Welcome to Nairametrics‘ summary of the daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills. This is brought to you by Zedcrest.

This report is dated May 21st, 2019.

***CBN Urges Banks to Lend or Lose Access to Government Bonds***

Key Indicators

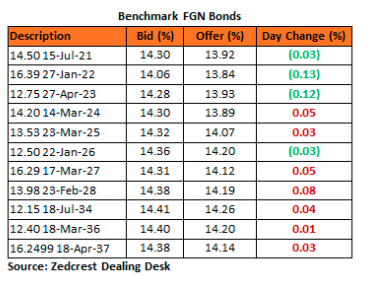

Bonds: The FGN Bond market traded on a relatively mixed note, with slight profit taking observed on the mid to long end of the curve, ahead of the FGN bond auction scheduled for tomorrow, whilst yields on the shorter end of the curve compressed lower in tune with the still depressed level of rates in the T-bills market. Yields were consequently unchanged on average.

The DMO will offer a total of N100bn of the 5, 10 and 30-yr bonds at the auction for tomorrow, and we expect rates to clear c.15 -20bps lower from their previous auction levels, with a moderate level of oversubscription expected mostly on the 10 and 30-yr maturities.

Treasury Bills: The T-bills market remained slightly bullish, with yields lower by c.5bps on the back of some more demand on the mid to long end of the curve. The rate of decline in yields has however slowed from previous sessions, with rates finding support at c.11.50% on the mid to long end of the curve.

The CBN decided to leave all parameters including its monetary policy rate unchanged at its MPC meeting concluded today, sighting renewed inflationary pressures, concerns for FX stability and the need to monitor real sector developments since the latest cut in the MPR to 13.50%. The CBN, however, frowned on the ‘over-investment’ of banking sector deposits in risk-free government securities which have consequently crowded out the much-needed credit to the private sector and stated its intentions to check the unlimited access to government securities by DMBs.

Whilst the CBN has slowed down its spate of OMO issuances in recent sessions, we await more clarity on how it actually intends to implement its aforementioned policy stance towards the DMBs. The market is however expected to be relatively stable in the near term, given the hold in the MPR.

Money Market: Rates in the money market remained relatively stable, as system liquidity improved to c.N266bn opening the day. The OBB and OVN rates consequently ended the session at 4.57% and 5.29% respectively.

We expect rates to remain stable at these levels tomorrow, as there are no significant outflows anticipated.

FX Market: At the Interbank, the Naira/USD rate was unchanged at N306.90/$ at the spot market, while the SMIS rate increased slightly by 0.03% to N356.92/$. The NAFEX closing rate in the I&E window however declined by 0.08% to N360.42/$, as market turnover improved by 65% to $138m. At the parallel market, the cash and transfer rates remained unchanged at N359.00/$ and N363.50/$ respectively.

Eurobonds: The NIGERIA Sovereigns improved slightly, with yields compressing by c.3bps on the day. We witnessed the most gains still on the shorter end of the curve.

In the NGERIA Corps, $200k of the DIAMBK 19s matured and were repaid to holders at par, while we saw slight interests on the ZENITH, UBANL and FIDBAN 22s.

________________________________________________________________________

Contact us:

Dealing Desk: 01-6311667 Email: research@zedcrestcapital.com

Disclaimer: Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}