Follow Us on Google Discover

Follow Us on Google Discover

Salary earners in Nigeria are mandated by law to pay tax under the Pay As You Earn (PAYE) scheme. Every month a portion of your salary is deducted as tax leaving you with a net salary to take home.

Taxes under the PAYE scheme fall under the jurisdiction of the State Inland Revenue Service, meaning that all the taxed you pay are remitted to the state of your residence.

For example, if you live in Ogun State but work in Lagos, you are liable to pay tax to Ogun State and not Lagos State.

Nigerian Personal Income Tax Laws have evolved over the years with several amendments introduced to align with the income of Nigerians. The latest amendment was in 2012 when the Goodluck Jonathan Administration signed into law an Amended Personal Income Tax Act, replacing several controversial sections of the act with a simpler and easy to calculate taxable income.

Also Read

The new amendments affect several sections of the Personal Income Tax Act, particularly Section 33 which deals with Personal Relief and Relief for Children, dependants, etc. This has now being replaced with a Consolidated Relief Allowance (CRA) of N200,000 + 20% of gross income.

They have also reviewed the Minimum Tax upwards from 0.5% to 1% and the Tax Table has also been notably amended.

In this article, we will demonstrate how your personal income tax is calculated using the example of a taxpayer named Mr Ahmed.

How to calculate your tax payable

Mr Ahmed earns an Annual Salary Package of N3 million including leave allowance. Mr Ahmed also contributes 2.5% of his basic to the National Housing Fund to enable him to secure a loan.

[Read Also: Does one’s fat salary automatically guarantee wealth?]

Let’s take you through these steps to calculate his taxable income:

(Remember CRA replaces all reliefs including transport, leave allowance, rents etc.)

Step 1:

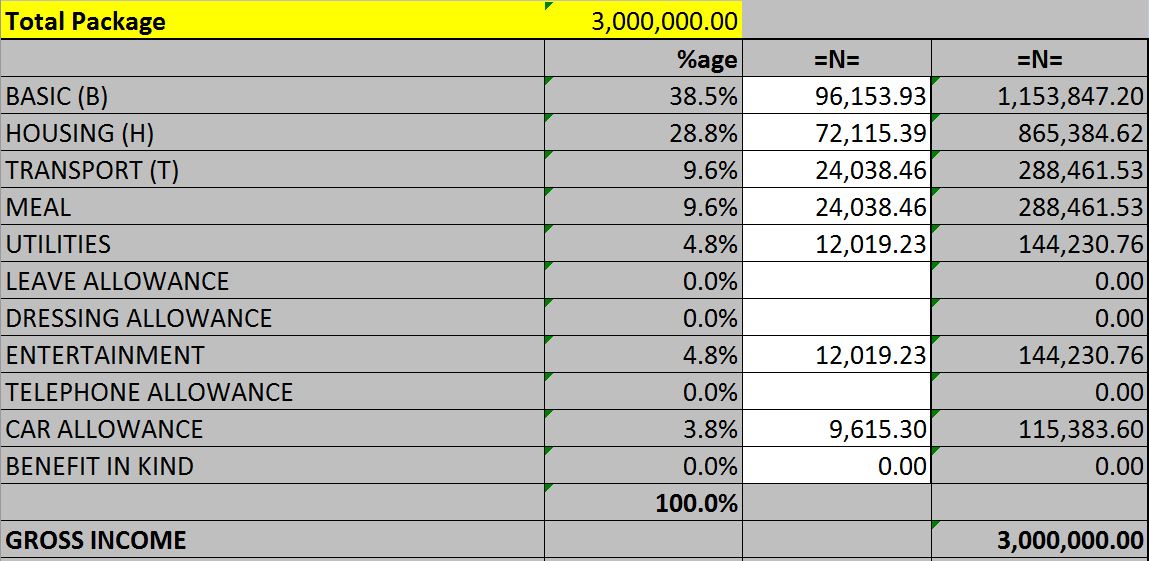

For tax purposes we can break-down his salary as follows:

'/%3E%3C/svg%3E)

Step 2:

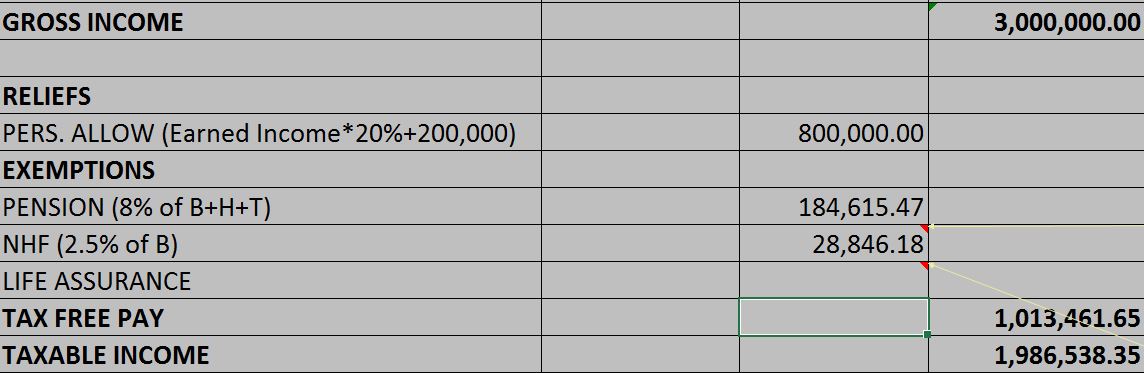

Following which we can now apply the Consolidated Relief of N200,000 plus 20% of Earned Income and also deduct exceptions such as National Housing Fund Contribution (NHF) which is 2.5% of your Basic and also Pension which is 8% of your Basic+Housing+Transport to arrive at your Taxable Income; Please see below:

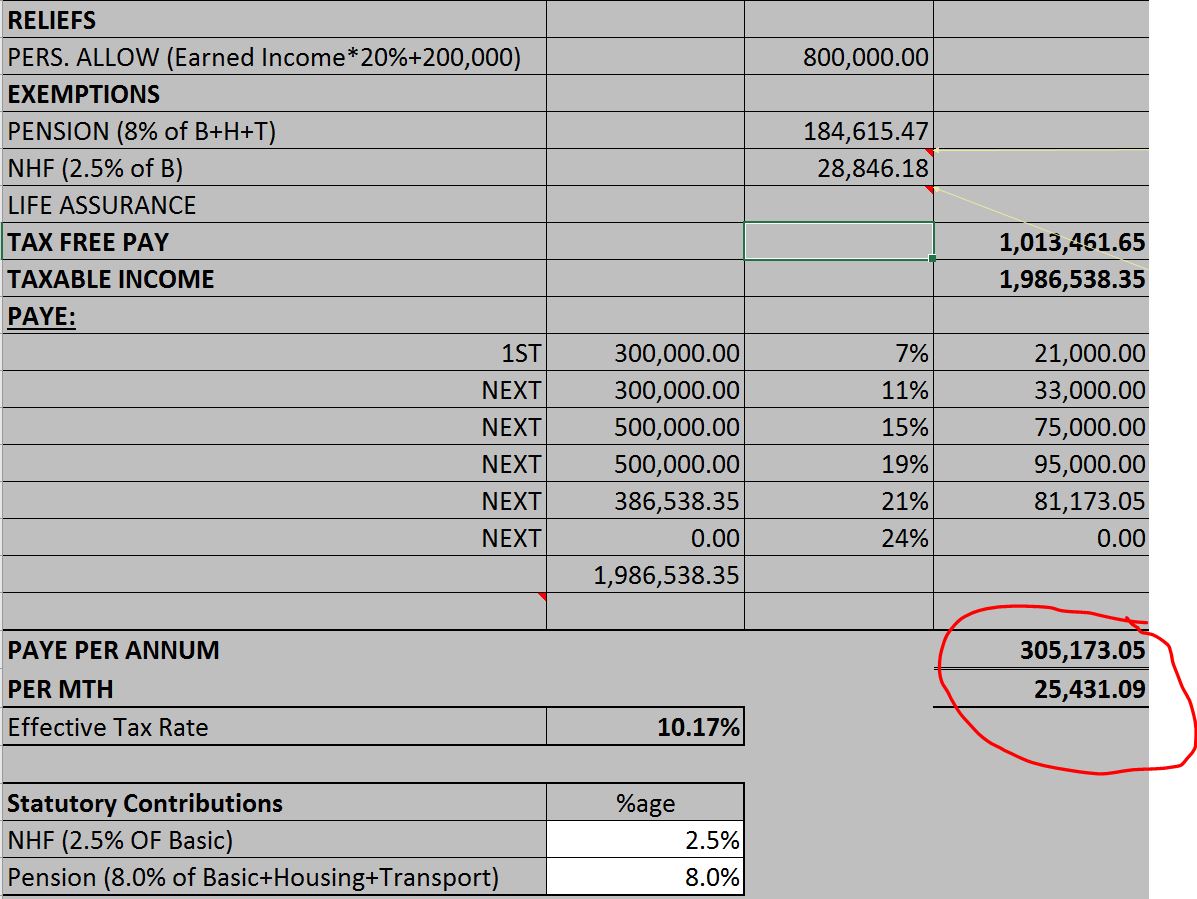

Step 3:

Mr Ahmed will now be taxed on N1,986,538.35 using the new tax table.

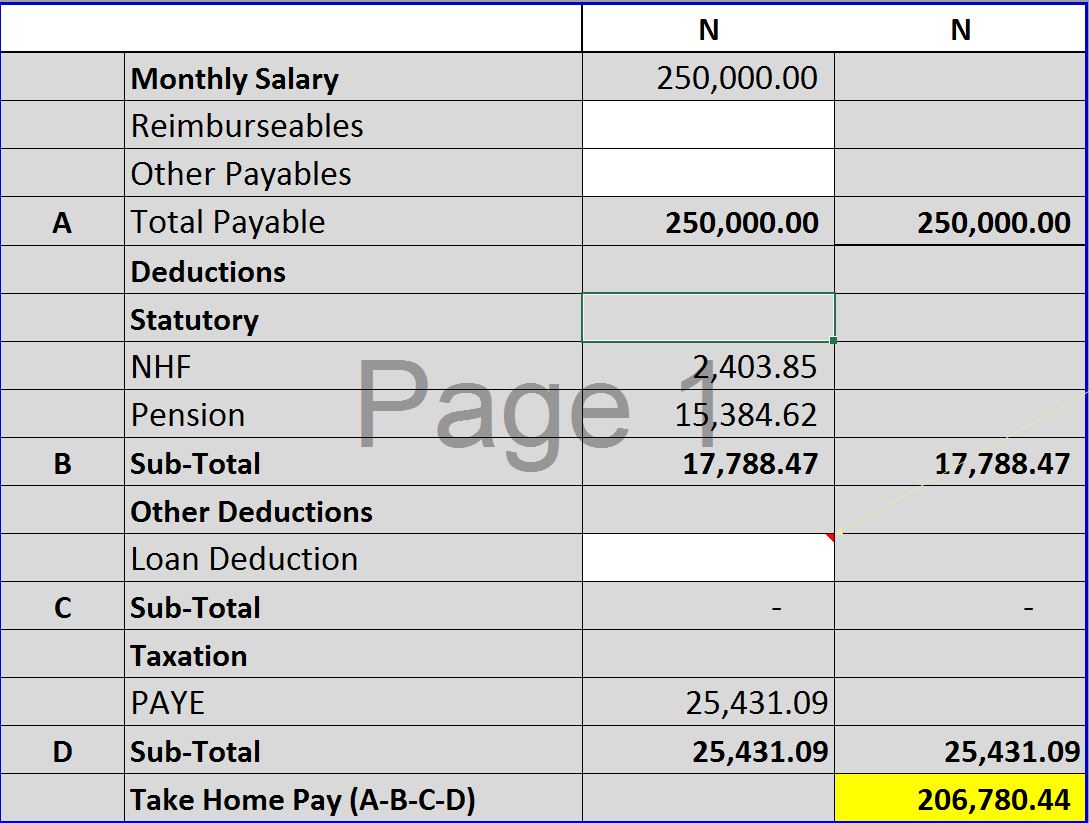

From the table above, Mr Ahmed will expect an annual tax deduction of N305,173.05 or a monthly tax deduction of N25,431.09. This is a 10.17% effective tax rate for Ahmed. And this is what his take home will look like:

[Read Also: Strategies to Reduce Expenses and Save Money]

The amended law makes it very easy to calculate income taxes unlike before, thus eliminating most of the loopholes that were previously being used to exploit taxpayers.

But how can I reduce my taxable income?

The new PAYE template introduced in 2012 makes it more difficult to reduce the amount of taxable income you are subjected to. However, there are still something you can do to reduce your taxable income.

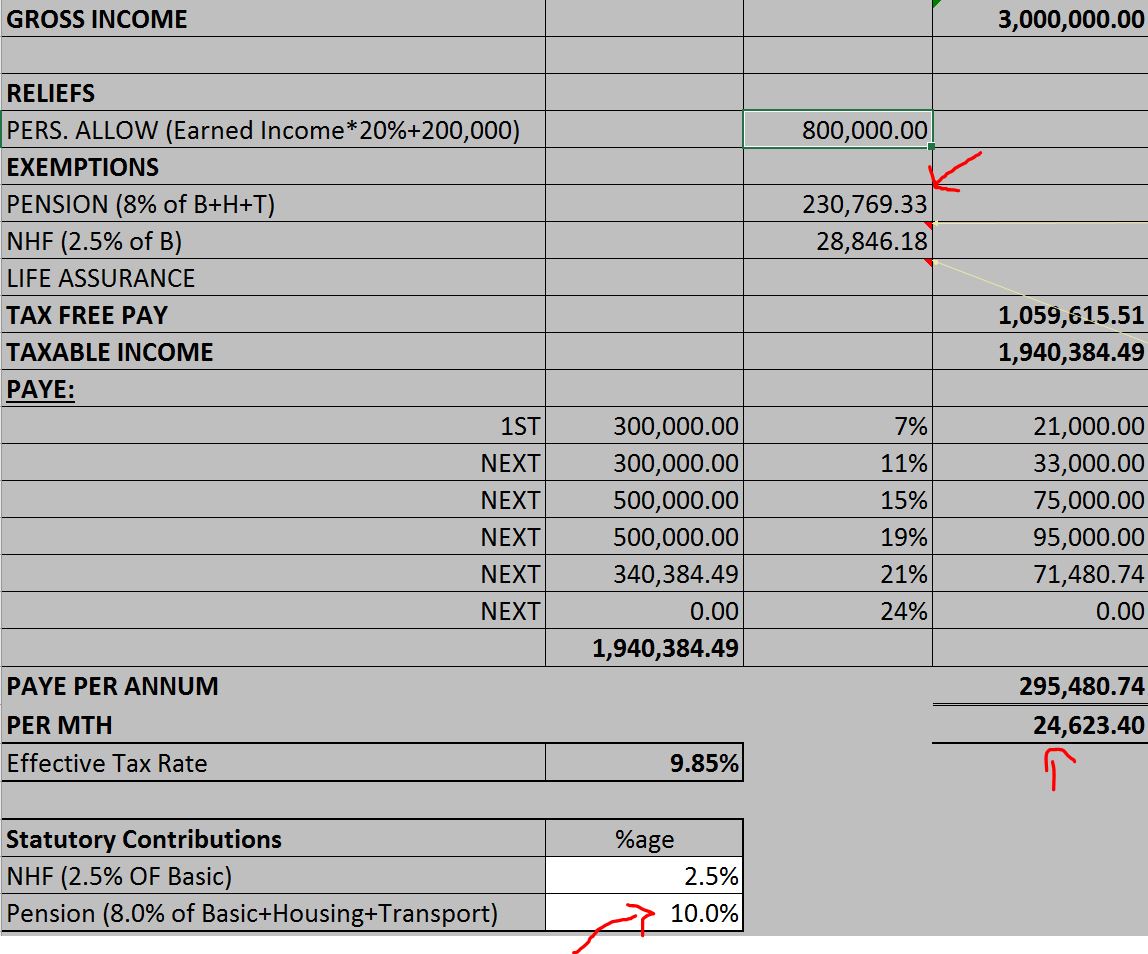

Pension

To encourage pension contribution the Government allows employees to contribute more than 8% of your basic, housing, and transport as a pension contribution. By doing so, you get more tax reliefs, thus lower taxable income. Using the example above, assuming you decide to increase your pension contribution from 8% to 10%, your monthly taxes reduce to N24,623 as depicted below:

It is important to note that by doing this your take-home pay will reduce as your salary will be deducted for the extra pension that you contribute. However, you get compensated for this by the extra return you earn on your pension contributions as well as paying lower taxes. Also, assuming you decide to resign and cash in on your pension within 5 years of contributing it, the new pension reform act of 2014 requires that the additional portion contributed will be taxed. Therefore, you will also have to have contributed it for a period of over 5 years to get a tax rebate.

[Read Also: DMO to auction fresh N145 billion bonds for subscription]

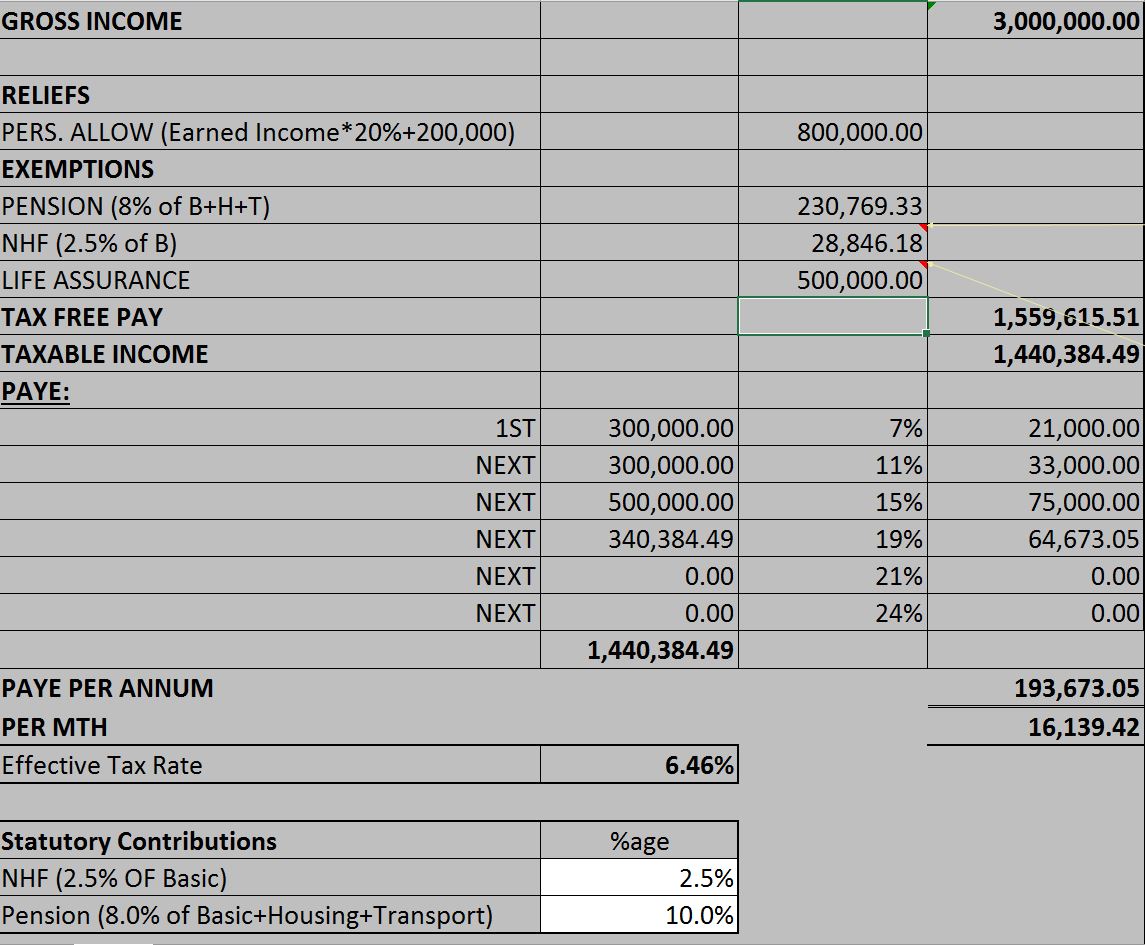

Life Assurance

Life Assurance premiums are those premiums you pay towards insuring an immediate family member in the event that you die. There is no limit to how much you can contribute and how much relief you can get from it. The higher your life assurance, the higher the relief that you get. Assuming Mr Ahmed paid a premium of N500,000 in life assurance during the year and also contributes 10% as pension, His taxes will look like this:

You can see that the tax per month has dropped to N16,139 as against N24,623 when he didn’t pay premiums on life assurance. Just like the increase in pension contribution, this also dents your take home but you get the benefit similarly.

Below is a simple template to help calculate your taxes by yourself. Send us an email or drop a comment if you have issues using it. Help us to help you.

[gview file=”https://nairametrics.com/wp-content/uploads/2017/01/PAYE-TEMPLATE-UPDATED-JAN-2017.xlsx”]

This article was first published on Ugometrics (Nairametrics) in 2012 and was later updated in 2019.

Can you please confirm if there has been a change in the template since the recent amendment in June. Cheers.

No changes has been made. The template is fine. Thanks

Please assuming some one is earning #1000000 (one million Naira ) per month. How much suppose to be his tax, paye per month.?

Am having issues with this tax issue deduction. Was trying to figure something out but looks complicated…if i may ask, someone who has an annual gross pay of 4026000…how much is meant to be deducted for PAYE and contributory pension monthly? I’ll L?k to get the answer in my email addy…thanks in advance

use this template https://ugometrics.com/2012/01/26/how-to-calculate-your-taxes-2-using-the-new-personal-income-tax-amendment-act/

Sorry, I meant this template ===>> https://resourcedat.com/2012/01/sample-p-a-y-e-template-based-on-2012-pita-amendment/

Thanks so much.

please kindly send me these new amended personal income tax template in my E-mail thanks

please kindly send me these new amended personal income tax template in my E-mail above

Thanks

Please send a computation of tax relief on INSURANCE PREMIUM.

Thanks

SIR,WHAT IS THE MINIMUM RANGE OF GROSS PAY FOR WHICH 1% CAN BE CHARGED?

This is dependent on what your allowed amount is and your gross pay. Is either 1% of gross pay or (Gross Pay – 200000 -20% of Gross Pay- Other Reliefs) subjected to tax calculator – the one that is higher is used.

Please kindly send into my email box; the current copy(2015) of the Annual return form for PAYE tax IN Nigeria.

oh seen. was looking for this earlier

thank you

Try out this Nigeria income tax calculator: https://africa.calculator.co.ke/nigeria-firs-payroll-income-tax-paye-calculator Should help clear things up!