Welcome to Fixed Income Market Monitor, where we avail you the opportunity to keep abreast with the investing outlook for the new week. Now, let’s get right into the details.

Money Market

The money market rate increased marginally last week as the Overnight rate (OVN) and Open Buy Back (OBB) rose to 11.67% and 11.17% respectively. Consequently, the average money market rate rose by 1.80% to settle at 11.42% despite the increase in the System liquidity to cN413bn from cN157bn in the previous week. Major inflow for the week included: OMO Maturity of cN213bn, Retail FX refund of cN165bn while Major Outflow included Weekly Wholesale, Invisible and SME FX auction of $210mn, Bi-weekly Retail FX Auction of N350bn and OMO Sale of cN400.48bn.

We expect the rates to close higher this week barring any significant inflow due to the following reasons: CBN weekly FX auctions on Monday, anticipated OMO auctions, and T-bills Primary Market Auction during the week.

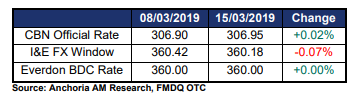

Forex: USD/NGN

The CBN Official rate grew by 0.02% to close at N306.95/$ while the rate in the Investors and Exporters’ FX Window fell by 0.07% to close at N360.18/$ as we continue to witness buoyant market turnover with inflows from Foreign Portfolio Investors. However, Naira at the parallel market remained unchanged to close at N360.00/$ (using the Everdon BDC Rate).

We expect rates in the parallel market to remain constant as the apex bank continues to supply FX into the market, coupled with its frequent Wholesale and Retail SMIS programme.

Commodities

The Brent Crude Oil and WTI Crude Oil rose by 2.16% and 4.37% to close at $67.16 and $58.52 per barrel respectively due to the following reasons:

a) massive power outage in Venezuela that hindered the oil exporter’s ability to load tankers

b) a bullish inventory report from the U.S. Energy Information Administration

c) Saudi Arabia’s commitment to further cutting its output, targeting sub-10 million barrels per day (bpd) and cutting exports to less than 7 million bpd.

Fixed Income

Bond: FGN: Despite a relatively quiet trading week due to the apathy of Foreign Portfolio Investors in the market, the bond market ended the week on a bullish note with increased demand seen on few maturities especially 2020 (-57bps) and 2037 (-16bps) bonds. Average yields fell marginally by 10bps to close the week at 14.19%. It can be estimated that the local participation account for between 80 – 90% of market activity.

Week Ahead: We expect the market to trade flat or on a bearish note if the apathy from Foreign Investors continue. Other factors expected to shape the market in the week ahead include:

• Anticipated Coupon payments

• Bond Auction scheduled to hold on 27th March 2019

• Monetary Policy Committee Meeting between 25th and 26th March 2019

Treasury Bills

Due to the increase in system liquidity during the week, the treasury bills market traded on a bullish note. Consequently, the average yield fell by 17bps to close the week at 13.31%. The T-bills and OMO auctions conducted during the week witnessed a reduction in rate showing the expansionary stance of the Central Bank of Nigeria and expected decline in rates.

Also, CBN has scheduled to conduct another round of T-Bills Primary

Market Auction on Wednesday, 20 March 2019.

Contact Anchoria Asset Management Limited for more information

Email: research@anchoriaam.com

www.anchoriaam.com

{kind=link}