Follow Us on Google Discover

Follow Us on Google Discover

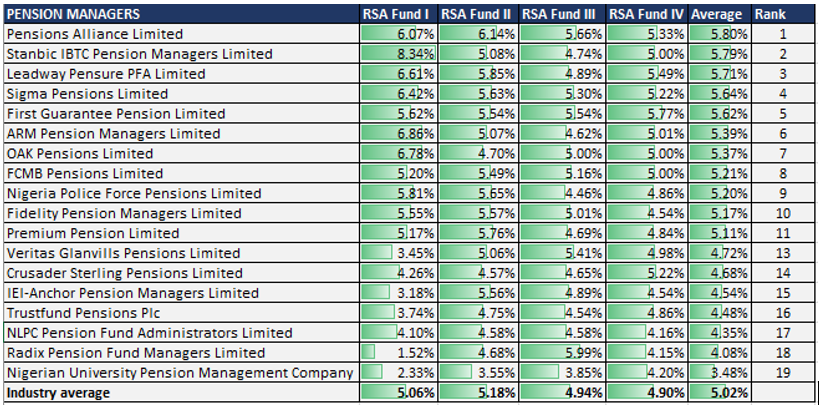

The Nigerian pension industry recorded an average return of 5.02% in the first half of 2022, as all the pension fund administrators printed positive returns in the period. The pension industry has grown highly competitive in the last two years following the opening of the transfer window, which allows contributors to switch PFAs.

According to data from the National Pension Commission (PENCOM), 12,336 contributors changed their pension administrators in Q1 2022, bringing the total transfers to 63,728 since Q4 2020. Although the industry has grown more competitive, the aggregate returns is still very much below the country’s inflation rate at 18.6%.

This is not surprising, considering the conservative nature of PFA investment. Looking at the latest report from the PENCOM, 62.1% of the total industry asset under management is invested in federal government securities, which are safe haven assets albeit with low-interest rates, hence, the low returns being printed by the pension managers.

Meanwhile, the industry regulatory body, PENCOM announced in April 2022 that all PFAs had complied with the Commission’s directive for the increase of the Minimum Regulatory Capital from N1 billion to N5 billion. The exercise, however, resulted in the merger of some of the administrators, reducing their number from 22 to 20.

Also Read

Notably, PENCOM approved the acquisition of AIICO Pension Managers Limited by FCMB Pensions Limited; and the merger between Tangerine Pensions Limited and APT Pension Funds Managers Limited and subsequent change of name of the merged entity to Tangerine APT Pensions Limited.

In the same vein, the Commission also approved the acquisition of IEI-Anchor Pension Managers Limited by Norrenberger, after the latter acquired the majority shareholder of the company, IEI Plc.

In line with Nairametrics’ regular ranking of various sectors in the Nigerian economy, here is a compilation of the best performing Pension Fund Administrators (PFA) in the first half of 2022. It is worth noting that, Tangerine Apt Pensions was not included in this ranking because of the two different entities coming together, each with their fund prices as of December 31st 2021.

RSA Fund I

The RSA Fund I is the riskiest of the funds under consideration. The fund is designed for active contributors who are 49 years of age and below, majorly for the sake of maximizing the returns on investment through diversifying 20% to 75% of the funds in income instruments.

Although contributors can shift from this fund to fund II or III once they attain 50 years of age. The fund category recorded an average return of 5.06% in the first half of the year.

Third Position: Oak Pensions

Half-year return – 6.78%

Second Position: ARM Pension Managers

Half-year return – 6.86%

First Position: Stanbic IBTC Pension Managers

Half-year return – 8.34%

RSA Fund II

The RSA Fund II is the default fund for contributors who are 49 years and below, although they are at liberty to shift to Fund I based on their risk appetite. It is worth noting that fund II with N6.21 trillion contributors fund accounted for the largest share of the total net assets in the pension industry as of September 2021.

The RSA Fund II was the best performing fund category in the period under review with an ROI of 5.18% between January and June 2022.

Third Position: Premium Pension

Half-year return – 5.76%

Second Position: Leadway Pensure PFA

Half-year return – 5.85%

First Position: Pensions Alliance Limited

Half-year return – 6.14%

RSA Fund III

The RSA Fund III is a conservative fund with only about 5% to 20% invested in variable income instruments. It is a fund for contributors who are 50 years and above. Although the contributors can shift to Fund II, upon request.

They recorded an average 4.94% returns on investment in the period under review.

Third Position: First Guarantee Pension

Half-year return – 5.54%

Second Position: Pensions Alliance Limited

Half-year return – 5.66%

First Position: Radix Pension Fund Managers

Half-year return – 5.99%

RSA Fund IV

This fund category is only open to retirees and investment conservatives. Contributors in this fund cannot move from this fund to any other fund. About 10% of the fund can be invested in variable income instruments. The fund recorded a 4.2% return on investment in the first six months of the year.

Third Position: Pensions Alliance Limited

Half-year return – 5.33%

Second Position: Leadway Pensure PFA

Half-year return – 5.49%

First Position: First Guarantee Pension

Half-year return – 5.77%

How we determine top performers

- The percentage difference between the bid price on 31st December 2021 and 30th June 2022 was computed to obtain the annual rate of returns for the PFAs.

- This is done across all fund categories where prices are published.

- The overall performance was obtained by averaging the ROI of the PFAs across the four fund categories.

- Bid prices and other associated data are obtained from the websites of all Pension Funds, provided that they are published on their website on the day it was captured. Nairametrics Research also reached out to some of the PFAs in situations where the data could not be found on their website.

- For this ranking, Nairametrics captured 19 listed Pension Fund Administrators with the PENCOM.

Pencom should please come to the rescue of pensionieers who retired under contributry pension scheem. What formular do you use in calculatig monthly pension? Pensionieer with over one point three million naira contributed earmning ten thousand naira a month is rediclous in this hyper inflation in the country. You are growing while people who contributed the money are starving. It is very unfair.

I am 35 years old, the grammars here are too mush for me to understand. Pls in a simple English, which PFA do you advise I use, this is very important for me. Kindly help.

I’m using NLPC. they r accessible

From the report above, it’s obvious Stanbic IBTC pension stood out.

Secondly, your level of risk appetite should determine your choice from the above reports.

I for instance, I hold account with Stanbic IBTC presently structure on fund II. Am planning to move my portfolio to fund I for better return on investment ROI.

I use Stanbic IBTC pensions. They are like the most reliable PFA we have presently.

I’m currently having my RSA with NLPCPFA… I want to port to StanbicIBTC pension administrator ASAP. NLPCPFA is hell abeg