Price and volume increases underpin revenue rebound

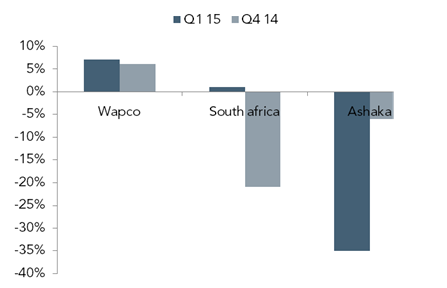

- Lafarge’s Q1 15 revenues rose 15% YoY to N57 billion, propelled by increases in revenue in the Nigerian (+14% YoY to N38.5 billion) and South African (+7% YoY to N18.4 billion) businesses. The rise in Nigeria was underpinned by higher prices (+8% YoY to N31,000 per tonne) and volumes (+7% YoY to 1.3MT) as an improvement in capacity utilization (+13pps YoY to 94%) at the WAPCO factory more than offset the drop in utilization (-24pps YoY to 47%) at the Ashaka plant due insurgents’ attacks and plant recalibrations. On the other hand, volumes in South Africa rebounded a modest (+1%), with favourable exchange rate translation of N1.6 billion buoying topline in naira terms. Thus, excluding the SA currency effect, Larfage’s group revenue is +12% higher YoY.

Figure 1: Change in cement volume growth

Source: Lafarge Africa presentation, ARM Research

Currency depreciation pressures gross margins

- Q1 15 COGS rose quicker than revenues (+24% YoY) to N39 billion reflecting pressures from devaluation of the naira as nearly 55% (our estimate) of the company’s input is exposed to currency fluctuations. Accordingly, though gross profit was flat (-0.1%) YoY at N18 billion, GM contracted 4.5pps YoY to 31.8%, relative to the average of 33.6% for the past 5 quarters.

- Q1 15 operating expenses increased 37% YoY to N7 billion, reflecting the upswing in WAPCO’s volumes as well as expenses related to ongoing product differentiation campaign being embarked upon by the company. Consequently, EBIT declined 14.6% YoY to N11 billion with related margins of 19.6% (vs. 26.45 in Q1 14).

Tax write-back tapers earnings pressure from UNICEM’s dollar loans…

- Q1 15 net finance cost surged 84% YoY to N315 million, driven by the sharper decline in finance income to N334 million (-58% YoY) relative to fall in finance charges (-33% to N649). Whilst contraction in the former is consistent with the 35% YoY decline in average cash balances to N16.5 billion, the latter tracks the ~90% YoY contraction in average debt levels to N17 billion. Furthermore, the company reported N2 billion share of loss from its UNICEM associate in which it currently holds 42.5% stake. Management attributed this loss to exchange rate losses on UNICEM’s sizable dollar loans ($320 million), but reiterated that the associate remained EBITDA positive.

- In all, higher costs pressure and losses from associate drove Q1 15 PBT 32%lower YoY to N8.8 billion, with lesser effective tax rate of 2.8% (vs. 14.5% in Q1: 2014) due to tax write backs—paring declines in PAT (-22% YoY to N8.6 billion). PBT margin shrank 10.6bps YoY to 15.5% while PAT margin expanded 7.3pps YoY to 15% respectively.

Devaluation to stoke earnings pressure

- In its last communication with Analyst, Lafarge’s management stated that repairs at Ashaka cement plant, following insurgency attacks, had been completed, which alongside the concluded recalibration should drive a rebound in capacity utilization to prior levels. Nevertheless, we expect volumes growth in Nigeria to remain subdued largely due to deep cut in government capital expenditure. That said, we expect topline growth to persist as additional hikes in cement prices in March 2015 is set to more than offset the downturn in volumes. At the other end, despite modest rebound in LSAH volumes, consumption of cement in South Africa remains weak, with more domestic players—such as Pretoria Portland Cement (PPC) in search of opportunities elsewhere. This suggests that recovery remains fragile, casting dark cloud over volume growth for the rest of the year. Overall, we expect the price driven growth in Nigeria to outweigh weakness in SA and sustain topline trajectory in the coming quarters. However, impact on bottom-line is likely to be eroded by extension of devaluation-induced cost pressures as well as losses from Unicem, pending restructuring of loans which management aims to achieve post consolidation late 2015. Lafarge trades at 2015 EV/EBITDA of 8.8x relative to 8.9x for Bloomberg EMEA peers. Following a 23% rally since our last update, the company’s stock price is now at a 19% premium to our FVE estimate (N82.47) which is yet to incorporate planned capacity expansion at Ashaka and full integration of Unicem. We have a SELL recommendation on the stock.

- Source: ARM

Disclosure – This article was culled from ARM Research newsletter and was not solely written for Nairametrics. The author of this article wrote it themselves, and did not write this article on behalf of Nairametrics.

{kind=link}