Follow Us on Google Discover

Follow Us on Google Discover

The latest data released by the Nigerian Communications Commission (NCC) revealed that the leading service provider of the industry, MTN Nigeria, lost 178,103 internet subscribers last month.

According to the data, MTN’s total internet subscribers stood at 52.4 million in May this year, while the number dropped to 52.2 million in June. It should, however, be noted that this is the first time MTN Nigeria would lose internet subscribers in about a year.

Industry Statistics: The breakdown of the data showed that the total internet subscribers in Nigeria also dropped for the first time in one year. The total internet subscribers dropped to 122.2 million from 122.6 million subscribers in May. Hence, in just one month, internet subscribers declined by over 332,000.

It is important to note that the last time internet subscribers suffered setback was in June 2018, when the total internet subscribers dropped by over 347,000 in one month.

Also Read

9mobile’s continuous free-fall: The data also revealed that the number of 9mobile’s active internet subscribers has continued to fall for over two years. In t June 2019, 9mobile suffered a dip as its internet subscribers declined to 9.03 million as against 9.35 million recorded in May 2019. Meanwhile, the company’s market share in the entire industry remains 9% of the market or 15.96 million subscribers.

[READ ALSO: worrisome trend as 9mobile loses over 3 million subscribers in 2 years]

- Meanwhile, Globacom recorded the highest number of subscribers in June 2019 with a 196 ,000 increase in internet subscribers.

- On the other hand, Airtel saw an addition of 42 ,000 to its total internet subscribers in June.

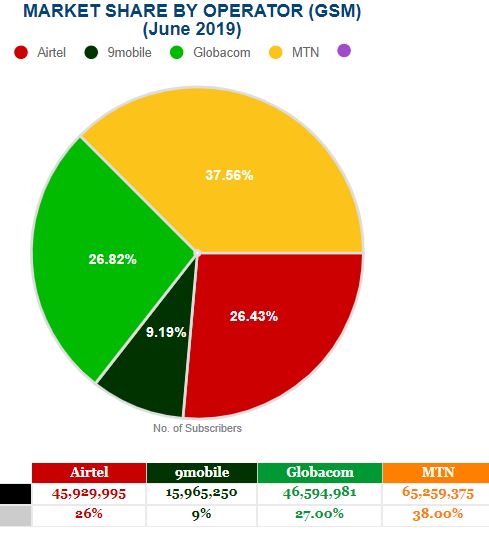

However, on the market share, MTN maintains the lead with the largest market share of 65.25 million subscribers (38% of the total market).

- The indigenous-owned Globacom is the second-largest telecommunication firm in Nigeria, as it overtook Airtel with a 27% share or 46.59 million subscribers to its services.

- Airtel, whose shares were recently floated on the local and international exchange markets in June, witnessed a slow rise in market shares standing at 26.43% or 45.92 million subscribers.

'/%3E%3C/svg%3E)

Network by market shares

Data concerns: The Nigerian telecommunication industry has been witnessing a rise in internet subscribers over the years, just as broadband penetration is rising. However, Nigerians have been made to bear the brunt of slow internet downloads despite high data plans.

- The recently released data, Internet World Stats revealed that the country now ranks 7th in terms of countries with the highest numbers of internet users in the world with 111.6 million subscribers.

- But an earlier report from the United Kingdom-based price comparison website, Cable, revealed that the country’s internet download speed is one of the slowest in the world.

Similarly, as competition heightens, the service providers are equally introducing several strategies to woo customers. Investigations showed that almost all internet service providers recently reviewed their data prices. While prices of data dropped for some, Nigerians are complaining about poor network and quick exhaustion of data.

An internet subscriber told Nairametrics disclosed that“MTN has reduced the price of 2gig data from N1,500 to N1,200, but the rate the data gets exhausted is unexplainable. I get confused when a 2gig data plan finishes in less than 2-weeks. I am not concerned about the cost, but the rate at which it gets exhausted.

“Glo data speed is really frustrating. Although it is cheap, I barely enjoy it due to the very slow download speed.”

“I recently had issues to use my Glo line to call MTN number several for days, and it left me really worried because people could not reach me.”

Upshots: Our Analyst tried to call both MTN and Glo customer care service centres to inquire about the reasons for poor network witnessed in recent times. Glo admitted to having network difficulties for days but noted the issue had been resolved.

Though MTN subscribers dropped for the first time in a year, the drop may not be unconnected to the recent quick exhaustion of data bundles which Nigerians claimed is biting hard.

[READ FURTHER: Nigeria’s internet download speed ranks one of the slowest in the world]