Follow Us on Google Discover

Follow Us on Google Discover

Pension Funds Administrators (PFAs) generally underperformed the inflation rate, MPR, and other major indicators used for determining investment performance.

This is according to information derived from the performance of pension funds during the first 9 months of 2022. PFAs manage pension contributions on behalf of retirement savings account holders (RSA).

The funds are incentivized to deliver superior returns to their RSA account holders depending on their risk appetite. Thus, the better the performance of a PFA in a Fund type compared to a competing PFA, there is more chance that they attract more RSA holders.

From our analysis, nearly all PFAs across all fund categories reported returns on investments that are 10% or below. The only fund that returned above 10% was the NLPC PFA Fund VI (A) which returned 15.38%. All others were either bother line of 10% or below, falling way below the average inflation rate of 17.43% in September.

Other News

Nairametrics in partnership with Money Counsellors presents an analysis of the performance of Pension Fund Administrators for the first 9 months of 2022.

Fund I

Fund I is accessible strictly by formal request of the contributor and only for those aged 49 years and below.

As of 30 September 2022 the Stanbic IBTC Pensions Fund I was the best year-to-date performer in this fund category, returning 10.33% YTD followed by First Guarantee Pension (9.16%) and ARM Pensions (7.90%).

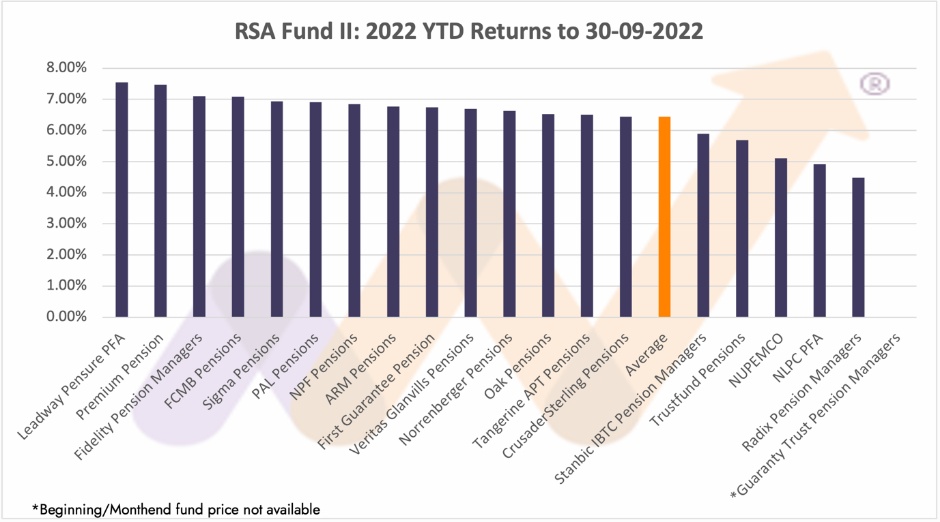

Fund II

Fund II is the default fund for all active contributors that are 49 years and below.

The best-performing RSA Fund II as of 30 September 2022 was the Leadway Pensure PFA Fund II (7.54%), followed by Premium Pension Fund II (7.47%) and Fidelity Pension Managers Fund II (7.10%).

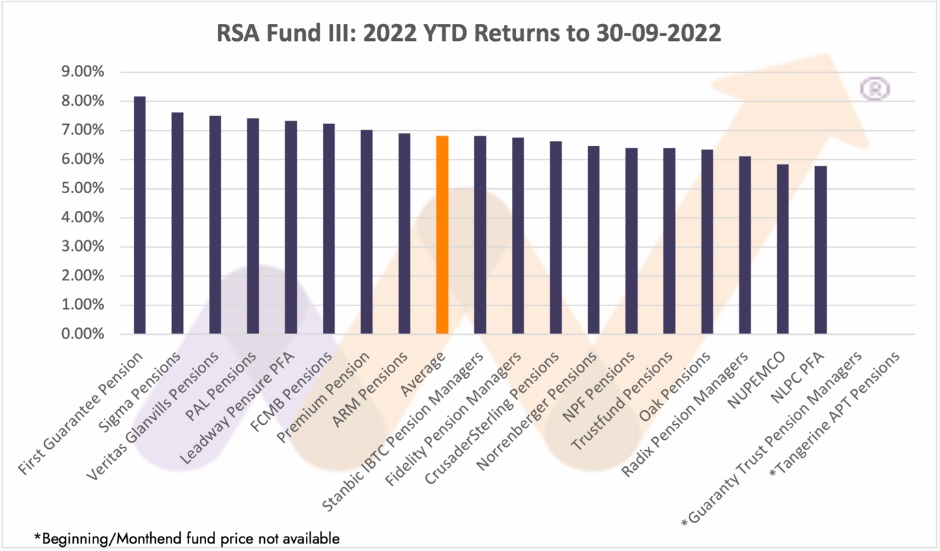

Fund III

Fund III is the default fund for active contributors that are 50 years and above.

The best-performing RSA Fund III as of 30 September 2022 was the First Guarantee Pension Fund III (8.18%), followed by the Sigma Pension Fund III (7.62%) and the Veritas Glanvills Pensions Fund III (7.50%).

Fund IV

Fund IV is strictly for retirees only.

The best-performing RSA Fund IV as of 30 September 2022 was the First Guarantee Pension Fund VI (8.43%), followed by the Leadway Pensure PFA Fund VI (8.38%) and the PAL Pensions Fund IV (7.98%).

Fund V

Fund V is only for Micro Pension Fund contributors.

Whilst, not all PFA’s offer the Fund V, the performance of those that do and publish prices and other information on their website show that the best performing RSA Fund V as of 30 September 2022 was the Veritas Glanvills Pensions Fund V (9.98%), followed by the Stanbic IBTC Pension Managers Fund V (8.38%) and the NLPC PFA Fund V (7.66%).

Fund VI (Active)

Fund VI (Active) is for those that choose to have their contributions invested in Non-interest Money and Capital Market Products.

For the few that offer and publish information on the RSA Fund VI (Active), the best performing RSA Fund VI (A) as of 30 September 2022 was the NLPC PFA Fund VI (A) (15.38%) followed by ARM Pensions (7.13%) and Premium Pension (6.92%).

Fund VI (Retiree)

Fund VI (Retiree) is for those that choose to have their contributions invested in Non-interest Money and Capital Market Products.

For the few that offer and publish information on the RSA Fund VI (Retiree), the best performing RSA Fund VI (R) as of 30 September 2022 was the Premium Pension Fund VI (R) (7.56%), followed by Sigma Pensions Fund VI (R) (7.29%) and Veritas Glanvills Pensions Fund VI (R) (6.99%).

Returns of All Funds Since Inception of each fund to 30 September 2022 (Unaudited)

The table below has been compiled using the daily prices as displayed on each respective PFA’s website. However, they are unaudited. To see your fund’s audited returns from inception to 31 December 2021, go to the Literature and Download section of your fund on moneycounsellors.com and download the report.

Conclusion

Whilst we have shown the average performance of funds in each fund class, using averages to visualise the performance of a fund compared to others does no one any good other than visual optics and we are hopeful that pension funds will soon have benchmarks to that one can measure and compare performance.

In the meantime, here are some metrics one can measure the funds against:

Metrics as of 30 September 2022

- NGX All-Share Index 14.77%

- NGX 30 Index 1.43%

- NGX Pension Index 2.17%

Yield on

- 3-Year FGN Bond (Jan 2026) 13.25%

- 5-Year FGN Bond (Feb 2028) 13.25%

- 10-Year FGN Bond (Jul 2034) 13.25%

- Inflation 20.52%

- MPR 15.50%

While the majority of the PFAs abide by the guidelines in publishing information on their website and promptly too, a few are late in doing so while some others do not bother publishing information at all.

- Providing information in the forms of factsheets, newsletters, asset allocation, NAV in audited accounts, etc., helps investors to review and make informed decisions about their pension fund.

- Also, providing regular and timely information helps existing customers and potential ones to understand a firm and its investment strategy in managing pension funds. Things can only get better.

What you should know

Please note that the figures presented below are unaudited. For audited figures, please refer to each fund and PFA report available in the Literature & Downloads section of each PFA on the moneycounsellors.com website.

- One of the guidelines by PenCom said that “in keeping with the spirit of transparency and to ensure that all stakeholders, particularly RSA holders, have access to vital basic information”, there is a minimum amount of information that PFA’s must post on their websites.

- This includes Daily Unit Prices for funds (for the last 7 days); structure of investment portfolio for the funds for the last 7 days; periodic newsletter on the activities of the PFA and the pension industry; latest approved audited accounts of the company and the funds.

- Also, the guideline on rates of returns on RSA funds mandates PFA’s to disclose “…the net assets value per unit of the fund” in financial statements. With all this in mind, we are reliant that all information on each respective PFA’s website is published under current guidelines, circulars, rules and regulations as issued by PenCom. It is also international best practice to do so.

You may download a report on the performance of your pension fund and your PFA by visiting the literature & Download section of your fund at moneycounsellors.com.

In partnership with © MoneyCounsellors.com