KEY INDICATORS

Monetary Policy Committee Meeting

The Monetary Policy Committee at its 262nd meeting announced its decision to maintain its benchmark rates at 14.00% as well as other monetary policy parameters, in line with market consensus. The Committee decided by a vote of seven (7) members to retain the Monetary Policy Rate (MPR) at 14.00%, while two (2) members voted to increase the MPR by 50bps and one (1) member voted to increase the MPR by 25bps.

The announcement by the MPC was largely in line with market consensus, as inflationary pressure is anticipated to rise and capital outflows picking up amid a selloff of emerging-market assets. Three out of 10 panel members voted to raise the benchmark rate, up from only one at the previous Committee meeting. The effect of the hawkish stance by the MPC should feed into bearish sentiments for the direction of yields by the year’s end, in addition to the Committee’s concern with the inflationary pressures from the liquidity impact from the 2018 budget, increasing FAAC distribution and pre-election spending.

Bonds

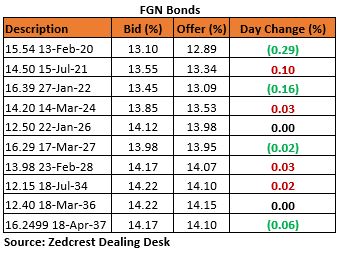

The bond market continued to trade cautious, as market participants waited the announcement of the MPC’s decisions. Yields compressed by c.4bps on the average across the curve, as mixed trades were witnessed on select maturities. Yields on the 10-year bond (2028s) to be opened at tomorrow’s auction, expanded by 3bps while some demand on the long end (2037s) saw yields compress by 6bps.

The monthly FGN Bond auction floated by the Debt Management Office (DMO) is scheduled for tomorrow. The DMO will be reopening the 5-, 7- & 10-yeard bonds, can could sell between N75bn-N100bn, a 50% increase from the previous calendar. Market expectation remains for stop rates for the bonds on offer at the auction to close higher than current secondary market levels. Please our forecast below:

Treasury Bills

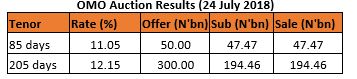

Consequently, T-bills market also traded cautious ahead of the MPC as well as the supply of securities via an OMO auction. The Central Bank sold a total of c.N252bn in 85- and 205-day bills, in a bid to manage the excess system liquidity from outstanding FAAC and bond coupon payments, while maintaining stop rates at 11.05% and 12.15% respectively. Discount rates compressed by a 3bps on the average across the benchmark securities.

We expect market to remain cautious, as market participants still expect the CBN to provide supply via another OMO auction during the week.

Money Market

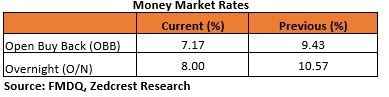

The interbank opened with buoyant liquidity (c.N573.10bn) via inflows from outstanding FAAC payments. Despite the CBN’s attempt to stem the excess liquidity via the sale of OMO securities, market liquidity levels drove money market rates down to close 7.17% and 8.00% for Open Buy-Back (OBB) and overnight (O/N) respectively.

We still expect the system liquidity to remain buoyant for the rest of the week, as OMO maturities N404.32bn are expected to hit the system later in the week. Lack of funding pressures should keep the rates down and the CBN is expected to offer another OMO auction to manage the excess liquidity.

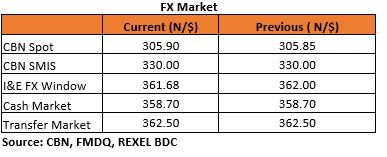

FX Market

The Naira remained relatively stable, with the Interbank rate closing at N305.90/$ (from N305.85/$ previously. The NAFEX rate appreciated slightly by 32k, closing at N361.68/$ (from N362.00/$ previously).

The Naira remained stable in the parallel market, as both the USD cash and transfer rates were maintained at gaining at N358.70/$ and N362.50/$ respectively.

Eurobonds

A quiet trading session for NGERIA Sovereigns saw yields further expand by a single basis point on the average across the trade tickers in repricing.

The NGERIA Corps on the other hand enjoyed some investor interests, as yields compressed by an average of c.4bps across the curve. Trading activities were witnessed on the GTBANK 18s, UBANL 22s & FIDBAN 22s.

{kind=link}