Follow Us on Google Discover

Follow Us on Google Discover

OMICRON VARIANT OF COVID-19 RATTLES GLOBAL MARKET

Just as the world subtly basked in the euphoria of the waning of uncertainties around the delta variant of the Covid-19 virus, we have suddenly been confronted with the omicron variant of the deadly virus that has now been reported in at least 23 countries including the U.S., South Africa and Nigeria. At the tail end of November, the World Health Organization (WHO) designated Omicron (variant B.1.1.529) a variant of concern, on the advice of WHO’s Technical Advisory Group on Virus Evolution (TAG-VE). The decision was based on the evidence presented to the TAG-VE that Omicron has several mutations that may have an impact on how it behaves, for

example, on how easily it spreads or the severity of illness it causes. Policy makers and markets around the world continue to oscillate as the world race to ascertain the extent to which the virus can compromise progress recorded so far in the battle against Covid-19.

Elsewhere, the appointment of Jerome Powell as the Federal Reserve Chairman for another four-year term beginning February 2022 ended weeks of speculation over U.S. apex bank’s policy trajectory. Whilst the appointment of Powell has essentially entrenched an era of a Hawkish Fed who just recently changed its erstwhile position that inflationary pressures were transitory, the appointment of his closest contender, Lael Brainard (who has now been promoted to vice chairman) would have seen the emergence of a U.S. Fed that is more dovish in its policy posture. Consequently, the Feds have commenced tapering its asset-purchase program starting with $15 billion, split across $10 billion treasury purchases and $5 billion mortgage-backed securities. Although the Fed has noted plans to close out the asset purchase program by midyear 2022, there are credible talks around closing out the pandemic support program even faster, as inflation which hit 6.8% (year on year) in December remains

a major cause for concern. However, we are cognizance of how much unfolding insights into Omicron can influence decisions going forward.

On the local front, the fuss on whether or not to withdraw subsidy payments on petroleum motor spirit (PMS) remains present. The Federal Government of Nigeria currently expends roughly ₦250 billion monthly on subsidizing PMS consumption in the country, a numbers that keeps increasing. However, due to slackly constituted structure of institutions, the masses do not get the full benefit of this humongous monthly expenditure. With the World Bank and indeed the international financing community almost daily sounding the gong in support of subsidy removal to the Nigeria authorities, it remains unclear if the government will muster the courage and political will to finally end the perceived treacherous era of subsidy payment and allow a sternly market driven industry, geared at creating value for the Nigerian people.

THE MACROECONOMY

GDP Growth & Oil Production

Other News

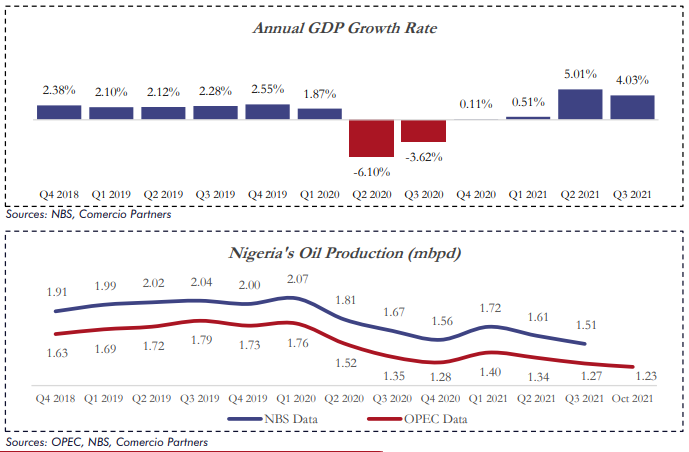

Nigeria sustained the growth trajectory seen in the last three quarters, as the economy recorded a real growth rate of 4.03% y/y in Q3 2021. The Q3 2021 growth rate represents a decline of 0.98% when compared to the preceding quarter (5.01%), but reflects a sharp uptick of 7.65% relative to the growth rate recorded in

Q3 2020 which stood at -3.62%.

The oil sector sustained its downtrend, as it recorded a real growth rate of -10.73% y/y in the third quarter of 2021. The oil sector marked its sixth consecutive period of contraction, despite the sustained bullish trend in the international oil market. Oil sector performance was dampened by the local production level, as it declined in the

review period. Local oil production stood at 1.57mbpd, reflecting a decline of 0.10mbpd when compared to the production level in Q3 2020 (1.67mbpd). Elsewhere, the non-oil sector recorded a real growth rate of 5.44% y/y in the review period, up by 7.95% and down by 1.30% relative to the rates recorded in Q3 2020 (- 2.51%) and Q2 2021 (6.74%), respectively.

Of the three major activity sectors, service retained the largest quotient in terms of GDP contribution, at 49.65%. Hence, agriculture and industries contributed 29.94% and 20.41%, respectively, to the GDP in Q3 2021. This explains the improvement seen in real GDP growth, as the service sector, which accounts for the lion’s share of the GDP, grew by 8.41% in the review period. Agriculture also grew by 1.22%, while industries remained in the contractionary region at -1.63%.

In other news, OPEC, in its monthly oil market report for November revealed that Nigeria’s oil production dipped on a monthly basis by 1.52% to 1.23mbpd in October 2021, as structural problems in the sector continues to weigh on output. This decline was recorded despite the 400,000bpd monthly output increase by OPEC+. In addition, OPEC estimated a demand growth of 5.7mbpd for 2021, 0.16mbpd lower than the preceding month’s estimate, putting the total demand for the year at 96.4mbpd. On the supply side, OPEC forecast a non-member supply growth of 0.7mbpd to average 63.6mbpd, leaving their projection unchanged from the preceding month’s estimate.

Inflation

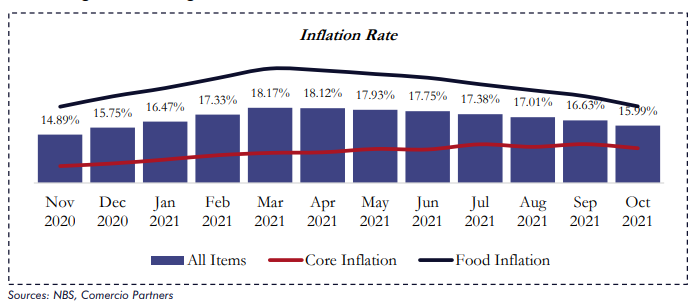

Inflation sustained its path of moderation in October 2021. The headline index grew by 15.99% YoY in October 2021, 0.64% lower than 16.63% recorded in September 2021. Likewise, the food and core inflation metrics respectively inched up by 18.34% and 13.24% YoY in October 2021, 1.23% and 0.50% lower than 19.57% and 13.74% recorded in September 2021. The drop in yearly headline inflation marks the seventh consecutive decline, following a 19-month uptrend that lasted from September 2019 till March 2021. The moderation in the headline index was largely driven by the sustained decline in the food subindex, as well as the reversal of the

core segment uptrend.

In October 2021, headline inflation rose by 0.98% MoM, representing a 0.17% decline from the rate of 1.15% that was recorded in the previous month. The yearly average rate rose to 16.96%, 0.13% greater than 16.83% recorded in the previous month. The decelerated rate of increase in the monthly headline rate of inflation benefited from a moderation in both food and core subindexes.

The food subindex rose by 0.91% MoM, reflecting a 0.35% decrease from the rate of 1.26% recorded in September 2021. The yearly average rate rose to 20.75%, 0.04% higher than 20.71% recorded in the preceding month. The food subindex reversed its monthly uptrend, benefitting from the gradual debottlenecking of supply chains and the year-end harvest impact.

Core inflation stood at 0.80% MoM, down 0.44% from 1.24% recorded in September 2021. The yearly average rate also rose to 12.73% last month, 0.18% higher than 12.55% recorded in the preceding month. The highest increases were recorded in prices of gas, fuels and lubricants for personal transport equipment, vehicle spare parts, non-durable household goods, solid fuel, passenger transport by road, passenger transport by air, garments, cleaning, repair and hire of clothing, major household appliances (whether electric or not), wine, clothing materials, other articles of clothing and clothing accessories.

Yearly headline, food and core inflation rates rose at a slower pace in the review month, as the impact of a more pronounced base effect held sway. Both headline and food yearly index changes are now at their lowest level in the year. Likewise, we recorded a moderation in the monthly inflation rate for all three indexes, with the food subindex drawing support from the main harvest season in both the northern and southern regions. Despite the improvement seen in both monthly and yearly rates, several inflationary drivers still remain active. The upsurge in the price of cooking gas and diesel stayed unassuaged in the review month, as the global energy crunch remained untamed.

Elsewhere, FX shortages continue to mount pressure on imported items, with the NAFEX rate depreciating by 0.57% month-on-month and 7.57% year-on-year to average ₦415.10/US$ in October.

Capital Importation and Foreign Exchange Reserves

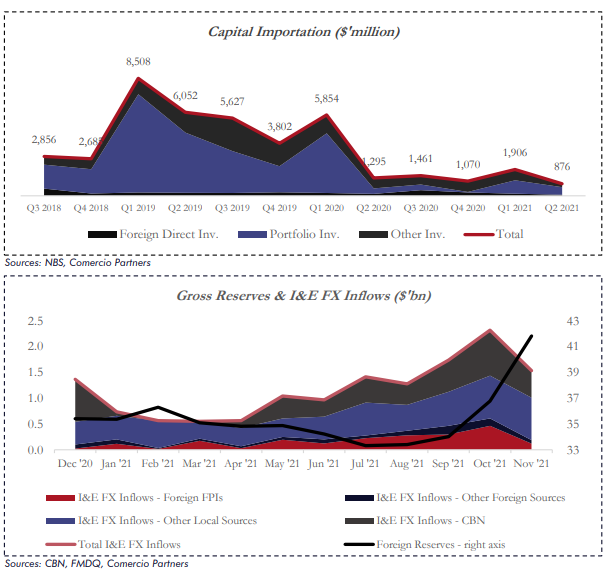

Nigeria’s foreign reserves remained elevated, hovering above the $40 billion benchmark, as it printed at $41.2 billion in November 2021, down marginally by 1.5% from $41.8 billion recorded in the previous month.

The total value of capital importation into the Nigerian economy through the I&E FX Window for the month of November dipped by 33.9%, standing at $1.5 billion compared to $2.3 billion recorded in the previous month of October. The decline in total inflow was chaired by a 73.9% and 53.2% decline in inflows for FPIs and other foreign sources which printed at $121 million and $67.5 million respectively in the month under review. Similarly, the 40.8% and 0.9% decreases seen in FX inflow through the CBN and other local sources weighed down the value of capital flows into the country, printing at $521.8 million and $823.7 million respectively.

Overall FX outflow through the I&E FX Window for the month of November decreased by 41% to reach $1.4 billion when compared to the previous month of October when $2.3 billion was recorded. FX outflows through FPIs dropped by 65% to print at $236.9 million, other foreign sources dropped by 48.8% when compared to the previous month, to print at $42 million; while outflow through other local sources equally declined by 30.1%, reaching $1.1 billion in the month under review.

Accordingly, I&E FX Netflow for the month of November 2021 stood at $164 million, a significant increase when compared to the previous month of October when a negative netflow of $3.6 million was recorded. The FX netflow posted in the month of October stands as the first negative netflow since the Month of June 2021.

FINANCIAL MARKETS

Fixed Income Market

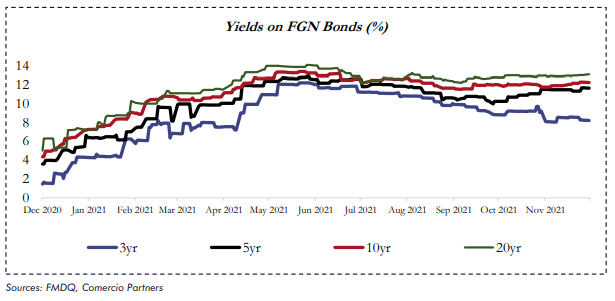

Activity in the fixed income market sustained its relatively mixed sentiment in November 2021 as market participant moved from the mid to long end of the curve, to shorter dated instruments given the unclear market direction. Monthly yields for the benchmark securities monitored declined on the short end of the curve while mid to long end maturities inched up on a month-on-month basis. Average yields on the sovereign bonds with 3-year declined by 85 bps, whilst 5-year, 10-year and 20-year maturities rose by 66 bps, 3 bps, and 2 bps, respectively.

At the Bond auction held on 17th September 2021, the DMO offered ₦150.00 billion worth of FGN FEB 2026, FGN MAR 2037 and FGN MAR 2050, with stop rates printing at 11.65%, 12.95% and 13.30%, respectively. The subscription stood at N267.15 billion, while ₦225.25 billion was allotted. The auction had a bid to offer ratio of 1.78x.

With inflation sticking to its course of moderation in October 2021, alongside a fourth consecutive quarter of positive real GDP growth in the third quarter of the year, the MPC found some comfort in existing policy decisions; hence, allowing them the leeway to retain their policy stance and adopt a wait-and-see approach to allow for a clearer view of global developments. Accordingly, at the end of the 23rd November MPC meeting, all policy levers were maintained, following a unanimous vote by all members of the committee.

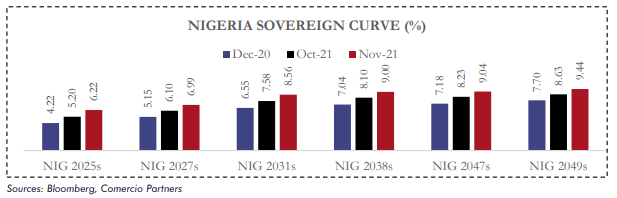

Eurobond Market

We witnessed a further weakness in the Eurobond space in the Month of November as the intensifying inflationary concerns coupled with tapering continues to drive a bearish bias in the Eurobond market. Average yield on the selected benchmarks monitored rose by 90 bps month on month in November 2021. Inflation accelerated at its fastest pace since 1982 in November, putting pressure on the economic recovery and raising the stake for the Federal Reserve. The consumer price index, which measures the cost of a wide-ranging basket of goods and services, rose 0.8% for the month, good for a 6.8% pace on a year over year basis and the fastest rate since June 1982.

Foreign Exchange Market

Foreign Exchange Market

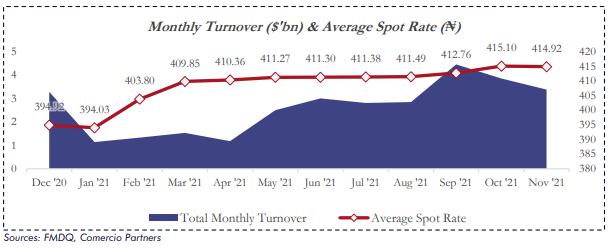

The average monthly value of the Naira appreciated by ₦0.18 at the I&E FX Window with the average exchange rate of the currency to a unit of the Dollar dropping to ₦414.92 in November 2021 from ₦415.10 in October 2021. Total monthly turnover traded on the I&E FX Window was down by 12.3% to $3.39 billion in November

2021 from $3.86 billion in October 2021.

According to data obtained from the CBN official website, Nigeria’s foreign reserve dipped by 1.47% during the month of November to close at $41.22 billion compared to $41.83 billion recorded in the month of October. The recent decline in the nation’s external reserve can be attributed to the intervention by the apex bank in the official forex market to stabilise the Local Currency. Nigeria’s reserve level had gained massively in the month of October, receiving an additional $5.99 billion, through proceeds from the $4 billion Eurobond issued by the federal government in September and a $3.35 billion SDR allocation from the International Monetary Fund (IMF), which saw the nation’s reserves surpass the $40 billion threshold.

Equities Market

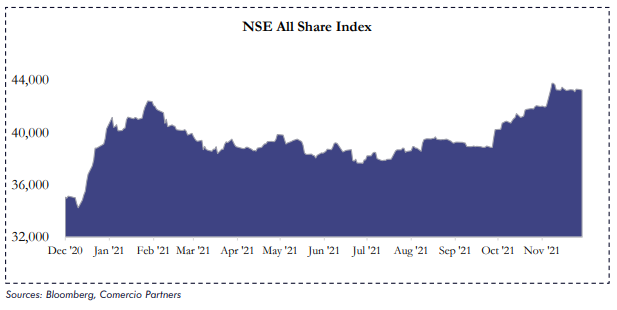

The profit-taking that ensued in November was highly inevitable given the local bourse’s spectacular performance in prior month. The month of October saw the exchange record a month-on-month gain of 4.52%, its best performance in nine months. In November, market sentiments were in line with the Q3’ 2021 performance of the listed firms as profit taking was prevalent for tickers whose results had already been priced in while sell pressure intensified for tickers that released subpar results. During the month, sentiments hovered between positive and negative following the announcement of some corporate disclosures. Speculators and retail

investors were the force behind market activities as institutions remained on the sidelines. The MPC meeting outcome coupled with the consistent rate decline for the 1-year bill had little to no impact on activities in the local bourse.

MTNN came out early in the month to announce that its major shareholder would sell up to 575mn units of the company shares to institutional and retail investors in November. The offer was executed via a book build to institutional investors, while retail investors were allotted shares at a fixed price. The units offered represent 3.72% of MTN’s c.76% stake in MTNN NL. Coincidentally news was released about MTNN NL & AIRTEL being granted an approval in principle by the CBN to operate a Payment Service Bank. For MTNN NL, this news bodes well for its public offer as it bolstered offshore and local interests in the stock.

The NGX released the NGX Domestic and Foreign Portfolio Investment Report for October 2021. Foreign participation improved to c.₦42bn from c.₦24bn in the previous month. Domestic participation was up to c.₦171bn from c.₦94bn. Domestic participation maintained the higher share of total flows at 80%.

The sectoral indices performance for the month was minimal as only two sectors posted gains. The Insurance sector and Industrial sector both gained 4.28% and 0.72% month-on month, respectively, while the Consumer goods, Banking and Oil & Gas followed, shedding 3.92%, 4.78% and 7.56%, month-on-month, respectively.

Despite the strong sell pressure seen in the month of November, the benchmark ASI index settled at 43,248.05 points, with a month-on-month gain of 2.88%. Year-todate returns remained positive at 7.39% gain.

'/%3E%3C/svg%3E) OUR EXPECTATIONS FOR THE COMING MONTHS

OUR EXPECTATIONS FOR THE COMING MONTHS

Non-oil sector growth, which is the sponsor of the overall economic uptick, remains driven by the rebound in activity level across various sectors relative to the base year where Covid-19 restrictions brought the economy to a standstill. Hence, the trend of growth is expected to decelerate in coming quarters, as the impact of the low base wanes. Elsewhere, the oil sector downtrend has more to do with structural issues in the industry, leaving neither OPEC+ output restrictions nor oil prices as the culprit behind the sustained downtrend in the sector. However, we expect the implementation of the Petroleum Industry Act (PIA) to catalyze renewed interest in capital investments, particularly in the upstream sector of the Nigerian oil industry. In the interim, oil prices have risen significantly over the last year, while Nigeria has failed to meet the output quota allotted by OPEC amidst the gradual increase in supply from the bloc. Hence, the sustained uptick in crude prices should help cushion the oil sector contraction, as Brent crude hovered close to its 3-year high at $75.07/bl at print time. Looking further into the coming year, we expect the economy to return to its tepid growth trend, with real growth rate staying subdued below 3.00% in 2022.

The trend of increase in yearly inflation is expected to moderate further in the coming month, as the impact of the high base effect becomes even more material. Nonetheless, the characteristic year-end spending around the festive season could override the impact of the main harvest season and the interim currency strengthening; hence, pressuring monthly inflation northwards. Also, energy prices continue to remain a major concern, as OPEC’s deviant stance to improve supply, amidst an anticipated increase in demand during the winter, could further worsen gas and diesel prices. On the monetary front, the MPC should find some comfort in the

sustained moderation in inflation, making economic growth the policy priority in the near term.

In the local bond market, we expect sentiment to remain mixed, with the short end of the FGN bond curve seeing most of the traction. However, in the Eurobond market, we expect the bearish sentiment to persist in coming months, as the spike in U.S inflation might accelerate the pace of asset purchase tapering by the Feds.

In the FX market, we expect the Apex bank to continue leveraging the relatively elevated foreign reserve level to provide support to the Naira by boosting FX supply.

On equities, the last month of the year will be strategic for market players that seek to position themselves ahead of full-year earnings releases and dividend announcements in the new year. Asides from the aforementioned strategic play, we should continue to see corporate disclosure drive most of the activity in the local bourse, whilst fundamental market anchors are disregarded.