KEY INDICATORS

Bonds

The bond market witnessed tepid interest, as yields compressed by c2bps on the average across the curve. Pockets of demand were witnessed at the short to mid-end of the curve particularly on high-coupon bearing instruments such as the 22s & 24s.

Market participants remain cautious on bonds with the release of the June 2018 inflation report, Monetary Policy Committee (MPC) meeting and the FGN bond auction all schedule for next week. Expectations for a lower inflation figure (analysts’ forecasts range between 10.90% and 11.20%), and the MPC to steady the course and higher stop rates at the bond auction provide a mix of sentiments for direction of yields in the market.

We maintain a bearish outlook on bonds as higher stop rates expected at the auction due to more funding pressure on the Debt Management Office (DMO) should translate into weakened yields in the secondary market.

Treasury Bills

The T-bills market was also relatively quiet, with buy activities witnessed on some select maturities. Discount rates compressed by a single basis point on the average across the benchmark securities.

We also maintain a bearish outlook on T-bills as demand continues to slow down. Reduced system liquidity as a result of FX funding should put pressure on T-bills, especially at the short to mid-end of the curve.

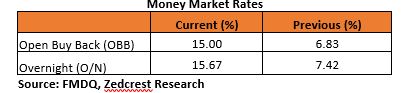

Money Market

Funding pressures as market participants made provisions for the Retail SMIS FX auction by the CBN saw interbank money market rates increase to close at 15.00% & 15.67% for the Open Buy-Back (OBB) rates and overnight (O/N) respectively.

We expect the market liquidity to remain stretched opening and for the most of next week, with some respite expected later in the week from OMO maturities N404.32bn which will be closely monitored by the CBN.

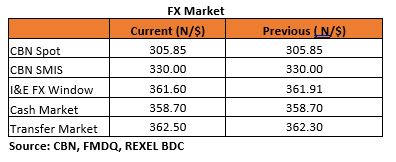

FX Market

The Naira maintained its status quo to close the week across the various trading windows, as the Interbank rate closed at N305.85/$ for a third consecutive trading day. The NAFEX rate appreciated by 31k, closing the week at N361.60/$ (from N361.91/$ previously).

The Naira also traded relatively flat at the parallel market. The USD cash rate remained stable at N358.70k while the transfer rate depreciated by N0.20k to close the week at N362.50/$ respectively.

The CBN commenced the sale of Chinese Renminbi alongside the US Dollars as it took bids for the Retail SMIS FX auction today. This is the first of such bids, following the yuan currency swap deal between Nigeria & China worth the equivalent of $2.4billion since May earlier this year.

Eurobonds:

There was demand for NGERIA Sovereigns and NGERIA Corps at the last trading session for the week, as yields compressed by c.8bps & c.6bps on the average respectively.

Investor interest in Nigerian dollar-yielding assets continue to strengthen on the back rebounding oil prices.

{kind=link}