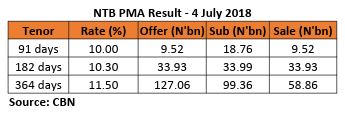

DMO Maintains 60% Rollover of Maturing PMA Bills

AfDB Partners African Nations to Narrow Continent’s Investment Gaps

KEY INDICATORS

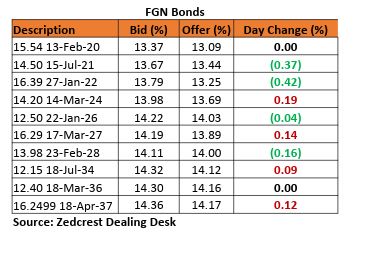

Bonds

Activities in the Bond market today was dominated by the local players, with more buyers seen on the shorter end of the curve (21s and 22s) and mixed sentiments on the longer end (slight demand on the 2036s and more selling on the 34s and 37s). Yields consequently compressed by c.5bps on average. We expect the market to remain client driven in the near term, with yields expected to remain relatively stable, barring a renewed selloff from offshore clients.

Treasury Bills

The T-bills market traded on a slightly bullish note, with yields compressing further by c.7bps on average. This came on the back of continued demand in anticipation of OMO and PMA maturities tomorrow. There was a PMA today, with rates left relatively unchanged on the 91 and 364-day, while the 182-day cleared 20bps higher. We however note that the DMO sold only 60% of the total amount offered, a trend also observed in the previous auction. It consequently decided to repay a total sum of N68.20bn of the 364-day maturity, most likely from the residual balance of its Eurobond proceeds raised earlier this year. We expect yields to remain relatively stable tomorrow, with the CBN expected to conduct an OMO auction to moderate excess inflows from maturing OMO T-bills and Net PMA repayments.

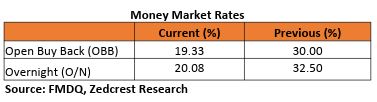

Money Market

The OBB and OVN rates declined further to 17% and 18.33% respectively, as there were no significant funding pressures in the system. System liquidity is consequently estimated to remain relatively stable at c.N100bn positive. We expect rates to trend lower tomorrow, due to expected inflows from OMO and Net PMA repayments (c.N240bn).

FX Market

The Interbank rate remained stable at its previous rate of N305.70/$, with the CBN’s external reserves recorded to have improved by 0.36% to $47.80bn from $47.63bn on the 13th of June. The I&E FX rate fell back by 0.03% to N361.40/$, while the total volume traded improved slightly by 11.83% to $179m. In the parallel market, cash rates appreciated further by 20k to N358.80/$, while the transfer market rate remained stable at N364.00/$.

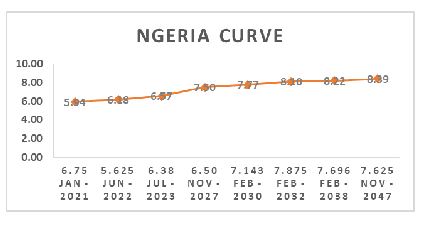

Eurobonds:

The NGERIA Sovereigns traded on a relatively flat note, with yields compressing marginally by c.2bps. We however witnessed slight buying interests mostly on the 27s and 37s which rose by +0.25pt and +0.40pt respectively.

The NGERIA Corps were also relatively quiet, except for slight buying interests seen on the ACCESS 21s Snr and UBANL 22s.

{kind=link}