Analysts at Coronation Research have a GDP growth forecast of 2.25% y/y for the twelve months ending December 2019. The analysts made this known in their report issued following the release of Q4 2018 GDP numbers by the National Bureau of Statistics.

Here are excerpts from the report.

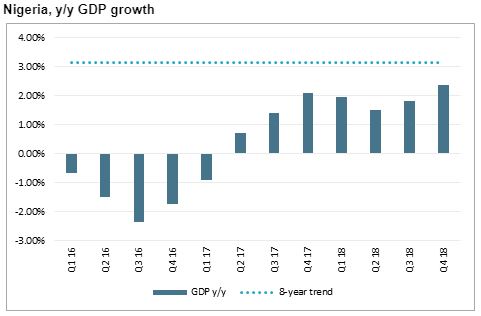

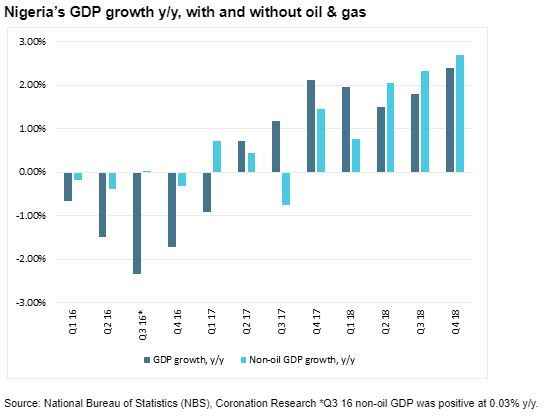

Q4 2018 GDP was reported today at +2.38% y/y versus the Bloomberg consensus estimate of +2.10% y/y. Non-oil growth was a respectable +2.70% y/y and has accelerated over the past four quarters. See page 2.

FY 2018 GDP was +1.93% y/y, compared with +1.76% y/y for 9M 2018 and +0.82% y/y for 2017. The World Bank’s revised estimate for 2018 was +1.90% y/y.

While below trend, growth is on a gentle upward slope. We forecast +2.25% y/y growth for 2019.

Positive implications for equities. Lack of loan growth was the bugbear for listed banks in 2018: more growth, particularly in the Telecoms and Manufacturing sectors, may point to renewed loan demand in 2019, though the large Trade sector (up by just 1.02% y/y) remains essentially weak. Segmental data for construction, +2.05% y/y, bodes well for the cement industry.

Mildly positive for market interest rates. As we argue in Coronation Research, Year Ahead 2019, A tale of two halves, 15 January, market interest rates support foreign portfolio investment, but may be cut in Q4 or even Q3 2019 if inflation moderates. We are already seeing some read-though in 10-year bond yields.

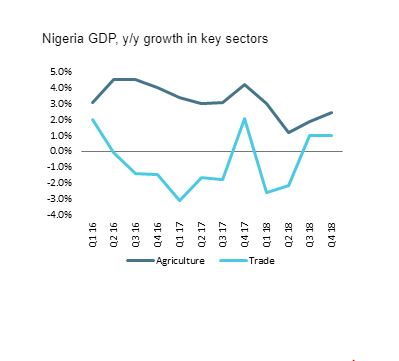

Mildly positive for inflation. The Agriculture segment (26% of GDP) showed improved growth (+2.46% y/y) and to the extent that this reflects improved production, we expect inflationary pressure to moderate towards mid-year, if momentum is sustained.

Non-oil & gas GDP

Robust performance in Non-oil GDP

Non-oil GDP accelerated throughout 2018, growing steadily from +0.76% y/y in Q1 18 to +2.70% y/y in Q4 18. We see a pattern emerging as the economy emerged from recession. Whereas GDP was reliant on its oil component to stimulate growth for much of the past, and therefore highly susceptible to volatility in the prices and production, non-oil GDP has become more resilient to such shocks. The Q3 2017 0.76% y/y decline in non-oil GDP now reads as an isolated event post-recession.

This resilience is even more impressive given that Agriculture is not growing as quickly as it did in 2016 and 2017, while Trade and Manufacturing have performed inconsistently. We expect Agriculture to post a very gradual recovery to its trend growth rate of 3%.

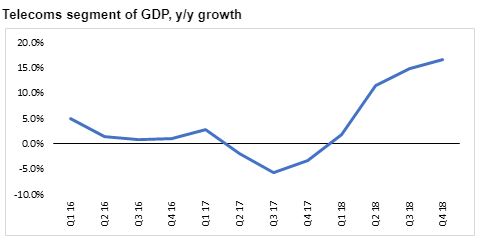

More recently Telecoms has been the main driver of growth in non-oil GDP. The sector grew 11.33% y/y for FY 2018. it is easily the best performing sector of the top six contributors to GDP well above Agriculture which grew by 2.12% y/y for FY 2018.

On the other hand, Oil & Gas GDP has underperformed in 2018, following one quarter of positive growth (Q1 2018, 14.77% y/y) with three consecutive quarters of year-on-year decline. The volatility of Oil and Gas itself is not surprising – in the last eight years it has recorded growth rates between +24.21% y/y and -23.04% y/y.

GDP Breakdown

Breakdown among the major segments

The top six sectors accounted for 74.10% of the Nigerian economy in Q4 2018, down 406bps from their collective contribution in Q3 2018. In order of size they were Agriculture, Trade, Telecoms, Manufacturing, Oil and Gas, and Real Estate.

In Q4 2018 Agriculture (25.83% of GDP) grew by 2.46% y/y. Trade (16.29% of GDP) grew by 1.02% y/y. Telecoms (9.73% of GDP) grew by 16.67% y/y. Manufacturing (8.75% of GDP) grew by 2.35% y/y. Oil & Gas (6.97% of GDP) contracted by 1.62% y/y. And Real Estate (6.52% of GDP) fell by 3.85% y/y.

Therefore, of the six largest sectors, four grew and two contracted. Agriculture sustained its upward track towards trend growth of 3%, indicating, a slowdown in core inflation is likely in the medium term. Manufacturing performance and PMI data are now showing signs of convergence after a period of disconnect. Telecoms consolidated it status as a core stimulant for non-oil GDP growth having reported double-digit growth over the last three quarters. Oil & Gas recorded a third consecutive quarter of year-on-year decline period post-Q1 17, mirroring the global trend in oil prices. Trading was up for two consecutive quarters. Real Estate remained in a sticky decline, with no clear pattern emerging in its development.

The growth in Agriculture remains at just below its 3% long term trend. At 26% of GDP, its provides a defense against the steep volatility that characterizes the Oil & Gas component.

Trade remains weak but positive

While a small percentage of consumers assess short-term unsecured credit for current consumption, most consumers fund consumption from out of pocket appropriations. The effect is some headroom for import-elastic consumption but also more importantly, demand for cheaper substitutes where possible. Trade growth suffers in this regard.

Positive growth in Manufacturing is being sustained by stability in the foreign exchange market, a feat achieved by the CBN’s willingness to supply US dollars to the foreign exchange markets, while offering inflation-adjusted yields in excess of 500bps to foreign investors. The combined growth in both Trade and Manufacturing, two sectors highly responsive to consumers wallet sizes and expectations, point to a pass-through of election-induced spending in the short term and broader recovery in the economy.

Swing Sectors

Telecoms – conditions at their best in years

The Telecoms sector (9.73% of GDP), grew by 16.67% y/y in Q4 2018. Building on its Q3 18 performance, the sector extended gains to post an 11.33% year-on-year growth among peers with contribution to GDP above 6.00%.

Telecoms segment of GDP, y/y growth

Strong growth in Telecoms reflects new investments, growing franchises and growth in internet and mobile banking. A deeper penetration of data-reliant devices in the Nigerian market, and an increasing migration of media services to internet-driven platforms otherwise traditionally offered off-net explain the strong performance. We expect Telecoms to leverage participation as Payment Service Banks and sustain growth going forward

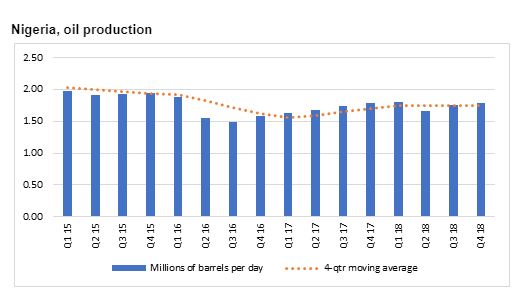

Oil & Gas GDP continues to exhibit volatility. Nigerian oil production was flat year-on-year and up 1.33% q/q in Q4 2018. However, actual cargo loadings from exports terminals declined by 7.29% q/q and 5.53% y/y in Q4. This, together with an average quarterly price below US$70.00bbl, partly explains the slide in Oil & Gas GDP for the quarter. A degree of volatility in production is likely to be addressed by the new Egina Oil field but Nigeria remains exposed to price volatility.

Pattern of growth and outlook for 2019

Q4 2018 GDP growth outperformed the Bloomberg consensus estimate of 2.10% y/y. While some of this growth may have been induced by election-related demand, we believe that more fundamental factors, in particular, Naira foreign exchange stability, are at work.

Monetary policy is less likely to change in response to the latest development in GDP, at least in H1 2019. Real growth of 1.93% for FY 2018 was achieved on the back of adjustments in fundamental variables, in our opinion. For instance, demand for loans was weak but we do not read this as an effect of market interest rates 300pbs above the Monetary Policy Rate (MPR). Prime lending rates data show a standard deviation of only 1.05pps since 2006, suggesting that interest rates are seldom low. We expect a positive shift in manufacturers’ and investor’ confidence, to have spurred growth, irrespective of interest rates.

Fiscal policy, in so far as it relates to government spending, is limited in contributing to real sector growth by its sheer smallness relative to the economy as a whole. Increasing debt servicing costs further squeeze government revenues and implementation of capital expenditure.

However, the trend in Agriculture is positive. Even more so is the performance of the Telecoms sector which headlined overall growth in Q4. A stable exchange rate remains the platform for Trade and Manufacturing to rebound though slack demand are likely to keep growth capped.

Downside risks to GDP growth remain from the risk of declining crude production levels and oil price volatility, as well as the performance of Real Estate. Nevertheless, we expect our base case GDP forecast of 2.25% y/y for

{kind=link}