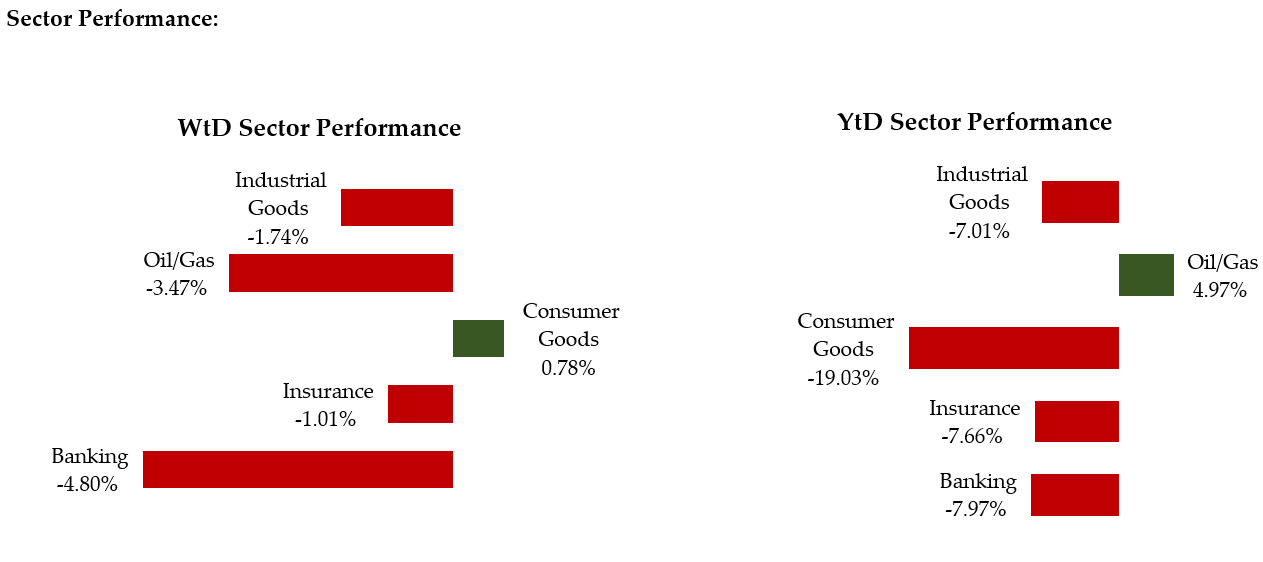

The market ended the week lower, as traders mulled over a raft of weak economic data (surging inflation and declining exports) as well as mixed corporate earnings. The week saw the tier-1 banks all reporting FY’2015 numbers. The numbers showed YoY growth in earnings and profitability. They however showed fourth quarter weakness, a reflection of the growing macro challenges. The banks also saw higher impairment charges. In that stride, the week started with Pan-African lender – ETI – issuing a profit warning notification, citing higher impairment charges in the last quarter. In spite of these challenges, the Banks announced dividend payments to shareholders with dividend yields in double digits.

The All-Share Index ended the week, dipping by 1.13%. The steepest declines came in from the Banks (-4.80%) on declines in the likes of ETI, ACCESS, WEMA & DIAMOND. The Oils were also weaker, on the back of profit taking in OANDO which had seen sharp gains in the preceding week. The Industrials saw moderate declines while the Consumers were higher on renewed demand for the likes of NB & UNILEVER which closed at the upper end of the range on Friday.

Market activity surged WoW, fuelled by off-market block divestment trades in UNITYKAPITAL & WEMABANK. Both trades accounted for c.50% of total market turnover (N18.338bn). The UNITYKAPITAL trade is in connection with the divestment of Unity Banks 50.3% stake in the insurance business in line with CBN directive that all banks divest from non-banking subsidiaries while the trade in WEMA represented c.17% of its total share outstanding. Outside these two names, activity was mainly in the shares of ZENITH, GUARANTY & WAPCO – the trio accounted for c.55% of total market turnover when we back out the off-market trades. The thinking on the street is that, the release of FY numbers brought in additional liquidity, creating an opportunity for offshore investors looking to exit Nigerian equities to sell into.

Market Snapshot

- All-Share Index: 25,679pts

- Market Cap (NGN): N84tn

- Market Cap (USD): $44.87bn

- Total Volumes Traded: 91bn

- Total Value Traded (NGN): N34bn

- Daily Average Value Traded – WtD: N67bn

- Daily Average Value Traded – YtD: N41bn

- Advance/Decline Ratio: 20/41

Sector Performance:

Market Screeners:

- Top Risers:

CONOIL (+21.38%; N20.10); UBA (+9.59%; N3.77) & LAWUNION (+9.38%; N0.70)

- Top Decliners:

OANDO (-25.23%; N4.00); ETI (-20.28%; N14.35) & ACCESS (-10. 63%; N3.95)

- Top by Volumes Traded:

ZENITHBANK (163.33mn); UBA (140.90mn) & GUARANTY (113.40mn)

- Top by Value Traded:

ZENITHBANK (N2.057bn); GUARANTY (N1.84bn) & WAPCO (N1.14bn)

- New 52-Week High:

UCAP (N1.78)

- New 52-Week Low:

7UP (N151.08); CAVERTON (N1.45) & IKEJAHOTEL (N2.35)

{kind=link}