Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

Bond Market Trades Flat, Despite Significant Cut in Auction Rates

***FG launches Micro Pension Plan for informal sector***

Key Indicators

Bonds

The FGN Bond market traded on a relatively flat note despite the significant cut in stop rates at yesterday’s auction. We witnessed slight demand on the short end of the curve (23s & 24s) countered by some profit taking on the 2028s which trended higher by c.20bps on the day, (having compressed significantly in the previous session). Yields were consequently unchanged on the day, closing at c.14.30% on average.

We expect yields to trend slightly upwards due to the recent profit taking sentiments in the market. We should however witness some renewed demand if the CBN maintains a hold on OMO sales.

Treasury Bills

The T-bills market traded on a relatively flat note, even as the CBN held of on OMO despite the c.N60bn in OMO T-bill maturities today.

Market players anticipate a renewed OMO auction by the CBN tomorrow, due to expected inflows from FAAC payments. We expect the market to trade slightly bearish if this occurs.

Money Market

Rates in the money market declined by c.5pct as inflows from retail FX refunds bolstered system liquidity which opened the day at c.N80bn positive. The OBB and OVN rates consequently ended the session at 10.07% and 10.71% respectively.

We expect rates to trend slightly higher tomorrow, due to expected outflows for Bond auction debits, a possible OMO sale and Retail FX provisioning by banks.

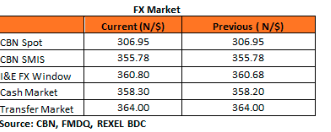

FX Market

At the Interbank, the Naira/USD rate remained unchanged at N306.95/$ (spot) and N355.78/$ (SMIS). The NAFEX closing rate in the I&E window depreciated further by 0.03% to N360.80/$, whilst market turnover improved by 74% to $203m. At the parallel market, the cash rates depreciated further by 0.03% to N358.30/$ whilst the transfer rate remained unchanged at N364.00/$ respectively.

Eurobonds

The NGERIA Sovereigns remained slightly bearish, with yields higher by c.3bps on the day. Investors however showed renewed interest for duration plays on the longer end of the curve (47s and 49s).

In the NGERIA Corps, we witnessed interests mostly on the DIAMBK 19s and FIDBAN 22s.

__________________________________________

Contact us:

Dealing Desk: 01-6311667 | Dayo: 07032208237 | Seyi: 08023231396 | Nnamdi: +2348133385000 | Tosin: +2347039394376

Email: research@zedcrestcapital.com

{kind=link}