Follow Us on Google Discover

Follow Us on Google Discover

Nigeria’s Eurobond yields spiked to as high at 12% last week as investors fled emerging market securities in the wake of Covid-19 pandemic and the crash in oil prices.

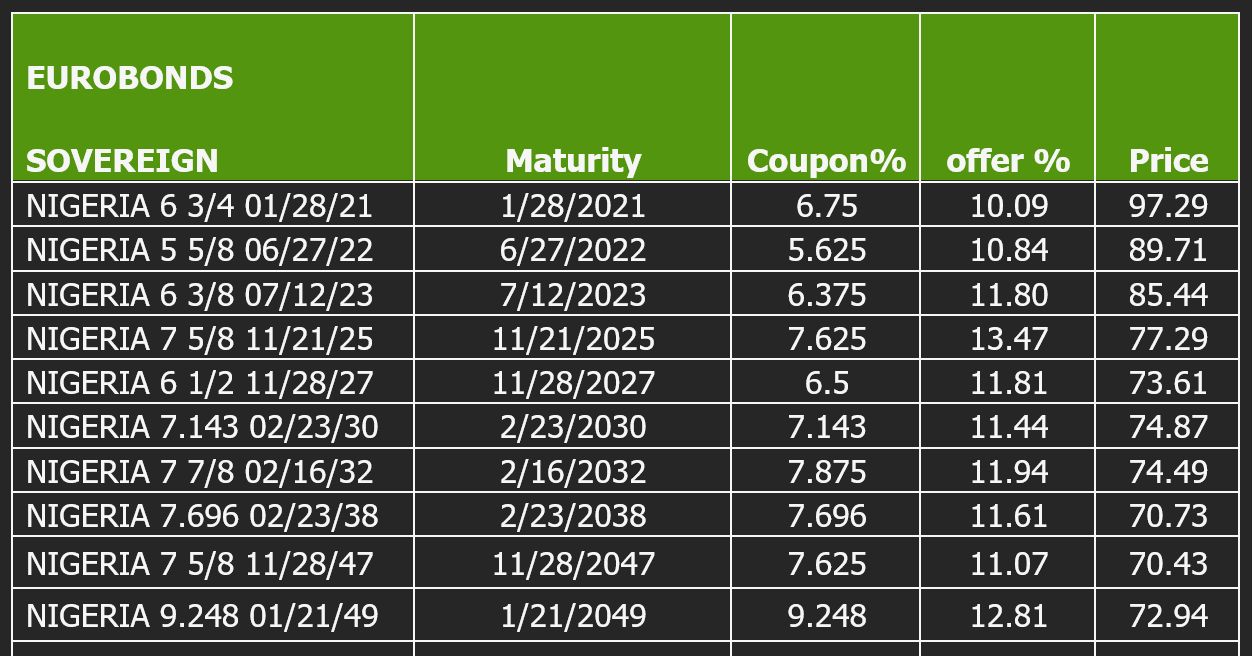

Higher bond yields: Nigeria’s 2049 Eurobond Yields traded at a yield of 12.81% as prices fell to $72.94. The coupon rate for this loan about 9.2%. The shorter ended 2021, 28th January bond yields sold for $97.29 with a yield of 10.09%. Bond yields are inversely correlated to their underlying prices. The lower the price of a bond the higher the yields. A falling bond price is often associated with higher risk consideration.

Country Risk: As Oil prices continue to fall, foreign portfolio investors are worried about the government’s ability to meet its credit obligations without seeking refinancing of the bonds. Nigeria currently has over $29 billion in external loans with the Eurobond component stated at $10.8 billion as of September 2019. The country’s revenue situation could affect its ability to repay its bond obligation forcing a sell-off and increasing bond yields.

Downgrades: Earlier in the month, one of the global rating firms, Fitch downgraded Nigeria’s credit ratings. This rating agency explained the downgrade was mostly due to the decrease in the country’s external reserve from $45.1 billion as of June 30, 2019, to about $38 billion as of January 31, 2020. The decline in the external reserve has persisted as it now $36.18 billion. It is also expected to fall further with the crash in oil prices below $30 per barrel.

Other News

In December 2019, Fitch Ratings revised the outlook on Nigeria’s long term foreign-currency issuer default rating (IDR) to ‘Negative’ from ‘Stable’, but affirmed the country’s sovereign credit rating at B+. However, Fitch’s Middle East and Africa sovereign analyst, Jan Friederich, hinted that the B+ rating could be revised downwards to negative.

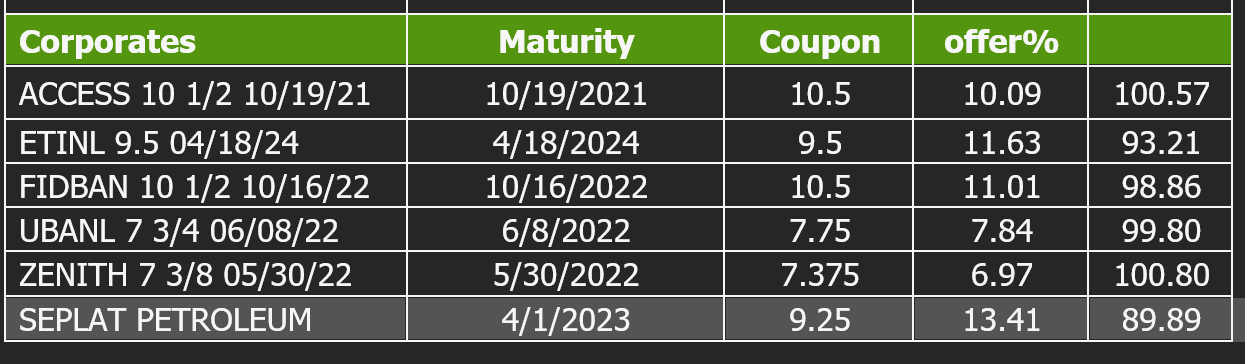

Eurobond Yields vs FGN Bonds Vs Corporate Bonds: Analysts also noted that Nigeria’s Eurobonds now traded at almost the same yields as FGN Bonds while some Corporate Bonds yields even had lower yields than Eurobonds.

This is somewhat of an anomaly as investors often price local bond securities at a higher yield when compared to foreign currency denominated bonds. This perhaps shows just how spooked foreign portfolio investors are about Nigeria’s revenue situation.

Buying Opportunity? The latest devaluation of the naira may have also presented a buying opportunity for Nigerian Eurobonds. With yields as high as 12%, investors will be in line for significant upside if prices rally later in the year. While the risks still remain high, a bond rally could ensue once the Covid-19 virus is contained and oil prices stabilize. This is not taking into consideration another possible round of devaluation later in the year.

Many thanks for the insights.

Is it advisable to hold on to Eurobond investments in the hope that there will be a turnaround? Or should one just cut their losses and liquidate instead?