Daily performance of major economic indicators and highlights from tradings sessions and key statistics such as T-bills, bonds, FX rates, inflation, oil price.

- Central Bank conducts yet another OMO auction in a bid to manage excess liquidity

- Eurobonds for oil producing countries and companies remain bearish amidst low crude prices

KEY INDICATORS

Bonds

Risk-off sentiments on FGN Bonds continued today as the market opened the week on quiet note. Market trading volumes remained on a decline with less than N1bn executed intraday, reflecting the weak appetite for FGN bonds. Consequently, yields traded flat across the curve, with slight sell-off seen at the short-end (2020s) and mid-end of the curve (2027s & 2028s).

We expect the market to trade scantily in the interim as investors weigh-in the effects of lower global oil prices on government borrowing cost. We retain a cautious outlook on bonds with a bearish bias till the end of the year.

Treasury Bills

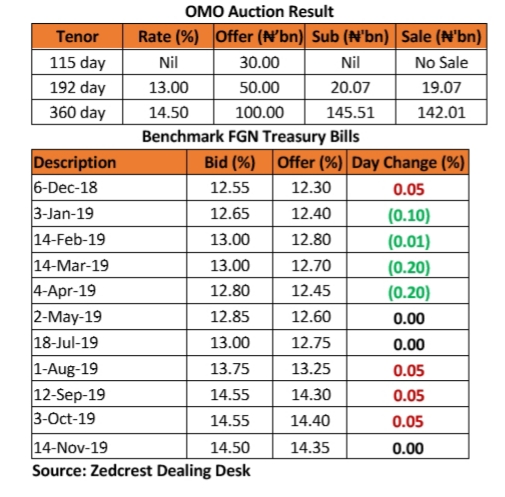

Trading in the T-bills market was muted on the day as the CBN conducted an unexpected OMO auction, a divergence from the usual OMO T-bills maturity vs OMO auction trend in past sessions. We saw slight bullish sentiments on the short end of the curve, while the medium to long end of the curve traded bearish due to more supply of OMO T-bills.

The CBN sold a total of N161.08bn OMO T-bills across two maturities, 192- and 360-days, while maintaining stop rates at 13.00% and 14.50% respectively. There was no sale recorded on the 115-day maturity due to no demand on that maturity.

We expect the market to trade bearish tomorrow due to the reduced System Liquidity as well as supply expected from the T-bills PMA to be conducted later in the week.

Money Market

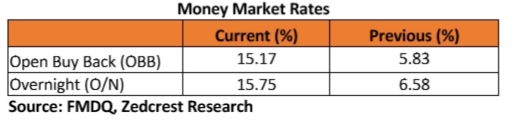

Money Market rates increased opening the week, off the back of outflows via the CBN’s OMO auction as well SMIS FX Wholesale Intervention conducted today. The OBB & O/N rates closed at 15.17% (from 5.83%) and 15.75% (from 6.58%) respectively. System liquidity is consequently estimated to close lower at c.N118.38bn positive.

We expect rates to remain in double digit territory in the interim as there are no OMO maturities expected this week. However, market participants may get some respite from FAAC payments as the month draws to a close.

FX Market

At the Interbank, the Naira/USD rate depreciated by c.0.02bps to close at N306.80/$ (spot), from N306.75/$ previously but remained unchanged at N359.81/$ (SMIS). At the I&E FX window a total of $147.30bn was traded in 303 deals, with rates ranging between N361.00/$ – N365.00/$. The NAFEX closing rate appreciated by c.0.23% to close at N363.85/$ from N364.70/$ previously.

At the parallel market segment, the cash and transfer rates both remained unchanged to close N364.00/$ and N366.50/$ respectively.

Eurobonds

Recovery in global oil prices was insufficient to provide respite for sovereign papers of oil producing countries, and the NGERIA Sovereigns were no exception. Yields on the NGERIA Sovereigns inched up further by c.7bps on the average across all the tickers on the curve. The major losers on the day were the NGERIA 21s and NGERIA 23s losing c.13bps and c.17bps respectively.

NGERIA Corps showed continued weakness amidst low oil prices. Yield expanded the most on the SEPLLN 23s by c.25bps, while in a surprise twist yields compressed on the Zenith 19s by c.127bps.

Disclaimer

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}