Forte Oil Plc released its 2014 9 Months results to aplomb showing a 33% increase in revenue to N122.5billion compared to N92.1billion in 2012. The company also reported a 175% increase in operational profit to N5.5billion compared to N2billion the year before. Pre-tax profits also increased 61.6% to N5.2billion compared to N3.2billion the year earlier. Profit after tax was N4billion compared to N2.7billion a year earlier. The result from this standpoint looks impressive and the market reacted positively with 4% pop in the company share price, helping it to close at N218. Here are some other good stats worth noting.

Gross Profit Margin – Which shows the company’s ability to be efficient in its top line revenue was 10.8% a 17% increase from the year before.

Operating profit margin – This shows how much profit the company made from its core business without accounting for finance cost and other income that was not earned from the company’s core operations. This is a key metrics for me as it shows how strong a company’s business model is. The company operational profit margin was 4.5% and rose over 106%. Operational profit margin in the downstream sector is typically under 4% with many posting under 2%.

Operational Expenses as a percentage of gross profit – which shows how the company’s expenses as a percentage of Gross profit was 57% compared to 77% in 2012. In absolute terms operating expenses rose 19% to N7.7billion.

These are all key metrics that probably swayed the market to react positively to the results. However, it is important to look at this result from another vantage point.

Earnings Per Share – The company in its result reported an earnings per share of N2.04 a 19% drop from the N2.52 it posted a year earlier. Now this raised a red flag for me considering the huge disparity from the 47% increase in profit after tax it declared. The reason is also highlighted in the result.

Other comprehensive income – The company reported that from its profit after tax it suffered a foreign exchange and actuarial loss of N90million which further reduced the PAT to N3.9billion.

Forte Oil Shareholders – Out of the profits of N3.9billion Forte Oil reported that its shareholders owned N2.1billion compared to N1.79billion for its minority shareholders. This also suggests, out of the profits it declared its shareholders owned about 53% of it.

The reason – Forte Oil is yet to release the notes to its account as at the time of blogging, however its past result shows its Geregu Power plant asset is owned by its subsidiary Amperion Power Distribution Ltd . Forte Oil owns 60% of that company whilst Amperion owns 51% of Geregu Power Plant.

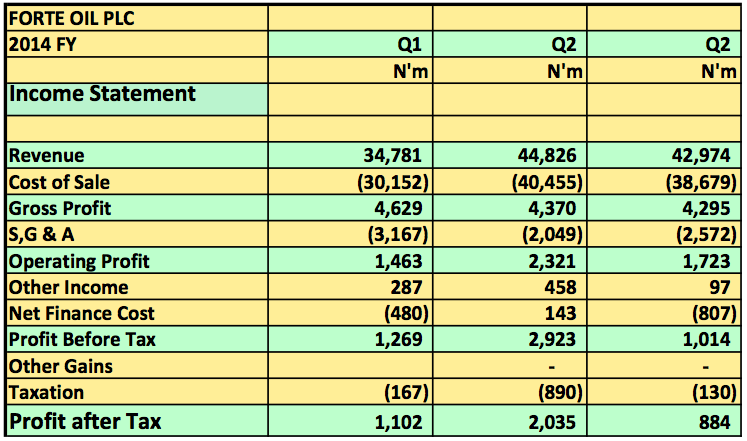

What else? – With a 19% drop in earnings per share, I decided to look closer at this quarter July – September 2014. Pre-tax profits was N1billion compared to N2.9billion in Q2 and N1.26billion in Q1. This suggest a weak Q3 and possibly weaker margins in the downstream sector considering that their Power Unit has posted above 40% margins since they started consolidated the power assets.

Finally – Forte Oil is a fantastically run company and have achieved a remarkable transformation within a short term. The downstream sector is typically a low margin space and Forte Oil has been spending to increase its market share there. Some also suggest their planned acquisition of a downstream asset is in readiness for a ‘planned” deregulation of a downstream sector. I also project the company will need to raise between N20billion to N50billion in the next couple of years if it is to consolidate its leadership in the sector.

Buy, sell or hold? – Current price looks high to me considering their long term earnings potential but the market has placed it as such for Months now.

Verdict: Hold short term, Buy Long term (if you are ready to hold for at least 5 years)

Remember; I do not speculate but rely on fundamentals only.

{kind=link}