Daily performance of major economic indicators and highlights from trading sessions and key statistics such as Treasury Bills, bonds, FX rates, inflation, oil price.

T-bills Market Trends Bearish as CBN Hikes OMO rate

Oil Traders Consider Nigerian Proposal to Prolong Fuels Swap

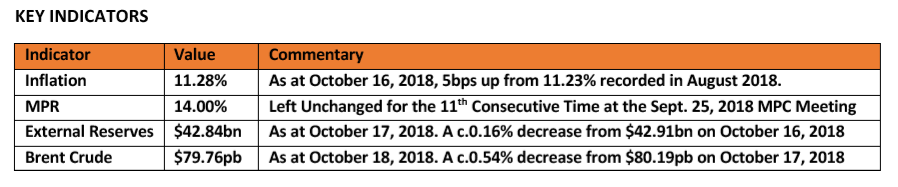

KEY INDICATORS

Bonds

The bond market remained relatively flat, but spreads tightened as offers improved slightly across most maturities, due to expectations of a hike in OMO rates by the CBN. Yields ticked higher on the longer end of the curve, while they compressed slightly on the shorter end, save for the 24s which ticked higher for the second consecutive session. On the average, yields were down by c.1bp on the day.

We expect a continued bearish positioning by market players as yields become gradually more attractive on T-bills, whilst we look forward to the FGN bond auction, where the DMO expects to raise ₦115bn in 5, 7 and 10yr bonds.

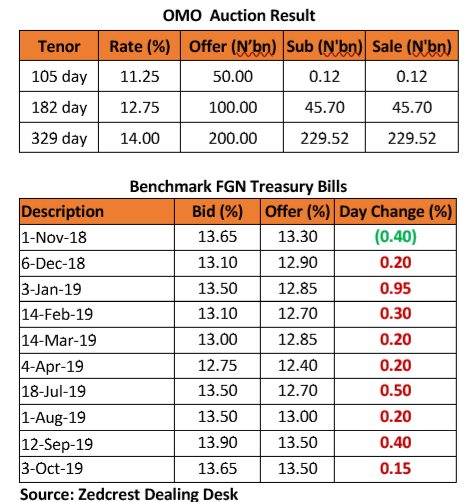

Treasury Bills

The T-bills market traded on a signifcantly bearish note, with yields trending higher by c.20bps. Selloffs were mostly on the longer tenured bills (Sep – Oct), as news of a higher than expected OMO clearing rate filtered into the market early into the trading session.

The expectations for higher OMO rates were confirmed by the OMO auction result released later in the day, as the CBN sold a total of c.275bn at +25bps higher on the 105 and 182 day bills and +50bps higher on the 329 day bill. With the effective yield on the long tenor OMO now at c.16%, yields on the long end of the curve have now hit levels last seen at the start of the year.

We expect the market to close the week on a relatively flat note. Market players should however cherry pick on some attractive bills on the shorter end of the curve.

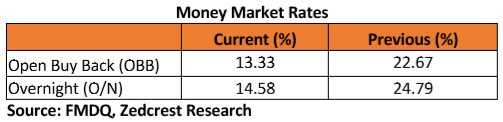

Money Market

In line with our expectations, the OBB and OVN rates, dipped below the 20% mark, closing today at 13.33% and 14.58%, as system liquidity was slightly bolstered by the net OMO and bond coupon payments (+104bn) today. System liquidity is consequently estimated at c.N76bn positive from a negative position of c.N28bn opening the day.

We expect rates to close the week at these levels, as there are no significant outflows expected.

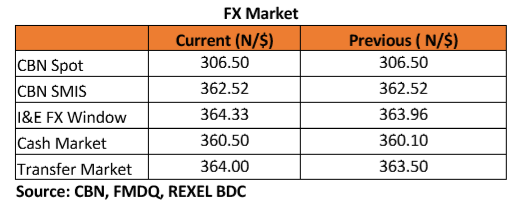

FX Market

At the Interbank, the Naira/USD rate remained stable at ₦306.50/$ (spot) and ₦362.52/$ (SMIS). At the I&E FX window a total of $70.74mn was traded in 284 deals, with rates ranging between ₦358.00/$ – ₦365.30/$. The NAFEX closing rate depreciated by c.0.10% to ₦364.33/$ from ₦363.96/$ previously.

At the parallel market, the cash rate and transfer rates depreciated by 40k and 50k to ₦360.50/$ and ₦364.00/$ respectively.

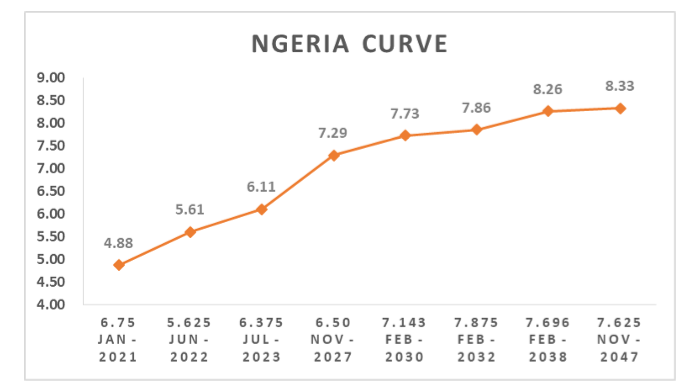

Eurobonds

The NGERIA Sovereigns remained firmly bearish in today’s session, on the back of the approval of a New Eurobond issuance by the Nigerian senate yesterday. Yields were higher by c.10bps d/d, with the most selloffs still on the 20-yr (2038).

In the NGERIA Corps, the DIAMBK 19s gave up some gains, while interests remained strong on the SEPLLN 23s.

Disclaimer:

Whilst proper and reasonable care has been taken in the preparation and accuracy of the facts and figures presented in this report, no responsibility or liability is accepted by Zedcrest Capital or its employees for any error, omission or opinion expressed herein. This report is not an investment research or a research recommendation and should not be regarded as such. The information provided herein is by no means intended to provide a sufficient basis on which to make an investment decision.

{kind=link}