Conoil Plc. (9 months ended September 2014)

- Conoil Plc (“Conoil”) reported that 9M 2014 revenues fell 14.4% YoY to N104.2 billion, with modest decline (3.1% YoY) in operating expenses responsible for 32% YoY drop in both PBT and PAT to N2.1 billion and N1.4 billion respectively.

Revenue plunges on weaker gasoline sales

- In contrast to modest declines recorded thus far in 2014 (Q1: -1% YoY, Q2: -2% YoY), revenues plunged 39% YoY to N25.7 billion (-36% shy of our forecast) on the back of significantly lower throughput volumes in Q3 14. We believe decline was driven by sharp contraction in gasoline volumes (~60% of total) in contrast to flat YoY topline reported by peers Total and Mobil.

- Affirming our view on decline in gasoline volumes, Q3 14 COGS fell a quicker 40.6% YoY to N22.7 billion, with gross profits 24% lower YoY at N2.9 billion. Accordingly, lower contribution from the thinner margin PMS drove a 230bps YoY expansion in gross margins to 11.5% — ahead of the 10.2% implied in our model and 10.7% average over the last 8 quarters.

- Tracking declines in gasoline volumes, operating expenses declined 19% YoY to N1.8 billion reflecting declines in selling and distribution expenses (-36% YoY to N372 million), and administrative expenses (-14% YoY to N1.4 billion). Consequently, operating income fell 26% YoY to N1.2 billion. Nonetheless, largely reflecting net impact of gross margin expansion, EBIT margins expanded 80bps YoY to 4.9%, 50bps above trailing 8-quarter average.

- Conoil’s weak operating performance was compounded by 8% YoY increase to N641 million in finance charges, which tracks a 13% YoY uptick in average borrowings to N13.3 billion. Consequently, PBT fell 44% YoY to N610 million, though normalization of tax rate to 32% (vs. 55.6% in Q3 13), pared the declines in PAT (-15% YoY) to N415 million. PBT margins contracted 20bps YoY to 2.4%, while PAT margins expanded 50bps YoY to 1.6%.

Margin compression on higher PMS volumes and rising interest expense drive subdued earnings outlook

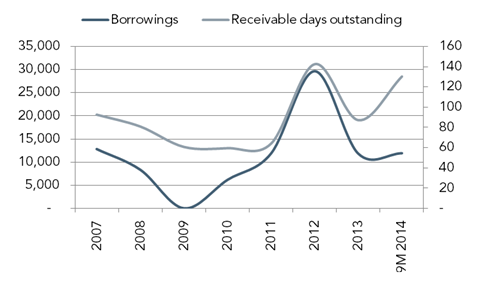

- In all, the Q3 14 results were scarred by lower throughput gasoline volumes which given the breakdown in relationship between receivable days outstanding and debt levels suggest a deliberate attempt by the company to reduce exposure to the subsidy scheme (days outstanding surged to 2012 subsidy saga levels well in excess of 100days). With negative operating cash flows thus far in 2014—vs. positive in each quarter of 2013—we believe Conoil will have to increase borrowing to support gasoline growth in the final quarter of 2014. On this front, lower oil prices, which trims exposure to regulated PMS to~N30/litre from about N50/litre in Q3 14, lowers the risk of subsidy payment delays and as such we see Conoil ramping up borrowing to support volume growth in the near term. Nevertheless, crystallization of the foregoing, in addition to higher finance charge should drive some moderation in margins.

Figure 1: Borrowings (N million) and receivable days outstanding

Source: Company financials, ARM Research

- Conoil trades at a 2014 P/E of 17.1x relative to peer average of 13.5x (Mobil and Total) an unjustified premium in our view of relatively modest earnings growth outlook. Furthermore, while current price of N49.23 implies a 27% correction since our Q2 14 update, it is nonetheless at a significant premium to our fair value estimate of N29.97. Accordingly, we retain our SELL rating on the stock.

{kind=link}