Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

Bond Market Opens Bearish as Weakness in Mid-Tenors Persist

Nigeria to Sell Ajaokuta, Others for 2018 Budget

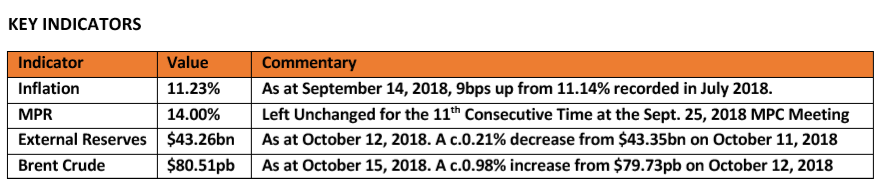

KEY INDICATORS

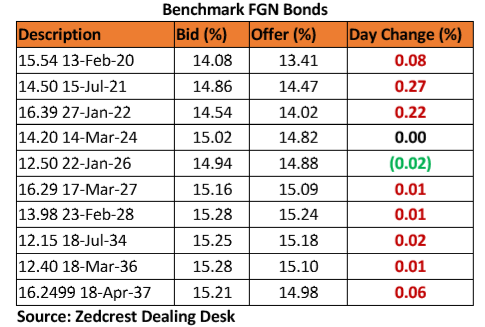

Bonds

The bond market opened the week on a slightly bearish note, following slight sell on the 28s (c.15.28%) and 34s (c.15.23%). Bids were also weaker on the shorter end of the curve (21s and 22s), prompting a c.7bps uptick in yields d/d.

Market players are expected to remain cautious, in wake of the expected uptick in inflation results to be published tomorrow.

Treasury Bills

The T-bills market also traded on a slightly bearish note, with most activities concentrated on the shorter end of the curve (Oct – Feb), where yields inched slightly higher by c.10bps. Across the curve, yields however closed on a relatively flat note, as funding pressures from a wholesale SMIS auction by the CBN kept most market players on the sidelines.

In subsequent sessions, we expect yields to remain slightly elevated, as market players anticipate renewed supply of bills via the forthcoming PMA (Wednesday) and expected OMO auction (Thursday).

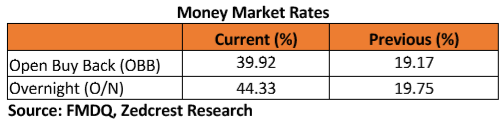

Money Market

In line with our expectations, the OBB and OVN rates spiked by c.20pct to 39.92% and 44.33%, due to funding for the wholesale FX auction by the CBN. System liquidity is consequently estimated to have compressed to c.N30bn from c.N105bn opening the day.

We expect rates to remain elevated, as there are no significant inflows expected until Thursday, where we have c.N347bn in OMO T-bill maturities, and c.N33bn in coupon payments on the April 2037 FGN Bond

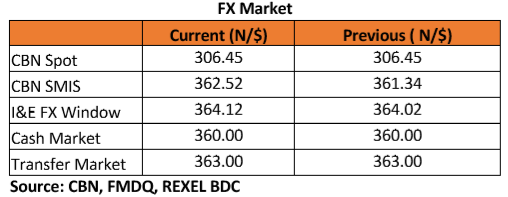

FX Market

At the Interbank, the NGN/USD Spot rate depreciated by 0.02% to N306.50/$ from N306.45/$ previously, while the SMIS rate remained stable at N362.52/$. At the I&E FX window a total of $61.25mn was traded in 211 deals, with rates ranging between N321.00/$ – N365.00/$. The NAFEX closing rate appreciated by c.0.05% to N363.92/$ from N364.12/$ previously.

At the parallel market, the cash and transfer rates remained unchanged at N360.00/$ and N363.00/$ respectively.

Eurobonds

The NGERIA sovereigns continued their mild recovery in today’s session, with yields compressing further by c.6bps on average. The Feb 2038 recorded the highest gains of c.0.50pct on the day.

The NGERIA Corps were mostly quiet, except for mild interests seen on the GRTBNL 18s and DIAMBK 19s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}