Follow Us on Google Discover

Follow Us on Google Discover

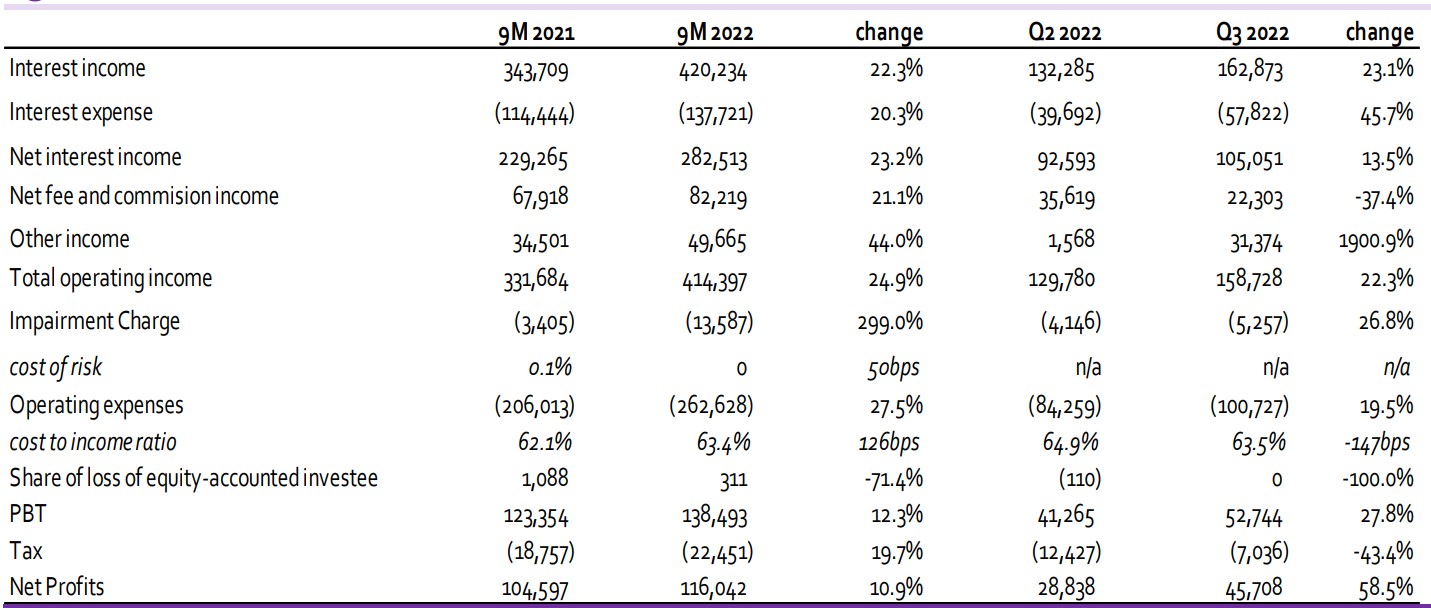

UBA’s 9-month unaudited numbers showed a moderate 22.3% y/y growth in Interest Income to N420.2bn driven mainly by significant growth in Interest Income on loans and investment securities. Net Loans to customers were up 13.8% as of September compared with the December 2021 position. Q/q (Q3 2022 compared with Q2 2022), Interest Income was up 23.1%. Interest Expense on the other hand was up 20.3% y/y but grew strongly in Q3 compared with Q2, up 45.7% q/q.

The y/y growth was on the back of significant growth in Interest Expense on both Customer Deposits and deposits from banks. While Customer Deposits were up 15.5% y/y, Interest Expense on such deposits were up 26.4%y/y, pointing to an increase in funding costs. Deposits were up 10.4% as of September compared with December 2021. Overall, Net Interest Income was up 23.2% y/y to N282.5bn in September 2022 from N229.3bn in September 2021.

Net Fee and Commission Income was up 21.1% y/y to N82.2bn. The y/y growth was driven by growth in trade transaction income (+76.2% y/y) and credit-related fees (+58.2% y/y). E-banking Income, which made up 34.7% of Fees and Commission was up 14.4% y/y to N47.96bn, albeit capped by high e-banking expense of N45.7bn, thus resulting in a balance of only N2.2bn for net e-banking income. Q/q, Net Fee and Commission declined significantly, down 37.4% in Q3 compared with Q2 2022 driven by a significant decline in credit-related fees in Q3 compared with Q2 (down 72.9%q/q). Commission on turnover was also significantly down in Q3 compared with Q2 2022.

UBA 9M 2022 N’m

Other News

Source: Company, CSL Research.

Other Income (Net Trading and Foreign Exchange Income and Other Operating Income) was up 44.0% y/y due to significant growth in Net trading Income on Fixed income securities (up 182.1%y/y) to N23.2bn. The bank also saw growth in foreign exchange trading income (up 14.7% y/y) to N40.8bn. The impact of these was however capped by increased Net Fair value loss on derivatives to N22.6bn in 9M 2022 from 5.3bn in 9M 2021. Q/q, Other Income grew significantly to 31.4bn compared with only N1.6bn in 9M 2021.

Impairment Charge was up 299.0% y/y to N13.6bn in 9M 2022, bringing annualised Cost of Risk (COR) to 0.6% compared with 0.1% for 9M 2021. We expect cost of risk to remain minimal, but we model a marginal increase of 0.7% for FY 2022.

OPEX grew significantly, up 27.5% y/y and 19.5% q/q. The slightly higher y/y increase in Opex compared with a 24.9% growth in Total Operating Income led to a slight deterioration in Cost to Income Ratio (ex-provisions) to 63.4% for 9M 2022 compared with 62.1% for 9M 2021. Major opex growth drivers were a significant growth in employee benefit expenses, which grew to N80.8 billion in 9M 2022 from N66.5 billion in 9M 2021. This, according to the management was due to investment in staff training. Other Operating Expenses also grew significantly (up 32.6%y/y).

Overall, Pre-tax Profit was up 12.3% y/y to N138.5bn while Profit after Tax was up 10.9%y/y to N116.0bn, bringing 9M 2022 annualised ROAE to 19.2% compared with 15.6% for FY 2021. Q/q pre-tax profit was up 27.8% q/q while Net Profits grew 58.5% q/q due to a significantly lower tax charge in Q3 compared to Q2.

With a fair value estimate of N19.40/s, we have a Buy recommendation on the stock. Current Price N7.00/s.